Back

BackConsumers and Incentives: The Buyer’s Problem, Preferences, and Elasticity

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Consumers and Incentives

Key Concepts in Consumer Choice

Understanding consumer behavior is central to microeconomics. The buyer’s problem involves making optimal choices given preferences, prices, and income. This section explores how consumers make decisions, the role of opportunity cost, and how demand curves and consumer surplus are derived.

Preferences: Consumers have tastes and preferences that guide their choices among goods and services.

Prices: Prices are fixed for the individual consumer, who is a price taker in competitive markets.

Income: The consumer’s budget limits the combinations of goods that can be purchased.

Opportunity Cost: The value of the next best alternative forgone when making a choice.

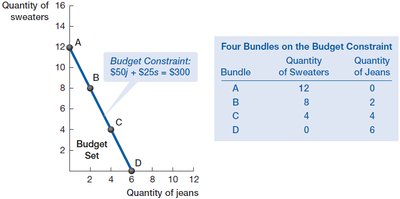

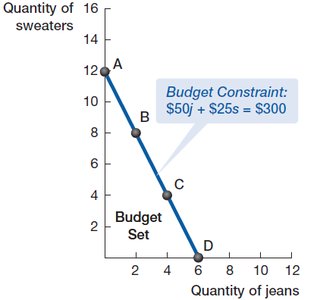

The Budget Set and Budget Constraint

Defining the Budget Set

The budget set is the collection of all possible combinations of goods a consumer can afford given their income and the prices of goods. The budget constraint is the boundary of this set, showing the maximum amount of one good that can be purchased for each possible amount of the other good.

Equation of the Budget Line: If income is , price of good X is , and price of good Y is , then the budget constraint is .

Slope of the Budget Line: The slope is , representing the opportunity cost of one good in terms of the other.

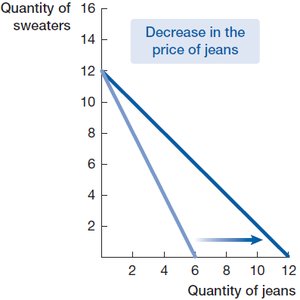

Opportunity Cost and Trade-offs

The slope of the budget line reflects the trade-off between two goods. The opportunity cost of one good is the amount of the other good that must be given up to obtain one more unit.

Opportunity Cost of Jeans:

Opportunity Cost of Sweaters:

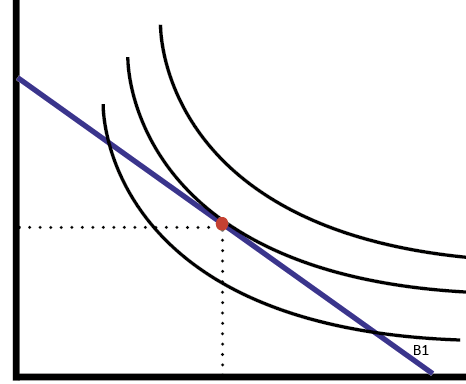

Preferences and Utility

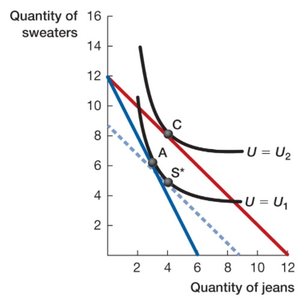

Indifference Curves and Utility

Indifference curves represent combinations of goods that provide the consumer with the same level of satisfaction (utility). The consumer’s goal is to reach the highest possible indifference curve given their budget constraint.

Properties of Indifference Curves:

Downward sloping (trade-off between goods)

Convex to the origin (diminishing marginal rate of substitution)

Curves cannot cross

Curves further from the origin represent higher utility

Marginal Rate of Substitution (MRS): The rate at which a consumer is willing to substitute one good for another, equal to the slope of the indifference curve:

Consumer Equilibrium

Optimal Choice

The optimal consumption bundle is found where the budget line is tangent to the highest attainable indifference curve. At this point, the rate at which the consumer is willing to trade one good for another (MRS) equals the rate at which the market allows the trade (price ratio).

Equilibrium Condition: or

Consumers maximize utility by equalizing the marginal benefit per dollar spent across all goods.

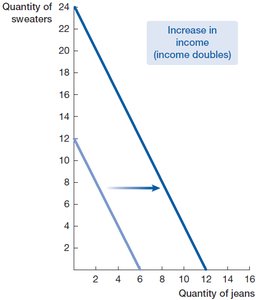

Changes in Prices and Income

Effects of Price and Income Changes

When the price of a good changes, the budget constraint rotates, leading to changes in the optimal consumption bundle. An increase in income shifts the budget constraint outward, allowing the consumer to reach higher indifference curves.

