Back

BackMicroeconomics Study Guide: Input Markets, Monopoly, Oligopoly, and Monopolistic Competition

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Input Demand: The Labor and Land Markets

Derived Demand and Marginal Revenue Product of Labor (MRPL)

In microeconomics, the demand for inputs such as labor and land is derived from the demand for the final goods and services produced. The Marginal Revenue Product of Labor (MRPL) is a key concept, defined as the additional revenue generated from employing one more unit of labor:

MRPL = MPL × PX, where MPL is the marginal product of labor and PX is the price of the product.

As more labor is hired, MRPL diminishes due to diminishing MPL.

The profit-maximizing level of labor in the short run is where MRPL = W (wage rate).

Profit-Maximizing Input Allocation with Multiple Inputs

When firms use more than one variable input (e.g., labor and capital), the allocation of resources must be optimized:

The profit-maximizing condition is: where MPL and MPK are the marginal products of labor and capital, and PL and PK are their prices.

If , the firm should use more labor and less capital until equality is achieved.

Market Structures: Perfect Competition, Monopoly, Oligopoly, and Monopolistic Competition

Perfect Competition

Perfect competition is characterized by many sellers offering identical products. Firms are price takers and have no market power:

The demand curve facing an individual firm is perfectly elastic (horizontal at market price).

Profit-maximizing condition: P = MR = MC.

Free entry and exit in the long run ensures zero economic profit and efficient production at the lowest average total cost (ATC).

Monopoly

A monopoly exists when there is only one seller with no close substitutes. The monopolist has market power and is a price maker:

Barriers to entry are the main cause of monopolies.

Profit-maximizing output is where MR = MC, but price is set above marginal cost (P > MC).

Monopolists can earn positive economic profit in the long run.

Monopoly leads to higher prices and lower quantities compared to perfect competition, resulting in deadweight loss (DWL).

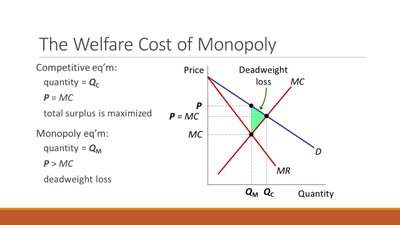

The Welfare Cost of Monopoly

Monopoly reduces total surplus and creates deadweight loss, as shown in the diagram below:

Competitive equilibrium: QC, P = MC, total surplus maximized.

Monopoly equilibrium: QM, P > MC, deadweight loss present.

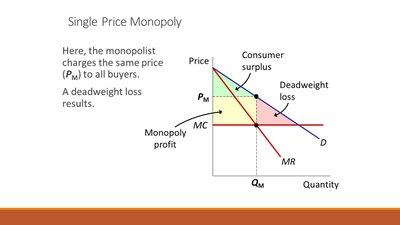

Single Price Monopoly

In a single price monopoly, the monopolist charges the same price to all buyers, resulting in consumer surplus, monopoly profit, and deadweight loss:

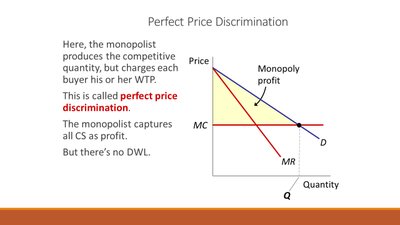

Perfect Price Discrimination

With perfect price discrimination, the monopolist charges each buyer their maximum willingness to pay, capturing all consumer surplus as profit and eliminating deadweight loss:

Oligopoly

An oligopoly is a market with a few sellers offering similar or identical products. Firms engage in strategic behavior, often analyzed using game theory:

High concentration ratio; firms may collude to act as a monopoly.

Collusion leads to monopoly quantity and price, but firms have incentives to cheat.

As the number of firms increases, the market outcome approaches perfect competition (P → MC).

Key concepts: dominant strategy, Nash equilibrium.

Monopolistic Competition

Monopolistic competition features many sellers offering differentiated products. Firms have some market power:

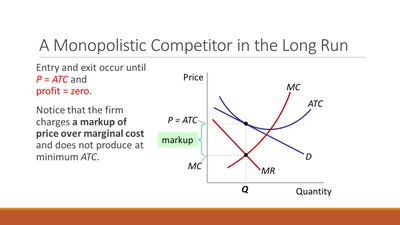

Short-run behavior resembles monopoly; long-run behavior resembles perfect competition due to free entry and exit.

Long-run equilibrium: P = ATC, profit = zero.

Firms do not produce at minimum ATC, resulting in excess capacity and markup of price over MC (P > MC).

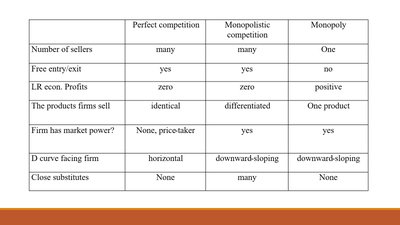

Comparison of Market Structures

Characteristics Table

The table below summarizes the main characteristics of perfect competition, monopolistic competition, and monopoly:

Perfect competition | Monopolistic competition | Monopoly | |

|---|---|---|---|

Number of sellers | many | many | One |

Free entry/exit | yes | yes | no |

LR econ. Profits | zero | zero | positive |

The products firms sell | identical | differentiated | One product |

Firm has market power? | None, price-taker | yes | yes |

D curve facing firm | horizontal | downward-sloping | downward-sloping |

Close substitutes | None | many | None |

Additional info: The notes and images together provide a comprehensive overview of input markets and the four main market structures, including their characteristics, profit-maximizing conditions, and welfare implications. This guide is suitable for exam preparation for microeconomics students.