Back

BackConsumer Choice and Behavioral Economics: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Consumer Choice and Behavioral Economics

Utility and Consumer Decision Making

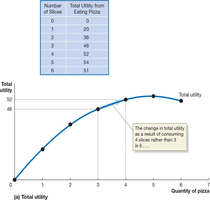

Understanding how consumers make choices is central to microeconomics. Economists use the concept of utility to describe the satisfaction or happiness consumers derive from consuming goods and services. The goal of consumers is to maximize their utility given their limited resources.

Utility: The enjoyment or satisfaction received from consuming goods and services. It is not directly measurable but is a useful theoretical concept.

Marginal Utility (MU): The additional utility gained from consuming one more unit of a good or service. In economics, "marginal" always means "additional."

Law of Diminishing Marginal Utility: As a consumer consumes more units of a good, the additional satisfaction from each extra unit tends to decrease.

Example: Eating pizza at a party: The first slice provides the most satisfaction, but each additional slice gives less extra happiness.

Additional info: The table and graph above illustrate how total utility increases with each slice of pizza, but the rate of increase slows, demonstrating diminishing marginal utility.

Allocating Resources and Maximizing Utility

Consumers face a budget constraint, which limits the amount of goods and services they can purchase. To maximize utility, consumers allocate their resources to equalize the marginal utility per dollar spent across all goods.

Budget Constraint: The limited income available to spend on goods and services.

Marginal Utility per Dollar: Calculated as the marginal utility of a good divided by its price. This measures the "bang for the buck."

Rule of Equal Marginal Utility per Dollar Spent: Consumers maximize utility by allocating their budget so that the marginal utility per dollar is equal for all goods.

Example: If pizza provides more marginal utility per dollar than Coke, a consumer should buy more pizza and less Coke until the marginal utility per dollar is equalized.

Conditions for Maximizing Utility

Satisfy the rule of equal marginal utility per dollar spent:

Exhaust your budget: Spend all available income.

Additional info: If a consumer does not follow these rules, they will not achieve maximum utility. For example, spending all money on one good may yield less total utility than a balanced allocation.

Effects of Price Changes: Income and Substitution Effects

When the price of a good changes, consumers adjust their consumption due to two effects:

Income Effect: The change in quantity demanded resulting from a change in purchasing power due to a price change. If the good is normal, a price decrease increases consumption; if inferior, it decreases consumption.

Substitution Effect: The change in quantity demanded resulting from a good becoming cheaper or more expensive relative to other goods.

Example: If pizza becomes cheaper, consumers may buy more pizza both because they can afford more (income effect) and because pizza is now relatively cheaper than Coke (substitution effect).

Social Influences on Decision Making

Consumer choices are often influenced by social factors, which standard economic models may overlook. These influences can affect demand and market outcomes.

Celebrity Endorsements: Consumers may be influenced by celebrities, believing they know more about the product or wanting to emulate them.

Network Externalities: The usefulness of a product increases as more people use it (e.g., social media platforms, Blu-ray discs).

Fairness: People value fairness and may make choices that are not financially optimal but are perceived as fair (e.g., tipping, ticket pricing).

Example: The NFL keeps ticket prices lower and distributes them randomly to maintain fairness, even though it could earn more by raising prices.

Behavioral Economics: Rationality and Real-World Choices

Behavioral economics examines whether people always make rational choices. Real-world behavior often deviates from the predictions of standard models due to biases, heuristics, and social influences.

Rationality: Standard models assume consumers are rational, but behavioral economics shows that people sometimes make inconsistent or suboptimal choices.

Applications: Businesses and policymakers use insights from behavioral economics to design better products, pricing strategies, and regulations.

Example: Taylor Swift's concert ticket strategy balanced fairness and profit, using verified fan registration to limit scalping and keep prices accessible.

Appendix: Indifference Curves and Budget Lines

Indifference curves and budget lines are graphical tools used to analyze consumer behavior. An indifference curve shows combinations of goods that provide equal utility, while a budget line represents all combinations a consumer can afford.

Indifference Curve: A curve showing all combinations of two goods that provide the same level of utility.

Budget Line: A line showing all combinations of goods that exhaust a consumer's budget.

Optimal Choice: The point where the budget line is tangent to the highest possible indifference curve represents the consumer's optimal choice.

Additional info: The slope of the indifference curve is the marginal rate of substitution, and the slope of the budget line is determined by the relative prices of the goods.