Back

BackImperfect Competition and Strategic Behaviour: Monopolistic Competition, Oligopoly, and Game Theory

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Imperfect Competition and Strategic Behaviour

Introduction to Imperfect Competition

Imperfect competition refers to market structures that fall between the extremes of perfect competition and monopoly. Most real-world industries are imperfectly competitive, with firms possessing some degree of market power but not complete control over the market. The extent of market power and the number of firms distinguish different types of imperfect competition.

Perfect Competition: Many small firms, identical products, no market power.

Monopoly: One firm, unique product, complete market power.

Imperfect Competition: Many or few firms, differentiated products, some market power.

Types of Imperfect Competition

Industries with Many Small Firms: Explained by the theory of monopolistic competition. Examples include hair salons, pubs, and local service providers.

Industries with a Few Large Firms: Explained by the theory of oligopoly. Examples include grocery chains, airlines, and life insurance companies.

Industrial Concentration

Industrial concentration measures the extent to which market power is held by a small number of firms. The concentration ratio is the fraction of total market sales controlled by the largest firms in the industry. Defining the relevant market (geographically and by product) is a key challenge in calculating concentration ratios.

Characteristics of Imperfectly Competitive Firms

Product Differentiation: Firms offer products that are similar but not identical, allowing for some control over price.

Price Setting: Firms are price setters, facing downward-sloping demand curves for their differentiated products.

Non-Price Competition: Firms compete through advertising, quality, guarantees, and other means beyond price.

Monopolistic Competition

Definition and Key Features

Monopolistic competition is a market structure with many firms, free entry and exit, and differentiated products. Each firm has some market power but faces competition from many close substitutes.

Developed by Edward Chamberlin (1933).

Examples: Dry cleaners, restaurants, auto mechanics, local service businesses.

Assumptions of Monopolistic Competition

Each firm produces a differentiated product and faces a highly elastic, downward-sloping demand curve.

All firms have access to the same technology and cost curves.

Firms do not behave strategically; they ignore competitors' reactions.

Free entry and exit in the industry.

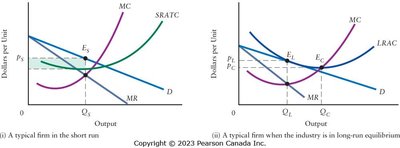

Short-Run and Long-Run Profit Maximization

In the short run, a monopolistically competitive firm behaves like a monopoly, maximizing profit where marginal revenue equals marginal cost. In the long run, entry and exit drive profits to zero, and firms produce at less than minimum average cost (excess capacity).

Short Run: Firms can earn positive, zero, or negative profits.

Long Run: Entry/exit ensures zero economic profit; firms operate with excess capacity.

Excess Capacity and Comparison to Perfect Competition

Excess Capacity: Firms produce less than the output that minimizes average cost. The gap between current output and minimum-cost output measures excess capacity.

Perfect Competition Comparison: In perfect competition, firms produce at minimum average cost in the long run, with price equal to marginal cost and average cost.

Oligopoly and Game Theory

Oligopoly: Definition and Features

An oligopoly is a market structure with a small number of large firms, each with significant market power. Firms are interdependent and must consider rivals' reactions when making decisions.

High market concentration ratio.

Firms face downward-sloping demand curves.

Strategic behaviour is central: firms anticipate and react to competitors' actions.

Profit Maximization in Oligopoly

Firms maximize profit where marginal revenue equals marginal cost, but marginal revenue depends on rivals' responses.

Strategic behaviour complicates decision-making.

Cooperative vs. Non-Cooperative Outcomes

Cooperative (Collusive) Outcome: Firms act together to maximize joint profits, behaving like a monopoly.

Non-Cooperative Outcome: Firms act independently to maximize individual profits, often leading to lower profits for all.

Game Theory in Oligopoly

Game theory analyzes strategic decision-making where each player's outcome depends on the actions of others. In oligopoly, firms are the players, their strategies are price/output decisions, and payoffs are profits.

Duopoly: A two-firm oligopoly is used to illustrate basic game theory concepts.

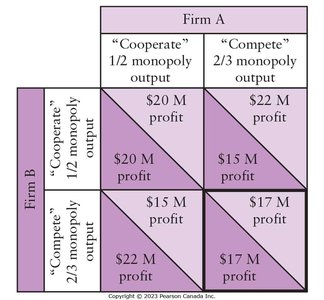

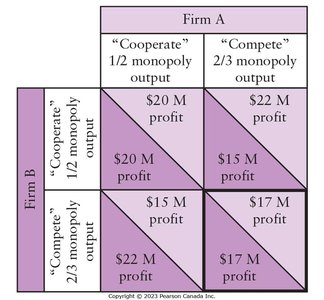

Payoff Matrix Example

The payoff matrix shows the profits for each firm depending on whether they cooperate or compete. The dominant strategy is to compete, leading to a non-cooperative outcome (Nash equilibrium), even though both would be better off cooperating.

Firm A: Cooperate | Firm A: Compete | |

|---|---|---|

Firm B: Cooperate | $20M, $20M | $15M, $22M |

Firm B: Compete | $22M, $15M | $17M, $17M |

Nash Equilibrium

A Nash equilibrium occurs when each player is doing the best they can, given the actions of the other. In the oligopoly example, both firms competing is the Nash equilibrium, even though both would be better off cooperating.

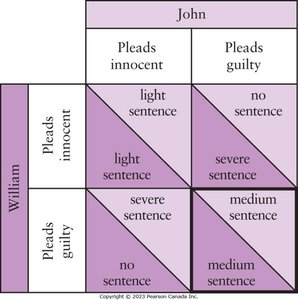

The Prisoner's Dilemma

The prisoner's dilemma is a classic example of a game where rational individual strategies lead to a worse collective outcome. In oligopoly, this explains why firms may fail to cooperate even when it is in their joint interest.

John: Pleads Innocent | John: Pleads Guilty | |

|---|---|---|

William: Pleads Innocent | light sentence, light sentence | severe sentence, no sentence |

William: Pleads Guilty | no sentence, severe sentence | medium sentence, medium sentence |

Extensions of Game Theory

Game theory applies to a wide range of strategic interactions, including pricing, product development, and other competitive behaviours among oligopolists. The prisoner's dilemma is just one example; many other games are relevant in economics.

Additional info: Game theory is a foundational tool in modern microeconomics for analyzing strategic behaviour in markets with a small number of firms. The Nash equilibrium concept is widely used to predict outcomes in competitive and cooperative settings.