Back

BackFirms in Perfectly Competitive Markets: Microeconomics Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Firms in Perfectly Competitive Markets

Overview of Market Structures

Market structures describe how firms interact with buyers to sell their output. The main types, in order of decreasing competitiveness, are:

Perfectly competitive markets

Monopolistically competitive markets

Oligopolies

Monopolies

Each structure provides insight into firm behavior and market outcomes.

Perfectly Competitive Markets

A perfectly competitive market is characterized by:

Many buyers and sellers

Identical products sold by all firms

No barriers to entry or exit

Firms in such markets are price takers, meaning they cannot influence the market price and must accept it as given. Agricultural markets, such as wheat, are classic examples.

Demand Curve: For an individual firm, the demand curve is perfectly elastic (horizontal) at the market price.

Profit Maximization in Perfect Competition

Firms aim to maximize profit, defined as total revenue minus total cost. In perfect competition:

Total Revenue (TR):

Average Revenue (AR):

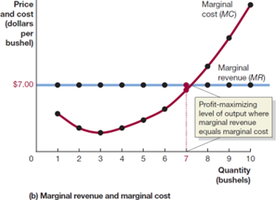

Marginal Revenue (MR):

For a perfectly competitive firm, .

The profit-maximizing output is where marginal revenue equals marginal cost (). This is also where for perfect competitors.

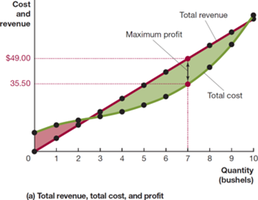

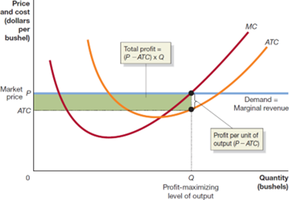

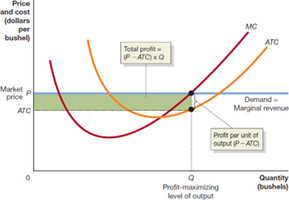

Illustrating Profit or Loss on the Cost Curve Graph

Profit can be visualized as the area between total revenue and total cost curves, or as the rectangle between price and average total cost at the profit-maximizing quantity:

Total Profit:

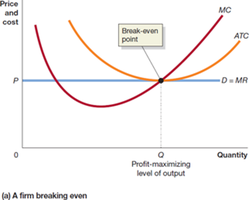

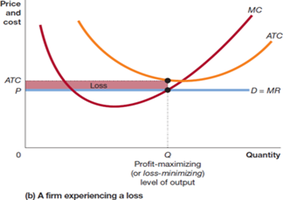

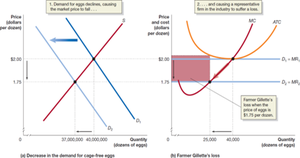

Break-Even and Loss-Minimizing Output

Even if a firm cannot make a profit, it should still produce at the output where to minimize losses. The firm's status can be determined as follows:

If , the firm makes a profit.

If , the firm breaks even.

If , the firm incurs a loss.

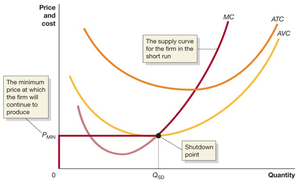

Short-Run Production and Shutdown Decision

When facing losses, a firm must decide whether to continue producing or shut down temporarily. The key consideration is whether price covers average variable cost (AVC):

If , produce where .

If , shut down (produce zero output).

The marginal cost curve above AVC is the firm's short-run supply curve.

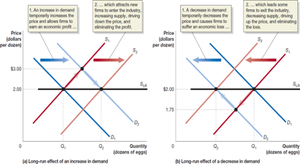

Entry and Exit in the Long Run

In the long run, firms can enter or exit the market:

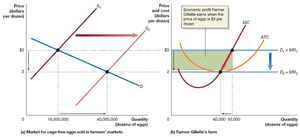

Economic profit attracts new firms, increasing supply and lowering price until profits are eliminated.

Economic loss causes firms to exit, decreasing supply and raising price until losses are eliminated.

Long-run equilibrium occurs when firms earn zero economic profit (break even), and price equals the minimum point of the long-run average cost curve.

The Long-Run Supply Curve

The long-run supply curve in a perfectly competitive market is typically horizontal at the break-even price, reflecting that the market can supply any quantity demanded at this price. However, in increasing-cost industries, the curve slopes upward, and in decreasing-cost industries, it slopes downward.

Efficiency in Perfect Competition

Perfect competition leads to two types of efficiency:

Productive efficiency: Goods are produced at the lowest possible cost (at the minimum of the average total cost curve).

Allocative efficiency: Goods are produced up to the point where the marginal benefit to consumers equals the marginal cost of production ().

These efficiencies serve as benchmarks for evaluating other market structures.