Back

BackMicroeconomics Practice: Production Possibilities, Opportunity Cost, and Market Concepts

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Q1. Which of the following is NOT considered a "factor of production" in economics?

Background

Topic: Factors of Production

This question tests your understanding of the basic resources used in the production of goods and services in economics.

Key Terms:

Factors of Production: The resources used to produce goods and services, typically classified as land, labor, capital, and entrepreneurship.

Goods: Finished products that are consumed.

Step-by-Step Guidance

Review the definition of each factor of production: land (natural resources), labor (human effort), capital (machinery, tools), and entrepreneurship (risk-taking and innovation).

Examine each option and determine whether it fits into one of these categories.

Identify which option is a finished good rather than a resource used in production.

Try solving on your own before revealing the answer!

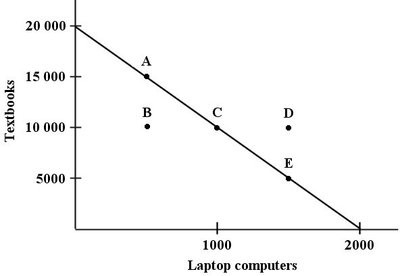

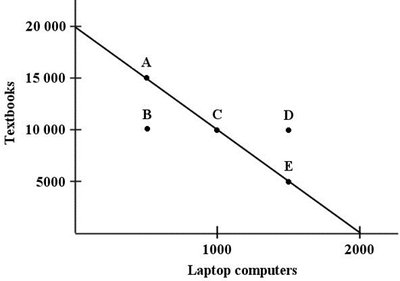

Q3. Refer to Figure 1-2. For the school board, what is the opportunity cost of one additional laptop computer?

Background

Topic: Opportunity Cost and Production Possibilities

This question tests your ability to calculate opportunity cost using a production possibilities frontier (PPF).

Key Terms and Formula:

Opportunity Cost: The value of the next best alternative foregone when making a choice.

Production Possibilities Frontier (PPF): A curve showing the maximum combinations of two goods that can be produced with available resources.

Key Formula:

Step-by-Step Guidance

Identify the maximum number of textbooks and laptops that can be purchased with the budget (from the endpoints of the PPF).

Calculate how many textbooks must be given up to obtain one more laptop (use the slope of the PPF).

Set up the opportunity cost calculation using the formula above.

Try solving on your own before revealing the answer!

Q4. Refer to Figure 1-2. Which of the following combinations of textbooks and laptops is unaffordable, given the school board's budget of $500,000?

Background

Topic: Feasibility and Budget Constraints

This question tests your ability to interpret a PPF and identify which combinations are attainable given a fixed budget.

Key Terms:

Budget Constraint: The limit on the consumption bundles that a consumer (or organization) can afford.

Feasible Combination: Any point on or inside the PPF.

Unaffordable Combination: Any point outside the PPF.

Step-by-Step Guidance

Examine the graph and identify which points (A, B, C, D, E) lie on, inside, or outside the PPF.

Recall that only points on or inside the PPF are affordable with the given budget.

Determine which point(s) are outside the PPF, indicating unaffordability.

Try solving on your own before revealing the answer!

Q5. Refer to Figure 1-2. What is the price of a laptop computer in this example?

Background

Topic: Unit Cost Calculation

This question tests your ability to calculate the price per unit given a total budget and the maximum quantity that can be purchased.

Key Formula:

Step-by-Step Guidance

Identify the total budget available for laptops and the maximum number of laptops that can be purchased.

Set up the calculation using the formula above.

Divide the total budget by the number of laptops to find the unit price.

Try solving on your own before revealing the answer!

Q8. What is an inferior good?

Background

Topic: Types of Goods and Income Effects

This question tests your understanding of how demand for certain goods changes with household income.

Key Terms:

Inferior Good: A good for which demand decreases as income increases.

Normal Good: A good for which demand increases as income increases.

Step-by-Step Guidance

Recall the definitions of normal and inferior goods.

Consider how demand for an inferior good changes when household income rises.

Identify the answer choice that matches the definition of an inferior good.

Try solving on your own before revealing the answer!

Q9. Consider butter and margarine, which are substitutes. When the price of butter falls, the demand curve for margarine is likely to:

Background

Topic: Substitutes and Demand Shifts

This question tests your understanding of how the demand for one good changes when the price of a substitute changes.

Key Terms:

Substitute Goods: Goods that can replace each other in consumption.

Demand Curve Shift: A change in demand at every price, represented by a shift of the curve.

Step-by-Step Guidance

Recall what happens to the demand for a good when the price of its substitute falls.

Think about consumer behavior: if butter becomes cheaper, what happens to the demand for margarine?

Identify which direction the demand curve for margarine will shift.

Try solving on your own before revealing the answer!

