Back

BackMicroeconomics: Foundations and Models – Chapter 1 Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economics: Foundations and Models

Three Key Economic Ideas

Economics is the study of how people make choices to attain their goals, given their scarce resources. Three foundational ideas guide economic analysis:

People are rational: Individuals use all available information to achieve their objectives, weighing costs and benefits to make optimal decisions.

People respond to economic incentives: Changes in incentives alter behavior, as seen in policy impacts or market changes.

Optimal decisions are made at the margin: Most choices involve incremental adjustments, analyzed through marginal cost and marginal benefit.

Example: Apple sets iPhone prices to maximize profit, not randomly. Marginal analysis helps decide whether to study an extra hour or watch TV.

The Economic Problem That Every Society Must Solve

Scarcity means limited resources must be allocated efficiently. Every society must answer:

What goods and services will be produced? Trade-offs are necessary; opportunity cost is the value of the next best alternative forgone.

How will goods and services be produced? Firms choose production methods based on costs and available technology.

Who will receive the goods and services produced? Distribution depends on income, government policy, and social goals.

Trade-off: Increasing production of one good requires reducing another due to resource scarcity.

Centrally Planned Economies vs. Market Economies

Economic systems differ in how resources are allocated:

Centrally planned economy: Government decides allocation.

Market economy: Households and firms interact in markets to allocate resources.

Mixed economy: Combines market mechanisms with government intervention.

The U.S. is best described as a mixed economy, with significant government involvement.

Efficiency and Equity in Market Economies

Market economies promote:

Productive efficiency: Goods produced at lowest cost.

Allocative efficiency: Production matches consumer preferences; marginal benefit equals marginal cost.

Voluntary exchange ensures both buyers and sellers benefit. However, markets may not always be fully efficient or equitable.

Equity: Refers to fair distribution of economic benefits, often requiring trade-offs with efficiency.

Economic Models

Economists use models—simplified representations of reality—to analyze events and policies. Model-building involves:

Deciding on assumptions

Formulating testable hypotheses

Using data to test hypotheses

Revising models as needed

Assumptions: Models require simplifications, such as assuming consumers maximize well-being and firms maximize profit.

Hypothesis: A statement about an economic variable, often concerning causality.

Statistical methods are used to test hypotheses, but establishing causality can be challenging.

Positive vs. Normative Analysis

Economics distinguishes between:

Positive analysis: What is (objective, fact-based)

Normative analysis: What ought to be (subjective, value-based)

Most economic research is positive, but policy decisions often require normative judgments.

Microeconomics vs. Macroeconomics

Economics is divided into two main branches:

Microeconomics: Studies individual households, firms, and markets.

Macroeconomics: Studies the economy as a whole, including inflation, unemployment, and growth.

Economic Skills and Careers

Studying economics develops analytical skills valuable in many careers, including business, government, and academia. Economics majors often earn higher salaries, though causation versus correlation is debated.

Important Economic Terms

Key terms include:

Scarcity: Unlimited wants, limited resources

Opportunity cost: Value of the next best alternative

Technology: Processes used to produce goods/services

Capital: Manufactured goods used in production

Appendix: Using Graphs and Formulas

Graphs in Economics

Graphs are essential tools for visualizing economic relationships. Common types include:

Bar graphs: Compare quantities across categories

Pie charts: Show proportions of a whole

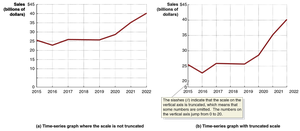

Time-series graphs: Track variables over time

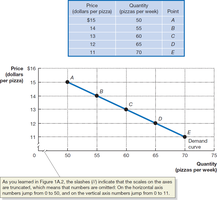

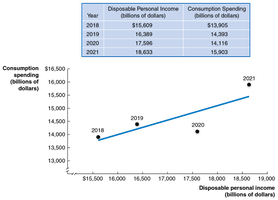

Plotting Price and Quantity

Price and quantity relationships are often plotted on two-dimensional grids. Each point represents a price-quantity combination, and connecting points illustrates the relationship.

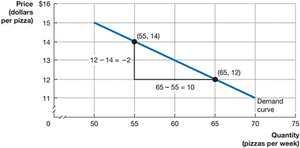

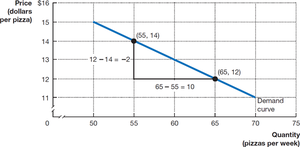

Calculating the Slope of a Line

The slope of a line is calculated as the change in the y-axis variable divided by the change in the x-axis variable. For a demand curve:

Slope formula:

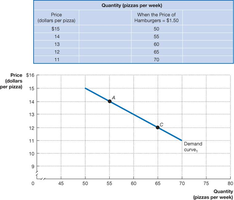

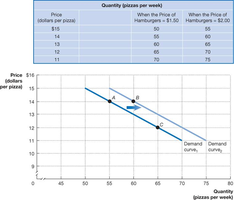

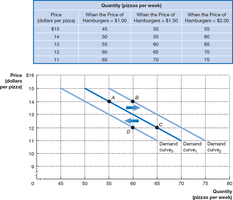

Showing Three Variables on a Graph

Graphs can illustrate how a third variable affects the relationship between two others, such as how the price of hamburgers affects pizza demand.

Positive and Negative Relationships

A positive relationship means both variables increase together; a negative relationship means one increases as the other decreases.

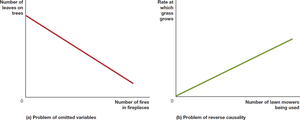

Cause and Effect in Graphs

Graphs can be misleading regarding causality. Omitted variables or reverse causality can distort conclusions.

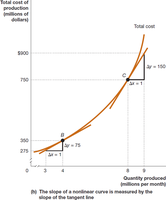

Linear vs. Nonlinear Relationships

Most economic relationships are not perfectly linear. Nonlinear curves have varying slopes at different points, which can be approximated or measured with tangent lines.

Percentage Change Formula

Percentage change measures the change in a variable from one period to another:

Formula:

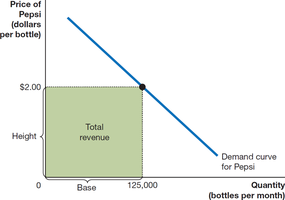

Graphing Total Revenue

Total revenue is the product of price and quantity, represented as the area of a rectangle on a graph.

Formula:

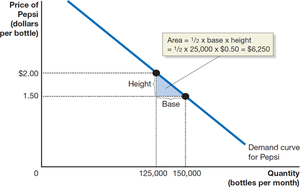

Area of a Triangle

The area of a triangle is useful in economic analysis, such as calculating consumer or producer surplus:

Formula:

Summary of Using Formulas

When applying formulas in economics:

Understand the concept the formula represents

Use the correct formula for the problem

Check that the result is economically reasonable