Back

BackMicroeconomics: First Principles and Individual Choice

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Economics

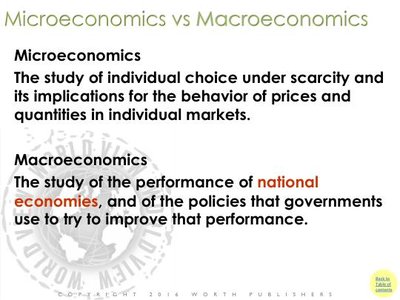

Microeconomics vs. Macroeconomics

Economics is the study of how individuals and societies allocate scarce resources. It is divided into two main branches: microeconomics and macroeconomics.

Microeconomics: The study of individual choice under scarcity and its implications for the behavior of prices and quantities in individual markets.

Macroeconomics: The study of the performance of national economies and the policies that governments use to improve that performance.

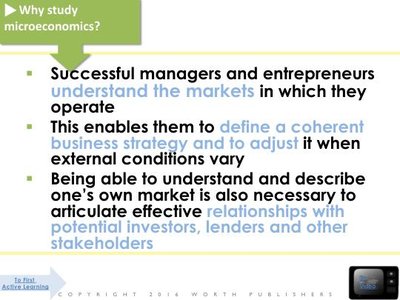

Why Study Microeconomics?

Understanding microeconomics is essential for managers, entrepreneurs, and anyone who needs to make informed decisions in markets. It helps in:

Understanding how markets operate

Defining and adjusting business strategies

Articulating effective relationships with investors, lenders, and stakeholders

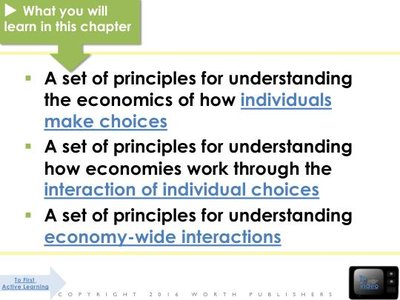

Learning Objectives

This chapter introduces the foundational principles for understanding:

How individuals make choices

How economies function through the interaction of individual choices

Economy-wide interactions

First Principles of Individual Choice

Choice: The Heart of Economics

Economics centers on the concept of choice. Every decision made by individuals or firms involves selecting among alternatives, and these choices affect others in the economy.

Principle 1: Choices Are Necessary Because Resources Are Scarce

Scarcity means that resources are limited and cannot satisfy all human wants. Therefore, individuals and societies must make choices about how to allocate these resources.

Resource: Anything that can be used to produce something else (e.g., land, labor, capital).

Scarce: A resource is scarce when there is not enough of it to satisfy all the ways society wants to use it.

Principle 2: The True Cost of Something Is Its Opportunity Cost

Every choice involves a cost—the value of the next best alternative forgone. This is known as opportunity cost.

Opportunity Cost: What you must give up in order to get something.

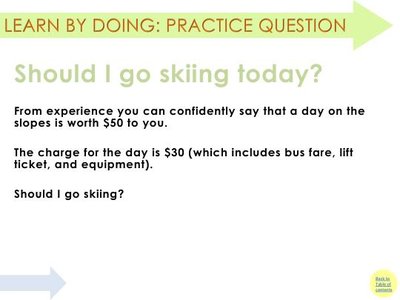

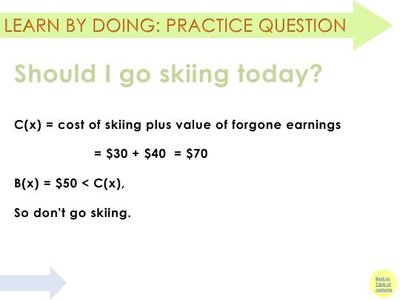

Example: Should I Go Skiing Today?

Suppose a day of skiing is worth $50 to you, and the cost is $30. Should you go skiing?

If you have no other alternatives, the benefit ($50) exceeds the cost ($30), so you should go skiing.

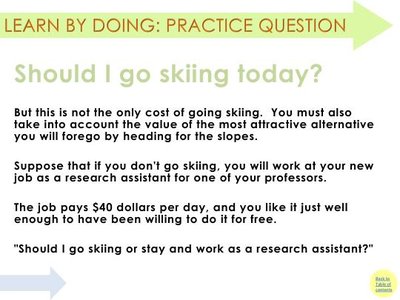

However, if you could earn $40 by working instead, the opportunity cost of skiing is $30 (skiing) + $40 (forgone earnings) = $70.