Q11. Suppose that some resource X is necessary to produce some good Y. If the price of X falls, what happens?

Background

Topic: Input Prices and Supply

This question tests your understanding of how changes in input prices affect the supply of a good.

Key Terms:

Input (Resource): A factor used in the production of goods or services.

Supply Curve: Shows the relationship between price and quantity supplied.

Step-by-Step Guidance

Recall how a decrease in the price of an input affects the cost of producing the final good.

Think about whether this change would shift the supply curve for the final good, and in which direction.

Eliminate answer choices that do not relate to the supply of the final good.

Try solving on your own before revealing the answer!

Q15. Suppose that supply for some good increases and that simultaneously the demand for the same good decreases. The result would be:

Background

Topic: Simultaneous Shifts in Supply and Demand

This question tests your ability to predict changes in equilibrium price (P) and quantity (Q) when both supply and demand curves shift.

Key Terms:

Equilibrium Price (P): The price at which quantity supplied equals quantity demanded.

Equilibrium Quantity (Q): The quantity bought and sold at the equilibrium price.

Step-by-Step Guidance

Recall what happens to equilibrium price and quantity when supply increases (holding demand constant).

Recall what happens when demand decreases (holding supply constant).

Combine the effects to determine the overall impact on price and quantity.

Remember that one effect may be indeterminate without more information.

Try solving on your own before revealing the answer!

Q16. Suppose that in Montreal in December, 2018, 10,000 ski helmets were sold at a price of $60 each. And in Montreal in December, 2019, 20,000 ski helmets were sold at a price of $80 each. One possible explanation for the change is that, ceteris paribus, from 2018 to 2019 the ________ curve for ski helmets shifted to the ________.

Background

Topic: Shifts in Supply and Demand

This question tests your ability to interpret changes in equilibrium price and quantity and relate them to shifts in supply or demand.

Key Terms:

Demand Curve: Shows the relationship between price and quantity demanded.

Supply Curve: Shows the relationship between price and quantity supplied.

Ceteris Paribus: All other things held constant.

Step-by-Step Guidance

Note the changes in both price and quantity from 2018 to 2019.

Recall what happens to equilibrium price and quantity when demand increases versus when supply increases.

Determine which curve must have shifted, and in which direction, to explain both a higher price and higher quantity.

Try solving on your own before revealing the answer!

Q19. If the price elasticity of demand is 1.2, then a 10% increase in price results in a:

Background

Topic: Price Elasticity of Demand

This question tests your ability to apply the concept of price elasticity to predict changes in quantity demanded.

Key Formula:

Step-by-Step Guidance

Recall the formula for price elasticity of demand and what the value 1.2 means (elastic demand).

Set up the equation using the given elasticity and the percentage change in price.

Solve for the percentage change in quantity demanded (but do not calculate the final value yet).

Try solving on your own before revealing the answer!

Q21. If two goods, X and Y, have a positive cross elasticity of demand, then we know that they:

Background

Topic: Cross Elasticity of Demand

This question tests your understanding of the relationship between goods based on cross elasticity.

Key Terms:

Cross Elasticity of Demand: Measures how the quantity demanded of one good responds to a change in the price of another good.

Substitutes: Goods with positive cross elasticity.

Complements: Goods with negative cross elasticity.

Step-by-Step Guidance

Recall the definition of cross elasticity and what a positive value indicates about the relationship between two goods.

Identify which answer choice correctly describes this relationship.

Try solving on your own before revealing the answer!

Q22. If a price ceiling is in place and if the demand curve for the product shifts rightward, one consequence would be:

Background

Topic: Price Ceilings and Market Outcomes

This question tests your understanding of how government-imposed price controls interact with shifts in demand.

Key Terms:

Price Ceiling: A legal maximum price set below equilibrium.

Excess Demand (Shortage): When quantity demanded exceeds quantity supplied at the ceiling price.

Step-by-Step Guidance

Recall what happens when a price ceiling is set below equilibrium price.

Consider the effect of an increase in demand on the quantity exchanged and the amount of excess demand.

Identify which outcome is most likely given the new market conditions.

Try solving on your own before revealing the answer!

Q23. If a price floor is in place and if the demand curve for the product shifts rightward, one consequence would be:

Background

Topic: Price Floors and Market Outcomes

This question tests your understanding of how price floors interact with shifts in demand.

Key Terms:

Price Floor: A legal minimum price set above equilibrium.

Excess Supply (Surplus): When quantity supplied exceeds quantity demanded at the floor price.

Step-by-Step Guidance

Recall what happens when a price floor is set above equilibrium price.

Consider the effect of an increase in demand on the quantity exchanged and the amount of excess supply.

Identify which outcome is most likely given the new market conditions.

Try solving on your own before revealing the answer!