Back

BackCh.12 Firms in Perfectly Competitive Markets: Microeconomics Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Firms in Perfectly Competitive Markets

Introduction to Perfect Competition

Perfect competition is a foundational concept in microeconomics, describing a market structure where many firms sell identical products, and no single firm can influence the market price. This chapter explores the characteristics, profit maximization, and efficiency of perfectly competitive markets.

Market Structures

Types of Market Structures

Perfect Competition: Many firms, identical products, no barriers to entry.

Monopolistic Competition: Many firms, differentiated products.

Oligopoly: Few firms, may sell identical or differentiated products.

Monopoly: One firm, unique product, high barriers to entry.

Each structure provides insight into how firms interact with buyers and set prices.

12.1 Perfectly Competitive Markets

Definition and Characteristics

Many buyers and sellers participate in the market.

Identical products are sold by all firms.

No barriers to entry for new firms.

Firms are price takers: they accept the market price as given.

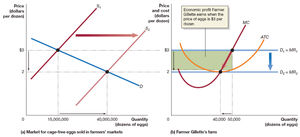

Perfect competition is rare in reality but is closely approximated by some agricultural markets, such as wheat or eggs.

Demand Curve for a Perfectly Competitive Firm

The market demand curve is downward sloping, but the individual firm faces a horizontal demand curve at the market price.

Firms can sell any quantity at the market price but cannot influence the price by their own output decisions.

Market Equilibrium and the Invisible Hand

Adam Smith's concept of the invisible hand describes how individual actions in a market lead to outcomes that benefit society as a whole.

Spontaneous order arises when collective actions, without central coordination, achieve efficient outcomes.

12.2 How a Firm Maximizes Profit in a Perfectly Competitive Market

Revenue Concepts

Total Revenue (TR):

Average Revenue (AR):

Marginal Revenue (MR):

For a perfectly competitive firm, .

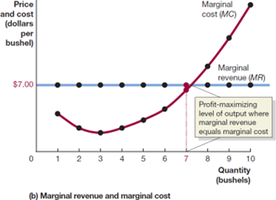

Profit Maximization Rule

Profit is maximized where MR = MC (Marginal Revenue equals Marginal Cost).

For perfect competition, this is also where P = MC.

Profit Calculation

Profit:

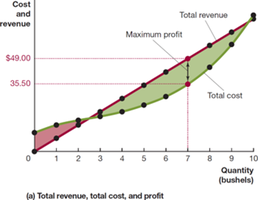

At the profit-maximizing output, the vertical distance between total revenue and total cost is greatest.

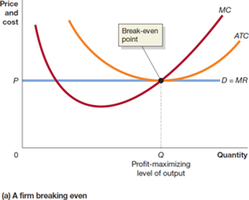

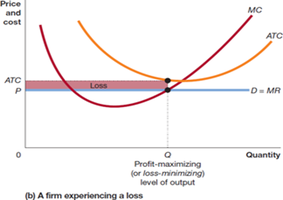

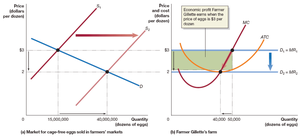

12.3 Illustrating Profit or Loss on the Cost Curve Graph

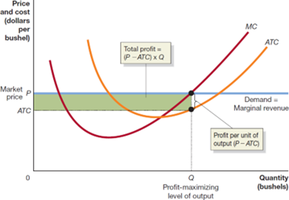

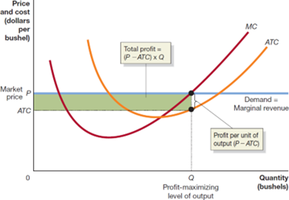

Graphical Representation of Profit

Profit per unit:

Total profit:

Profit is shown as the area between price and average total cost, up to the profit-maximizing quantity.

Break-Even and Loss

If , the firm makes a profit.

If , the firm breaks even.

If , the firm incurs a loss.

Even when making a loss, the firm should produce where to minimize losses.

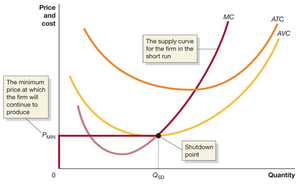

12.4 Deciding Whether to Produce or to Shut Down in the Short Run

Shutdown Rule

Fixed costs are sunk costs and should not affect the shutdown decision.

The firm should produce if (Average Variable Cost).

If , the firm should shut down in the short run.

The marginal cost curve above AVC is the firm's short-run supply curve.

12.5 Entry and Exit of Firms in the Long Run

Economic Profit and Entry

Economic profit includes both explicit and implicit costs (opportunity costs).

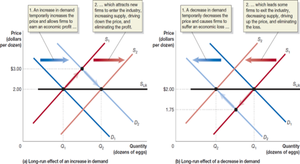

When firms earn economic profit, new firms enter the market, increasing supply and lowering price until profit is eliminated.

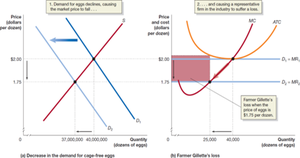

Economic Loss and Exit

If firms incur economic losses, some exit the market, reducing supply and raising price until losses are eliminated.

Long-Run Competitive Equilibrium

In the long run, firms earn zero economic profit (break even).

The market price equals the minimum point on the long-run average cost curve.

The long-run supply curve is horizontal at this price in a constant-cost industry.

Increasing-Cost and Decreasing-Cost Industries

Increasing-cost industry: Entry raises input prices, causing the long-run supply curve to slope upward.

Decreasing-cost industry: Entry lowers input prices or increases efficiency, causing the long-run supply curve to slope downward.

Market Adjustment to Demand Changes

An increase in demand raises price and profit, attracting entry until price returns to break-even.

A decrease in demand lowers price and causes losses, leading to exit until price returns to break-even.

12.6 Perfect Competition and Efficiency

Productive and Allocative Efficiency

Productive efficiency: Goods are produced at the lowest possible cost (at minimum ATC).

Allocative efficiency: Goods are produced up to the point where the last unit provides a marginal benefit to consumers equal to the marginal cost of production ().

Perfectly competitive markets achieve both productive and allocative efficiency in the long run, serving as benchmarks for evaluating other market structures.

Summary Table: Key Rules for Perfect Competition

Condition | Firm's Action |

|---|---|

Make a profit | |

Break even | |

Make a loss | |

Produce in short run | |

Shut down in short run | |

Profit-maximizing output |

Additional info: These notes synthesize textbook content, lecture slides, and standard microeconomic theory to provide a comprehensive overview of perfectly competitive markets, including graphical analysis and real-world applications.