Substitution Effect: Change in consumption due to a change in relative prices, holding utility constant.

Income Effect: Change in consumption due to a change in purchasing power.

Behavioral Economics and Incentives

Monetary Incentives and Consumer Behavior

Behavioral economics examines how real-world consumers respond to incentives. For example, offering a monetary incentive to quit smoking or to get vaccinated can alter consumer choices by changing the perceived benefits and opportunity costs.

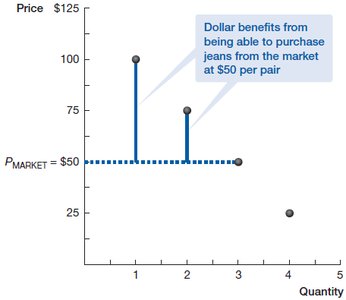

Consumer Surplus: The difference between what a consumer is willing to pay and what they actually pay.

Monetary incentives can increase the likelihood of certain behaviors, as shown in experimental studies.

Elasticity of Demand

Price Elasticity of Demand

Elasticity measures how responsive quantity demanded is to changes in price, income, or the price of other goods.

Price Elasticity of Demand (ED):

Interpretation:

: Elastic demand (quantity demanded is sensitive to price changes)

: Inelastic demand (quantity demanded is not very sensitive to price changes)

: Unit elastic

Determinants of Elasticity

Availability of substitutes

Share of budget spent on the good

Time horizon

Other Elasticities

Cross-Price Elasticity: Measures how the quantity demanded of one good responds to a change in the price of another good.

Positive: Substitutes

Negative: Complements

Income Elasticity: Measures how the quantity demanded changes as consumer income changes.

Positive: Normal goods

Negative: Inferior goods

Applications and Practice Problems

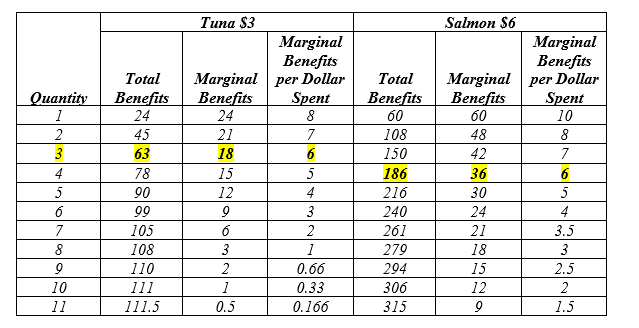

Budget Constraint and Marginal Analysis Example

Consider a consumer with a fixed budget choosing between two goods. The optimal bundle is found by comparing marginal benefits per dollar spent.

Quantity | Total Benefits (Tuna $3) | Marginal Benefits | Marginal Benefits per Dollar | Total Benefits (Salmon $6) | Marginal Benefits | Marginal Benefits per Dollar |

|---|---|---|---|---|---|---|

1 | 24 | 24 | 8 | 60 | 60 | 10 |

2 | 45 | 21 | 7 | 108 | 48 | 8 |

3 | 63 | 18 | 6 | 150 | 42 | 7 |

4 | 78 | 15 | 5 | 186 | 36 | 6 |

5 | 90 | 12 | 4 | 216 | 30 | 5 |

6 | 99 | 9 | 3 | 240 | 24 | 4 |

7 | 105 | 6 | 2 | 261 | 21 | 3.5 |

8 | 108 | 3 | 1 | 279 | 18 | 3 |

9 | 110 | 2 | 0.66 | 294 | 15 | 2.5 |

10 | 111 | 1 | 0.33 | 306 | 12 | 2 |

11 | 111.5 | 0.5 | 0.166 | 315 | 9 | 1.5 |

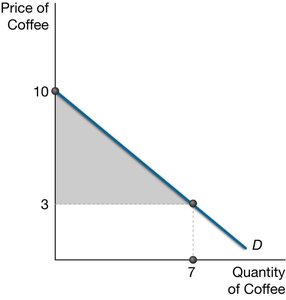

Consumer Surplus Example

Consumer surplus is the area between the demand curve and the price line, up to the quantity purchased. For example, if Alex’s demand for coffee is and the price is $3 cups. The consumer surplus is the area of the triangle above the price line and below the demand curve.

Additional info: These notes provide a comprehensive overview of consumer choice, utility maximization, and elasticity, with practical examples and graphical analysis to reinforce key concepts in microeconomics.