Back

BackGeneral Equilibrium and the Efficiency of Perfect Competition

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

General Equilibrium and the Efficiency of Perfect Competition

Introduction

This chapter explores how individual markets and economic agents interact to determine the overall allocation of resources in an economy. It examines the concepts of general equilibrium, efficiency, and the conditions under which markets succeed or fail in achieving optimal outcomes.

Market Adjustment to Changes in Demand

General Equilibrium and Market Connections

General equilibrium occurs when all markets in an economy are in simultaneous equilibrium, meaning supply equals demand in every market.

Markets are interconnected; a change in one market (such as a shift in demand) can affect other markets through changes in prices and resource allocation.

Partial equilibrium analysis examines individual markets in isolation, while general equilibrium considers the entire system.

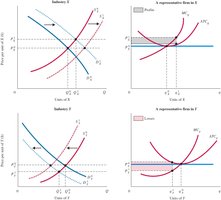

Example: If demand for product X increases, its price rises, attracting resources from other sectors (such as Y), where demand and prices may fall. This reallocation continues until profits and losses are eliminated, and all markets clear.

Allocative Efficiency and Competitive Equilibrium

Pareto Efficiency

Pareto efficiency (or Pareto optimality): A situation where no individual can be made better off without making someone else worse off.

Efficiency requires that resources are allocated to produce what people want at the lowest possible cost.

To assess efficiency, economists consider both the gains and losses to different members of society.

Example: Budget cuts in a government office may save money for taxpayers but could increase waiting times for services, illustrating trade-offs in efficiency and equity.

Economic Efficiency in Perfect Competition

Perfect competition leads to efficient allocation of resources among firms and households.

All firms face the same input prices and maximize profits, ensuring resources are used where they are most productive.

Consumers freely choose their preferred combinations of goods, leading to an efficient distribution of output.

The efficient mix of output is achieved when all firms set price equal to marginal cost:

The Sources of Market Failure

Market Failure

Market failure occurs when resources are misallocated, resulting in waste or lost surplus.

Four main sources of market failure:

Imperfect competition: Firms with market power can set prices above marginal cost, leading to inefficient outcomes.

Public goods: Goods that are non-excludable and non-rivalrous (e.g., national defense) are underprovided by markets.

Externalities: Costs or benefits that affect third parties outside the transaction (e.g., pollution).

Imperfect information: When buyers or sellers lack full knowledge, markets may not allocate resources efficiently.

Evaluating the Market Mechanism

Efficiency and Equity

While perfectly competitive markets can achieve efficiency, real-world markets often deviate from these ideal conditions.

Government intervention may be justified to correct market failures, but it can also introduce inefficiencies.

Besides efficiency, economic systems are also evaluated based on equity (fairness) in the distribution of resources and outcomes.

Key Terms and Concepts

Efficiency: Producing what people want at the lowest possible cost.

Externality: A cost or benefit imposed on others outside a transaction.

General equilibrium: All markets are in equilibrium simultaneously.

Imperfect information: Lack of full knowledge by market participants.

Market failure: Inefficient allocation of resources by the market.

Pareto efficiency: No one can be made better off without making someone else worse off.

Partial equilibrium analysis: Examining one market in isolation.

Public goods: Goods that are non-excludable and non-rivalrous.

Table: Sources of Market Failure

Source | Description | Example |

|---|---|---|

Imperfect Competition | Firms have market power, set prices above marginal cost | Monopoly pricing |

Public Goods | Non-excludable, non-rivalrous goods underprovided by markets | National defense |

Externalities | Costs or benefits spill over to third parties | Pollution, vaccination |

Imperfect Information | Buyers or sellers lack full information | Used car market ("lemons problem") |

Application: General Equilibrium and Real-World Events

The war in Ukraine and its impact on oil prices illustrates how interconnected markets are. A disruption in the oil market led to higher production and transportation costs, affecting prices across many sectors and prompting policy responses.

Critical Thinking: Use general equilibrium analysis to trace how a shock in one market (like oil) can ripple through the economy, affecting prices, output, and welfare in other markets.

Additional info: The images of the textbook cover and publisher logo are not included, as they do not directly reinforce the economic concepts discussed.