Back

BackChapter 2: The Economic Problem – Production Possibilities, Efficiency, Trade, and Economic Growth

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

The Production Possibilities Frontier (PPF) and Opportunity Cost

Definition and Structure of the PPF

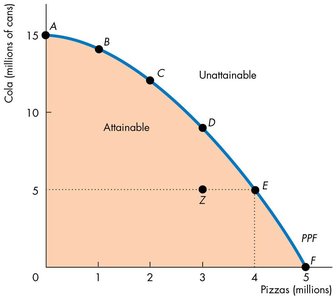

The Production Possibilities Frontier (PPF) is a fundamental concept in microeconomics, representing the boundary between attainable and unattainable combinations of two goods or services, given fixed resources and technology. The PPF illustrates the trade-offs and opportunity costs inherent in production decisions.

Attainable Points: Combinations of goods that can be produced with available resources (on or inside the PPF).

Unattainable Points: Combinations outside the PPF, requiring more resources than available.

Ceteris Paribus: All other factors are held constant except the two goods under consideration.

Production Efficiency and Inefficiency

Production efficiency occurs when it is impossible to produce more of one good without producing less of another. All points on the PPF are efficient, while points inside the PPF are inefficient due to underutilized or misallocated resources.

Efficient Points: On the PPF.

Inefficient Points: Inside the PPF; more of one good can be produced without sacrificing the other.

Trade-offs and Opportunity Cost

Moving along the PPF involves a trade-off: increasing production of one good requires reducing production of the other. The opportunity cost is the amount of one good forgone to produce more of the other.

Opportunity Cost Formula:

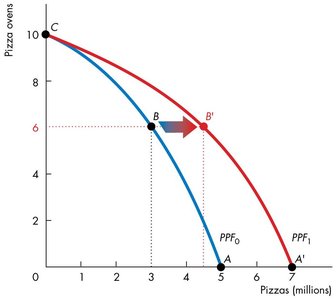

Example: Moving from E to F, producing 1 million more pizzas costs 5 million cans of cola.

Increasing Opportunity Cost: The PPF bows outward because resources are not equally productive in all activities.

Using Resources Efficiently: Marginal Cost and Marginal Benefit

Marginal Cost

The marginal cost of a good is the opportunity cost of producing one additional unit. As production increases, marginal cost typically rises due to increasing opportunity costs.

Marginal Cost Curve: Shows how opportunity cost increases with quantity produced.

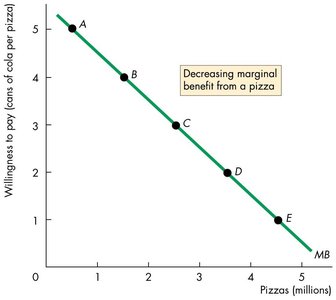

Preferences and Marginal Benefit

Preferences describe individual likes and dislikes. The marginal benefit is the value a person places on consuming one more unit, measured by willingness to pay. Marginal benefit decreases as more of a good is consumed (principle of decreasing marginal benefit).

Marginal Benefit Curve: Shows the relationship between marginal benefit and quantity consumed.

Allocative Efficiency

Allocative efficiency is achieved when resources are used to produce the mix of goods and services most highly valued by society. This occurs at the point where marginal benefit equals marginal cost.

Efficient Quantity: The intersection of the marginal benefit and marginal cost curves determines the optimal production level.

Gains from Trade: Comparative and Absolute Advantage

Comparative vs. Absolute Advantage

Comparative advantage exists when a person or country can produce a good at a lower opportunity cost than others. Absolute advantage refers to higher productivity in producing a good.

Comparative Advantage: Based on opportunity cost.

Absolute Advantage: Based on productivity.

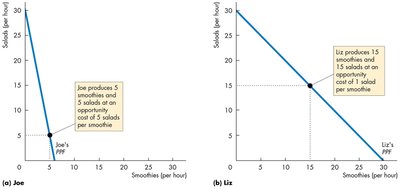

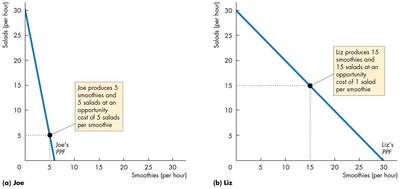

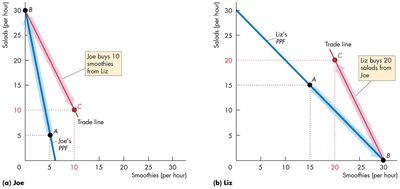

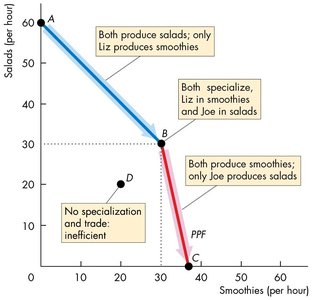

Example: Joe and Liz's Smoothie Bars

Joe and Liz have different opportunity costs for producing smoothies and salads. Joe has a comparative advantage in salads, Liz in smoothies.

