Back

BackMicroeconomics Study Guide: Externalities, Public Goods, and Elasticity

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Externalities, Economic Efficiency, and Government Policy

Externalities and Economic Efficiency

Externalities occur when the actions of producers or consumers affect others who are not directly involved in the transaction. These effects can be either positive or negative, leading to market outcomes that are not economically efficient.

Externality: A side-effect of production or consumption that impacts third parties.

Private Cost: The cost incurred by the producer.

Social Cost: The total cost, including both private and external costs (e.g., pollution).

Economic Efficiency: Achieved when Marginal Social Cost = Marginal Social Benefit.

Market Failure: Occurs when the market does not allocate resources efficiently, often due to incomplete property rights or difficulty enforcing them.

Example: Pollution is a negative externality where the social cost exceeds the private cost, requiring regulatory intervention.

Government Intervention in Externalities

Governments intervene to correct inefficiencies caused by externalities, typically through taxes (for negative externalities) or subsidies (for positive externalities).

Negative Externality: Tax imposed to internalize the external cost.

Positive Externality: Subsidy provided to encourage beneficial activities.

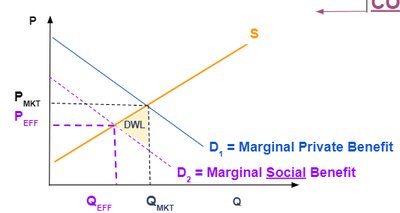

Deadweight Loss (DWL): The reduction in economic surplus due to market inefficiency.

Key Graph Terms:

PMKT: Market price before externality correction.

PEFF: Efficient price after correction.

QMKT: Market quantity before correction.

QEFF: Efficient quantity after correction.

Types of Externalities and Government Response

Externalities can be classified based on their impact and the target audience:

Negative Externality (Producer): Tax, reduces quantity.

Negative Externality (Consumer): Tax, reduces quantity.

Positive Externality (Producer): Subsidy, increases quantity.

Positive Externality (Consumer): Subsidy, increases quantity.

Efficient Pollution Level: Achieved when the marginal benefit of reducing emissions equals the marginal cost.

Private Solutions: The Coase Theorem

The Coase Theorem suggests that private parties can resolve externalities through bargaining, provided property rights are well-defined and transaction costs are low.

Conditions: Clear property rights, low transaction costs, full information.

Result: Efficient outcome without government intervention.

Government Policies: Taxes, Command-and-Control, and Cap-and-Trade

Governments use various policies to address externalities:

Taxes: Imposed to internalize negative externalities.

Subsidies: Provided to encourage positive externalities.

Command-and-Control: Direct regulations, such as emission limits or required technology.

Cap-and-Trade: Allowances for emissions that can be traded among firms.

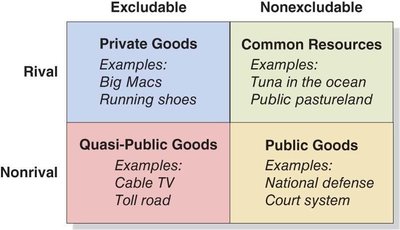

Four Categories of Goods

Classification of Goods

Goods are classified based on their excludability and rivalry:

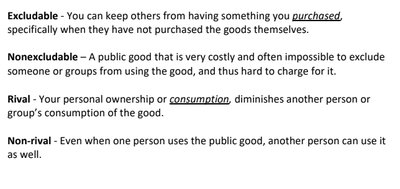

Excludable: Access can be restricted to those who pay.

Nonexcludable: Access cannot be easily restricted.

Rival: Consumption by one reduces availability for others.

Nonrival: Consumption by one does not reduce availability for others.

Elasticity: The Responsiveness of Demand and Supply

Price Elasticity of Demand

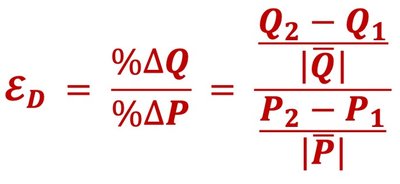

Price elasticity of demand measures how much the quantity demanded responds to a change in price.

Formula:

Elastic: (quantity changes more than price)

Inelastic: (quantity changes less than price)

Unit Elastic: (quantity changes equal to price)

Determinants of Price Elasticity of Demand

Several factors influence the price elasticity of demand:

Availability of substitutes

Time horizon (elasticity increases in the long run)

Luxury vs. necessity

Definition of the market

Share of budget

Elasticity and Total Revenue

The relationship between price elasticity and total revenue is crucial for firms:

Total Revenue:

Elastic demand: Price increase decreases total revenue.

Inelastic demand: Price increase increases total revenue.

Unit elastic: Price change does not affect total revenue.

Other Elasticities

Cross-Price Elasticity: Measures responsiveness of demand for one good to the price change of another.

Income Elasticity: Measures responsiveness of demand to changes in income.

Price Elasticity of Supply

Price elasticity of supply measures how much the quantity supplied responds to a change in price.

Formula:

Elastic supply:

Inelastic supply:

Unit elastic supply:

Time is the most important determinant (supply is more elastic in the long run).

Summary Table: Four Categories of Goods

Excludable | Nonexcludable | |

|---|---|---|

Rival | Private Goods Examples: Big Macs, Running shoes | Common Resources Examples: Tuna in the ocean, Public pastureland |

Nonrival | Quasi-Public Goods Examples: Cable TV, Toll road | Public Goods Examples: National defense, Court system |