Back

BackLecture 12: Information Asymmetry and Market Failure

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Information Asymmetry

Markets often operate under conditions of uncertainty, where not all parties have equal access to relevant information. Asymmetric information occurs when one party in a transaction possesses more or better information than the other. This disparity can significantly impact market efficiency and lead to various forms of market failure.

Why Markets Fail

Overview of Market Failure

Market failure arises when unregulated competitive markets do not allocate resources efficiently. There are four primary reasons for market failure:

Market Power: When a single buyer or seller (or a group) can influence prices, leading to inefficient allocation of resources.

Externalities: Costs or benefits of a transaction that affect third parties and are not reflected in market prices.

Public Goods: Goods that are non-excludable and non-rivalrous, leading to underproduction in private markets.

Incomplete Information: When consumers or producers lack accurate information about prices or product quality, resulting in inefficient market outcomes.

Asymmetric Information

Types of Asymmetric Information

There are two main types of asymmetric information that cause market problems:

Hidden Characteristics: Attributes known to one party but not the other (e.g., product quality known to the seller but not the buyer).

Hidden Actions: Actions taken by one party that are not observed by the other (e.g., effort exerted by an employee).

Problems Arising from Asymmetric Information

Adverse Selection

Adverse selection occurs when one party exploits hidden characteristics, leading to market inefficiency. For example, in the health insurance market, individuals with higher health risks are more likely to purchase insurance, raising costs for insurers and potentially driving low-risk individuals out of the market.

Adverse selection is especially problematic when sellers have more information about product quality than buyers.

This can result in high-quality goods being driven out of the market by low-quality goods, as seen in the "lemons problem."

The Lemons Problem

The lemons problem describes a situation where, due to asymmetric information, low-quality goods ("lemons") drive high-quality goods out of the market. George Akerlof's seminal paper illustrated this using the market for used cars. As buyers cannot distinguish between high- and low-quality cars, they are only willing to pay an average price, which discourages sellers of high-quality cars from participating.

As the proportion of low-quality goods increases, buyers' willingness to pay decreases further, exacerbating the problem.

Examples of Adverse Selection

Adverse selection is not limited to used cars. It appears in many markets, including:

Health insurance

Retail stores (product returns and repairs)

Dealers of rare collectibles (authenticity concerns)

Home repair services (quality of work)

Restaurants (food safety and quality)

Reducing Adverse Selection

Strategies to Mitigate Adverse Selection

There are several methods to reduce adverse selection:

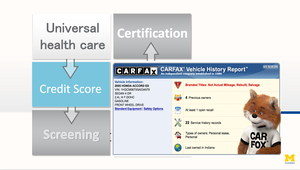

Restricting Exploitation: For example, universal health coverage spreads risk across all individuals, reducing the incentive for only high-risk individuals to purchase insurance.

Equalizing Information: Credit scores and shared credit histories help lenders distinguish between high- and low-risk borrowers.

Screening: Actions by the uninformed party to elicit information (e.g., requiring inspections or tests).

Signaling: Actions by the informed party to convey information (e.g., educational credentials in the labor market).

Standardization and Reputation: Customer reviews and ratings provide information about product quality.

Certification: Third-party verification that a product meets certain standards (e.g., CARFAX reports for used cars).

Moral Hazard

Definition and Examples

Moral hazard arises when one party takes unobservable actions that affect the outcome of a transaction, often because they do not bear the full consequences of their actions. For example, an insured individual may take greater risks because they do not bear the full cost of those risks.

Common examples include reckless driving with car insurance, or banks taking excessive risks when they expect government bailouts.

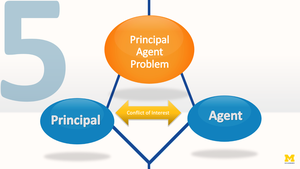

The Principal–Agent Problem

Nature of the Principal–Agent Problem

The principal–agent problem occurs when an agent (e.g., a manager) has incentives that do not align with those of the principal (e.g., the owner). This misalignment is exacerbated by information asymmetry, as the principal cannot perfectly monitor the agent's actions.

Principals can use monitoring, market discipline, and incentive contracts to align interests.

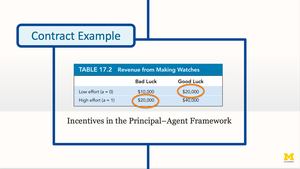

Contract Design and Incentives

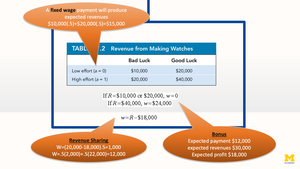

To mitigate the principal–agent problem, principals can design contracts that align the agent's incentives with their own. For example, a manufacturer may offer a repairperson a bonus or revenue-sharing arrangement to encourage high effort, even when effort cannot be directly observed.

Effort Level | Bad Luck Revenue | Good Luck Revenue |

|---|---|---|

Low Effort (a=0) | $10,000 | $20,000 |

High Effort (a=1) | $20,000 | $40,000 |

Fixed Wage: No incentive for high effort; expected revenue is $15,000.

Bonus Arrangement: Rewards high effort; expected payment is $12,000.

Revenue Sharing: Wage depends on revenue exceeding a threshold, incentivizing high effort.

Summary Table: Key Concepts in Information Asymmetry

Concept | Definition | Example |

|---|---|---|

Adverse Selection | Hidden characteristics exploited by one party | Used car market (lemons problem) |

Moral Hazard | Hidden actions taken after a transaction | Reckless driving with insurance |

Principal–Agent Problem | Agent's incentives not aligned with principal's | Manager vs. owner objectives |

Conclusion

Asymmetric information is a central challenge in microeconomics, leading to adverse selection, moral hazard, and principal–agent problems. Understanding these concepts and the mechanisms to mitigate them is essential for analyzing real-world markets and designing effective policies.