Producer | Opportunity Cost of Smoothie | Opportunity Cost of Salad |

|---|---|---|

Joe | 5 salads | 1/5 smoothie |

Liz | 1 salad | 1 smoothie |

Specialization and Gains from Trade

By specializing in their comparative advantage and trading, both Joe and Liz can consume more than they could produce alone. The trade line shows the terms of trade.

Specialization: Joe produces only salads, Liz only smoothies.

Trade: Joe and Liz exchange goods, moving to points outside their individual PPFs.

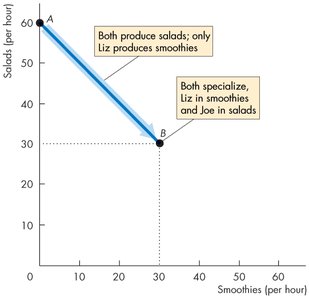

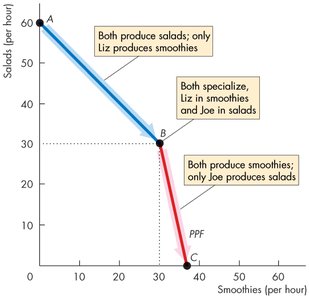

Economy-Wide PPF and Efficiency

The combined PPF of Joe and Liz's economy is kinked, reflecting their different opportunity costs. Efficient production occurs when each specializes according to comparative advantage.

Economic Growth

Sources and Costs of Economic Growth

Economic growth is the expansion of production possibilities, increasing the standard of living. It is driven by technological change and capital accumulation, but requires sacrificing current consumption for investment.

Technological Change: Development of new goods and production methods.

Capital Accumulation: Growth of capital resources, including human capital.

Opportunity Cost: Less current consumption to enable future growth.

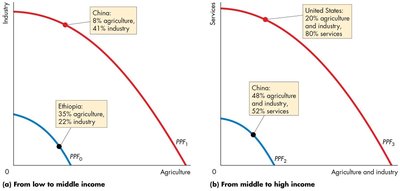

Patterns of Production Across Countries

Economic growth alters the mix of goods produced, as illustrated by differences between low-income and high-income countries.

Economic Coordination: Institutions and Circular Flow

Key Economic Institutions

Efficient resource allocation and gains from trade require coordination through social institutions:

Firms: Organize production and sell goods/services.

Markets: Enable buyers and sellers to transact.

Property Rights: Govern ownership and use of resources.

Money: Facilitates exchange as a medium of payment.

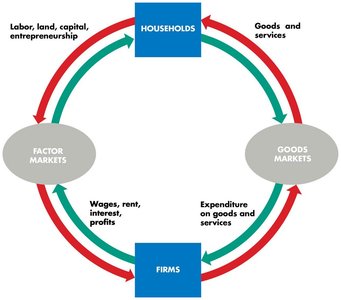

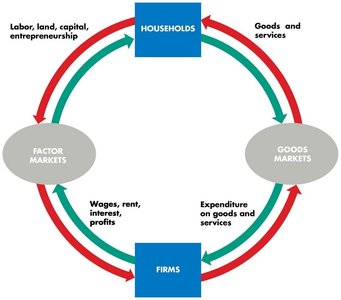

Circular Flow Model

The circular flow model illustrates the movement of goods, services, and money between households and firms through factor and goods markets.

Market Coordination

Markets coordinate individual decisions through price adjustments, ensuring efficient allocation of resources.

Summary Table: Key Concepts

Concept | Definition |

|---|---|

PPF | Boundary of attainable production combinations |

Opportunity Cost | Value of the next best alternative forgone |

Comparative Advantage | Lower opportunity cost in production |

Absolute Advantage | Higher productivity in production |

Marginal Cost | Opportunity cost of one more unit |

Marginal Benefit | Value placed on one more unit |

Allocative Efficiency | Marginal benefit equals marginal cost |

Economic Growth | Expansion of production possibilities |

Institutions | Firms, markets, property rights, money |