Since $50 < $70, you should not go skiing.

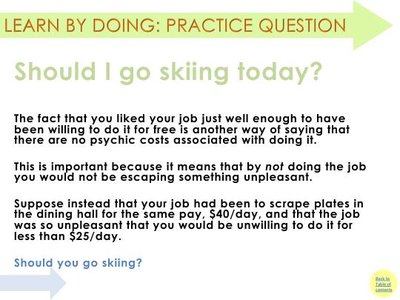

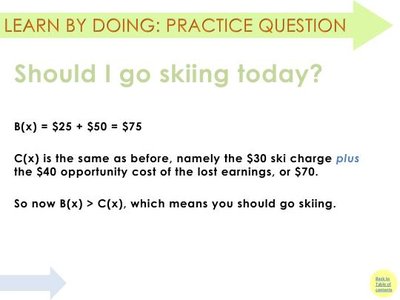

If the alternative job is unpleasant and you would only do it for $25/day, then the benefit of skiing ($50) plus the minimum compensation for the unpleasant job ($25) is $75, which exceeds the cost of skiing ($70). In this case, you should go skiing.

Principle 3: "How Much" Is a Trade-Off—A Decision at the Margin

Many decisions are not all-or-nothing but involve choosing "how much" to do of something. These are called marginal decisions and involve weighing the additional (marginal) benefits and costs.

Trade-off: Comparison of the costs and benefits of doing something.

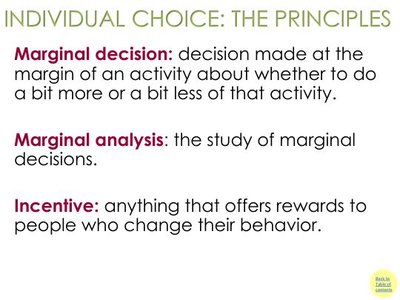

Marginal Decision: Decision made at the margin about whether to do a bit more or a bit less of an activity.

Marginal Analysis: The study of marginal decisions.

Incentive: Anything that offers rewards to people who change their behavior.

Economic Surplus and Decision Making

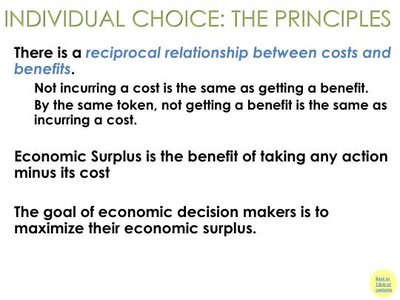

There is a reciprocal relationship between costs and benefits. Economic surplus is the benefit of taking any action minus its cost. The goal of economic decision makers is to maximize their economic surplus.

Not incurring a cost is the same as getting a benefit.

Not getting a benefit is the same as incurring a cost.

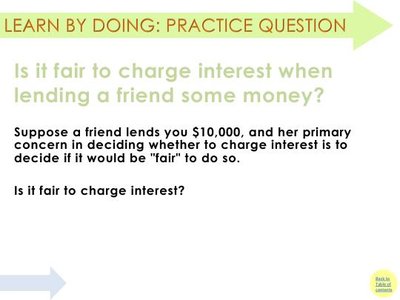

Practice Question: Is It Fair to Charge Interest When Lending Money?

Suppose a friend lends you $10,000. Is it fair for her to charge interest?

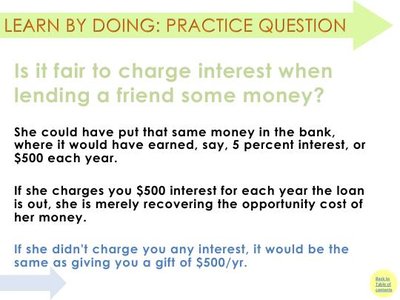

If she could have earned 5% interest ($500/year) by putting the money in the bank, charging you $500/year in interest simply recovers her opportunity cost.

If she charges no interest, it is equivalent to giving you a $500/year gift.

Key Terms and Concepts

Resource: Anything used to produce something else.

Scarcity: Limited availability of resources.

Opportunity Cost: Value of the next best alternative forgone.

Trade-off: Balancing costs and benefits.

Marginal Decision: Decision about doing a little more or less of an activity.

Marginal Analysis: Study of marginal decisions.

Incentive: Reward for changing behavior.

Economic Surplus: Benefit of an action minus its cost.

Formulas

Opportunity Cost Formula:

Economic Surplus Formula:

Marginal Analysis:

where is marginal benefit and is marginal cost.