Back

BackEconomic Efficiency, Government Price Setting, and Taxes: Microeconomics Study Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Efficiency, Government Price Setting, and Taxes

Introduction

This unit explores how competitive markets achieve economic efficiency, the effects of government intervention through price controls and taxes, and how these interventions impact consumer surplus, producer surplus, and overall welfare. Understanding these concepts is essential for analyzing real-world market outcomes and policy decisions.

Consumer Surplus and Producer Surplus

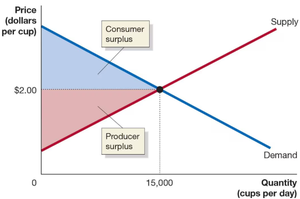

Consumer Surplus

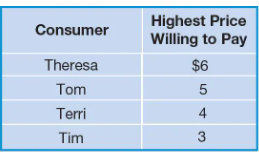

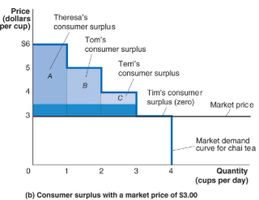

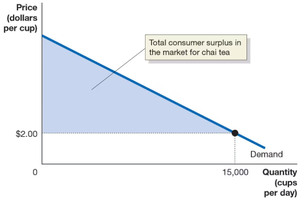

Consumer surplus is the dollar benefit consumers receive from purchasing goods or services at a price lower than the maximum they are willing to pay. It is a key measure of consumer welfare in a market.

Definition: The difference between the highest price a consumer is willing to pay and the actual price paid.

Marginal Benefit: The additional benefit from consuming one more unit of a good or service.

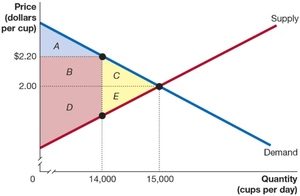

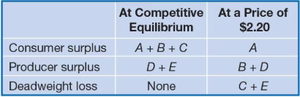

Measurement: Total consumer surplus is the area below the demand curve and above the market price.

Example: If a consumer is willing to pay $6.99 for a movie rental but pays $4.99, the consumer surplus is $2.

Producer Surplus

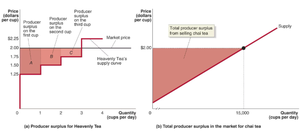

Producer surplus is the dollar benefit firms receive from selling goods or services at a price higher than the minimum they are willing to accept. It reflects the net gain to producers from market transactions.

Definition: The difference between the lowest price a firm would accept and the price it actually receives.

Marginal Cost: The change in total cost from producing one more unit.

Measurement: Total producer surplus is the area above the supply curve and below the market price.

Example: If the marginal cost of producing a cup of tea is $1.25 and the market price is $2, the producer surplus is $0.75 for that cup.

Economic Surplus

Economic surplus is the sum of consumer surplus and producer surplus. It represents the total net benefit to society from market transactions.

Formula:

Measurement: In a competitive market at equilibrium, economic surplus is maximized.

The Efficiency of Competitive Markets

Marginal Benefit Equals Marginal Cost in Competitive Equilibrium

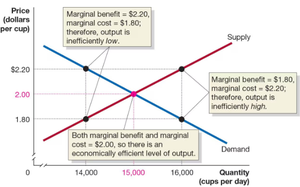

Economic efficiency in competitive markets occurs when the marginal benefit to consumers equals the marginal cost of production. This ensures resources are allocated optimally.

Competitive Equilibrium: The point where the demand curve (marginal benefit) intersects the supply curve (marginal cost).

Efficiency Condition:

Outcome: At equilibrium, every unit produced provides a benefit to buyers at least equal to the cost to producers.

Economic Surplus and Deadweight Loss

Economic surplus is maximized at equilibrium. When the market is not at equilibrium, deadweight loss occurs, representing lost welfare due to inefficiency.

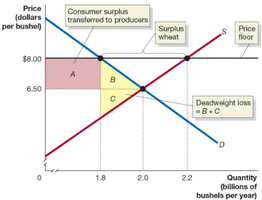

Deadweight Loss: The reduction in economic surplus from a market not being in competitive equilibrium.

Measurement: Deadweight loss is the area representing lost consumer and producer surplus.

Government Intervention: Price Floors and Price Ceilings

Price Floors

A price floor is a legally determined minimum price that sellers may receive. It is binding only if set above the equilibrium price.

Example: Agricultural price supports, such as wheat and corn.

Effects: Increases producer surplus, decreases consumer surplus, creates deadweight loss, and may cause surpluses.

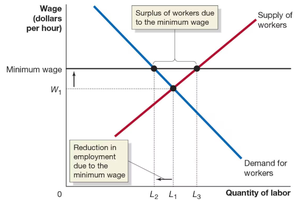

Price Floors: Labor Markets

Minimum wage laws are an example of price floors in labor markets. They set a minimum wage above the equilibrium wage.

Effects: Reduces employment, increases labor supply, creates a surplus of workers (unemployment).

Price Ceilings

A price ceiling is a legally determined maximum price that sellers may charge. It is binding only if set below the equilibrium price.

Example: Rent control in housing markets.

Effects: Increases consumer surplus for some, decreases producer surplus, creates deadweight loss, and causes shortages.

Illegal Markets and Peer-to-Peer Sites

When price controls are enacted, buyers and sellers may circumvent regulations through illegal markets or online platforms, undermining the intended effects of government intervention.

Results of Price Controls

Winners: Those who benefit from lower prices or higher incomes.

Losers: Those who face shortages or reduced incomes.

Loss of Efficiency: Deadweight loss measures the decrease in economic efficiency.

Positive vs. Normative Analysis

Positive Analysis: Concerned with what is (objective outcomes).

Normative Analysis: Concerned with what should be (value judgments).

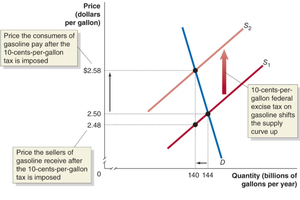

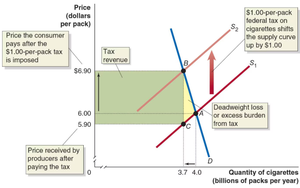

The Economic Effect of Taxes

Taxes and Economic Efficiency

Government taxes on goods and services shift supply or demand curves, reducing the quantity produced and consumed, and causing deadweight loss.

Public Finance: The field analyzing government revenue and expenditure.

Excess Burden: The deadweight loss from a tax.

Efficiency: A tax is efficient if it imposes a small excess burden relative to the revenue it raises.

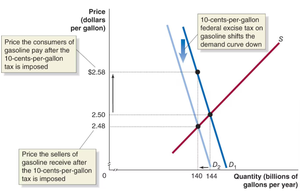

Tax Incidence

Tax incidence refers to the actual division of the tax burden between buyers and sellers, regardless of who is legally required to pay.

Graphical Analysis: Taxes shift supply or demand curves, changing equilibrium prices and quantities.

Appendix: Quantitative Demand and Supply Analysis

Demand and Supply Equations

Quantitative analysis uses equations to determine equilibrium price and quantity in a market.

Example Equations:

Demand:

Supply:

Equilibrium Condition:

Solving for Equilibrium Price:

Equilibrium Quantity: Substitute into either equation.

Calculating Consumer Surplus and Producer Surplus

Consumer surplus and producer surplus can be calculated using the areas under the demand and supply curves, respectively, above or below the market price.