Back

BackMicroeconomics Exam Study Guide: Monopoly, Competition, Cost, and Production

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

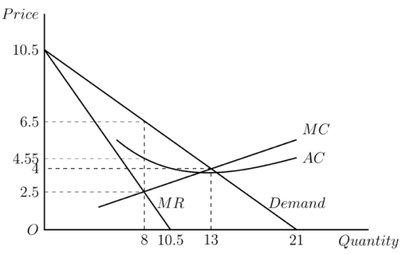

Q1. The monopolist’s profit-maximizing output level is ____.

Background

Topic: Monopoly Profit Maximization

This question tests your understanding of how a monopolist determines the quantity of output that maximizes profit, using marginal revenue (MR) and marginal cost (MC).

Key Terms and Formulas:

Marginal Revenue (MR): The additional revenue from selling one more unit.

Marginal Cost (MC): The additional cost from producing one more unit.

Profit Maximization Rule for Monopoly:

Step-by-Step Guidance

Examine the graph and identify the MR and MC curves.

Find the quantity where the MR curve intersects the MC curve. This is the profit-maximizing output for the monopolist.

Check the horizontal axis (Quantity) at the intersection point to determine the output level.

Do not confuse this with the competitive equilibrium, which would be where MC intersects Demand.

Try solving on your own before revealing the answer!

Final Answer: 8 units

The intersection of MR and MC occurs at Quantity = 8, which is the monopolist's profit-maximizing output.

Q2. The monopolist’s profit-maximizing price level is ____.

Background

Topic: Monopoly Pricing

This question tests your ability to determine the price a monopolist will charge at the profit-maximizing output, using the demand curve.

Key Terms and Formulas:

Demand Curve: Shows the price consumers are willing to pay for each quantity.

Profit-Maximizing Price: The price on the demand curve at the profit-maximizing quantity.

Step-by-Step Guidance

From the previous question, identify the profit-maximizing quantity (where MR = MC).

Locate this quantity on the demand curve to find the corresponding price.

Remember: In monopoly, price is set above MC, at the demand curve for the chosen quantity.

Read the price value from the vertical axis at the profit-maximizing quantity.

Try solving on your own before revealing the answer!

Final Answer: $6.5

At Quantity = 8, the price on the demand curve is $6.5, which is the monopolist's profit-maximizing price.

Q3. Suppose the market demand is given by . What is the marginal revenue function facing a monopolist?

Background

Topic: Marginal Revenue for Monopoly

This question tests your ability to derive the marginal revenue function from a linear demand function.

Key Terms and Formulas:

Market Demand:

Inverse Demand:

Total Revenue:

Marginal Revenue:

Step-by-Step Guidance

Start by finding the inverse demand function: Solve for in terms of .

Express total revenue as .

Expand and differentiate with respect to to find .

Simplify the expression to get the marginal revenue function.

Try solving on your own before revealing the answer!

Final Answer:

After deriving the inverse demand and differentiating, the marginal revenue function is .

Q4. The market demand is given by . A monopolist has a short-run cost function . Then the monopolist’s profit-maximizing output level is ______.

Background

Topic: Monopoly Profit Maximization with Cost Function

This question tests your ability to set up and solve the profit-maximizing condition for a monopolist with a quadratic cost function.

Key Terms and Formulas:

Profit Function:

Inverse Demand:

Cost Function:

First Order Condition:

Step-by-Step Guidance

Write the profit function: .

Expand and simplify the profit function.

Take the derivative with respect to and set it equal to zero to find the profit-maximizing output.

Solve the resulting equation for .

Try solving on your own before revealing the answer!

Final Answer:

Solving the first order condition yields as the profit-maximizing output.

Q5. Suppose there are 100 identical firms in the competitive market, and each has a supply curve of . Then the market supply curve is ____.

Background

Topic: Market Supply in Perfect Competition

This question tests your understanding of how to aggregate individual firm supply curves to obtain the market supply curve.

Key Terms and Formulas:

Individual Supply Curve:

Market Supply Curve:

Step-by-Step Guidance

Recognize that the market supply is the sum of all individual supply curves.

Multiply the individual supply curve by the number of firms: .

Simplify the expression to get the market supply curve.

Try solving on your own before revealing the answer!

Final Answer:

The market supply curve is .

Q6. In a competitive market, the demand and supply curves are and respectively. What is the price in the competitive equilibrium?

Background

Topic: Competitive Market Equilibrium

This question tests your ability to find the equilibrium price where market demand equals market supply.

Key Terms and Formulas:

Demand Curve:

Supply Curve:

Equilibrium Condition:

Step-by-Step Guidance

Set the demand and supply equations equal to each other: .

Combine like terms and solve for .

Check your solution to ensure it satisfies both equations.

Try solving on your own before revealing the answer!

Final Answer:

The equilibrium price is .

Q7. Consider a firm with production function . Assume that capital is fixed at . The rental rate of capital is and the wage rate of labor is . The cost of production is the total expenditure on capital and labor. Then the cost of producing units is _______.

Background

Topic: Cost Functions and Production

This question tests your ability to derive the cost function for a firm given a production function and input prices.

Key Terms and Formulas:

Production Function:

Cost Function:

Input Prices: ,

Step-by-Step Guidance

Set (fixed) and solve for in terms of : .

Plug and into the cost function: .

Simplify the expression to get the cost function in terms of .

Try solving on your own before revealing the answer!

Final Answer:

The cost function is .

Q8. A production function exhibits ______.

Background

Topic: Returns to Scale

This question tests your understanding of how to determine returns to scale from a Cobb-Douglas production function.

Key Terms and Formulas:

Returns to Scale: How output changes when all inputs are scaled by the same proportion.

Cobb-Douglas Function:

Step-by-Step Guidance

Double both inputs: .

Calculate the new output: .

Simplify the exponents: .

Compare the new output to the original: If output doubles, returns to scale are constant.

Try solving on your own before revealing the answer!

Final Answer: Constant returns to scale

Doubling both inputs doubles output, so the function exhibits constant returns to scale.

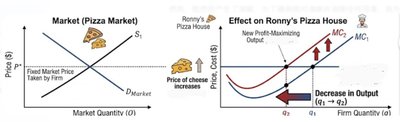

Q9. Ronny's Pizza House operates in the perfectly competitive local pizza market. If the price of cheese increases, what is the expected impact on Ronny's profit-maximizing output decision?

Background

Topic: Cost Shocks in Perfect Competition

This question tests your understanding of how input price changes affect a firm's marginal cost and output decision in a competitive market.

Key Terms and Formulas:

Marginal Cost (MC): The cost of producing one more unit.

Profit Maximization in Competition:

Cost Shock: Increase in input price shifts MC upward.

Step-by-Step Guidance

Recognize that an increase in cheese price raises the cost of each pizza, shifting the MC curve upward.

In perfect competition, the firm produces where .

With MC higher, the intersection with the fixed market price occurs at a lower quantity.

Thus, the firm's profit-maximizing output decreases.

Try solving on your own before revealing the answer!

Final Answer: Output decreases because the marginal cost curve shifts upward.

Higher input costs raise MC, so the firm produces less.

Q10. If a legal service offers personalized pricing so that it charges each customer their willingness to pay. This is a practice of ______.

Background

Topic: Price Discrimination

This question tests your understanding of the types of price discrimination in microeconomics.

Key Terms and Formulas:

First-degree price discrimination: Charging each customer their exact willingness to pay.

Second-degree price discrimination: Charging different prices based on quantity purchased.

Third-degree price discrimination: Charging different prices to different groups.

Step-by-Step Guidance

Identify the practice: Personalized pricing for each customer.

Recall the definitions of the three degrees of price discrimination.

Match the practice to the correct degree.

Try solving on your own before revealing the answer!

Final Answer: First-degree price discrimination

Charging each customer their willingness to pay is first-degree price discrimination.

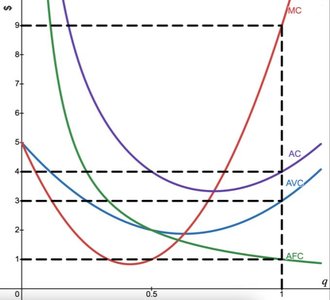

Q11. True or False: When the market price is $1, the competitive firm should shut down in the short run.

Background

Topic: Shutdown Decision in the Short Run

This question tests your understanding of the shutdown rule for competitive firms in the short run.

Key Terms and Formulas:

Average Variable Cost (AVC): The average cost of variable inputs per unit.

Shutdown Rule: Firm should shut down if .

Step-by-Step Guidance

Check the market price () against the AVC curve.

If is below AVC at all output levels, the firm should shut down.

Use the graph to compare and AVC.

Try solving on your own before revealing the answer!

Final Answer: True

Since is below AVC everywhere, the firm should shut down.

Q12. When the market price $9, this competitive firm’s maximized profit level is ________.

Background

Topic: Profit Calculation in Perfect Competition

This question tests your ability to calculate profit given price, output, and cost curves.

Key Terms and Formulas:

Profit:

Supply Rule: Firm produces where .

Average Cost (AC): Total cost per unit at the chosen output.

Step-by-Step Guidance

Find the output where intersects the MC curve (from the graph).

At this output, read the AC value from the graph.

Calculate profit: .

Set up the calculation but stop before computing the final value.

Try solving on your own before revealing the answer!

Final Answer: 5

At , , so profit is .

Q13. Suppose the cost function for a competitive orange juice producer is . This firm’s supply curve is _______.

Background

Topic: Supply Curve Derivation

This question tests your ability to derive the supply curve from a cost function in a competitive market.

Key Terms and Formulas:

Cost Function:

Marginal Cost (MC):

Supply Rule:

Step-by-Step Guidance

Differentiate the cost function to find .

Set to find the supply curve.

Solve for in terms of .

Try solving on your own before revealing the answer!

Final Answer:

The supply curve is .

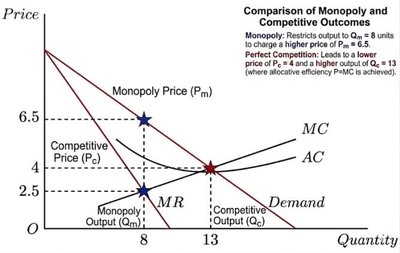

Q14. A monopolist sells at a price ____ the competitive equilibrium price and sells _____ the competitive equilibrium output level.

Background

Topic: Monopoly vs. Perfect Competition

This question tests your understanding of the differences in price and output between monopoly and competitive markets.

Key Terms and Formulas:

Monopoly Price: Higher than competitive price.

Monopoly Output: Lower than competitive output.

Competitive Equilibrium: at higher output.

Step-by-Step Guidance

Compare the monopoly and competitive equilibrium points on the graph.

Note the price and quantity at each equilibrium.

Monopoly restricts output to raise price above competitive levels.

Try solving on your own before revealing the answer!

Final Answer: Higher than, less than

Monopolists charge a higher price and produce less output than in perfect competition.