Back

BackMicroeconomics Study Notes: Consumer Choice, Production, and Market Structures

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Consumer Choice and Utility Maximization

Utility and Marginal Utility

Utility is the satisfaction or enjoyment a consumer receives from consuming goods and services. Marginal utility (MU) is the additional utility gained from consuming one more unit of a good or service.

Total Utility (TU): The total satisfaction received from consuming a certain quantity of a good.

Marginal Utility (MU): The change in total utility from consuming an additional unit.

Law of Diminishing Marginal Utility: As more of a good is consumed, the additional satisfaction from each extra unit tends to decrease.

Formula:

Budget Constraint and Utility Maximization

Consumers face budget constraints due to limited income. The budget constraint shows all combinations of goods a consumer can afford.

Budget Constraint: The limited amount of income available to spend on goods and services.

Utility Maximization Rule: Consumers maximize utility when the marginal utility per dollar spent is equal across all goods, and the budget is exhausted.

Formulas:

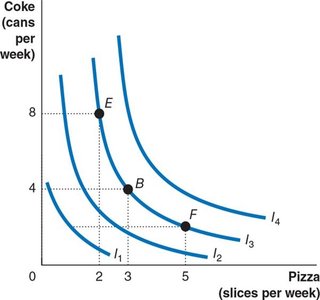

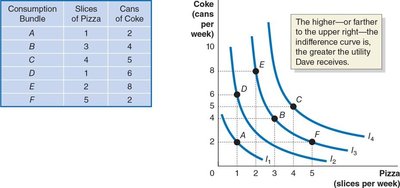

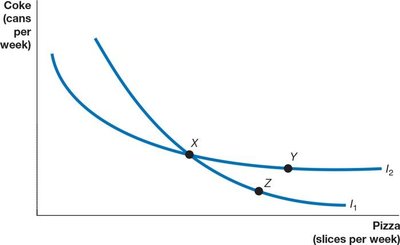

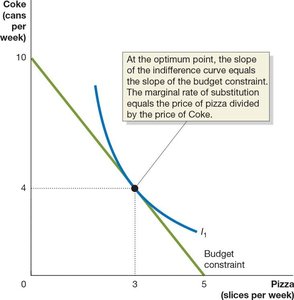

Indifference Curves and Marginal Rate of Substitution (MRS)

Indifference curves represent combinations of two goods that provide the same level of utility to the consumer. The marginal rate of substitution (MRS) is the rate at which a consumer is willing to trade one good for another while maintaining the same utility.

Indifference Curve: A curve showing all combinations of two goods that yield the same utility.

MRS: The slope of the indifference curve; the rate at which the consumer is willing to substitute one good for another.

Indifference curves are convex to the origin due to diminishing MRS.

Indifference curves cannot cross.

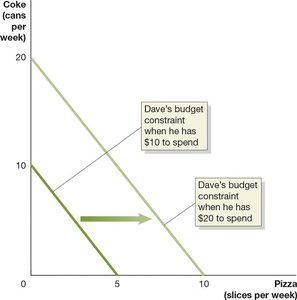

Budget Constraint and Consumer Equilibrium

The consumer's optimal choice occurs where the highest attainable indifference curve is tangent to the budget constraint. At this point, the MRS equals the ratio of the prices of the two goods.

Budget Line: Shows all combinations of two goods that can be purchased with a given income and prices.

Effect of Income Change: An increase in income shifts the budget line outward, allowing higher utility.

Consumer Equilibrium: The point where the budget line is tangent to an indifference curve.

Production and Costs

Technology and Production

Technology in economics refers to the process by which inputs are transformed into outputs. Technological change can be positive (improving productivity) or negative (reducing productivity).

Production Function: The relationship between inputs used and the maximum output that can be produced.

Short Run and Long Run

The short run is a period during which at least one input is fixed, while in the long run, all inputs can be varied.

Fixed Costs (FC): Costs that do not change with output.

Variable Costs (VC): Costs that change as output changes.

Total Cost (TC):

Cost Measures

Average Total Cost (ATC):

Average Fixed Cost (AFC):

Average Variable Cost (AVC):

Marginal Cost (MC):

Cost Curves

Cost curves illustrate the behavior of costs as output changes. ATC and AVC are typically U-shaped due to economies and diseconomies of scale. The MC curve intersects ATC and AVC at their minimum points.

Long-Run Costs

Economies of Scale: Long-run average costs decrease as output increases.

Constant Returns to Scale: Long-run average costs remain unchanged as output increases.

Diseconomies of Scale: Long-run average costs increase as output increases.

Perfect Competition

Characteristics of Perfect Competition

Many buyers and sellers

Identical products

No barriers to entry or exit

Firms are price takers

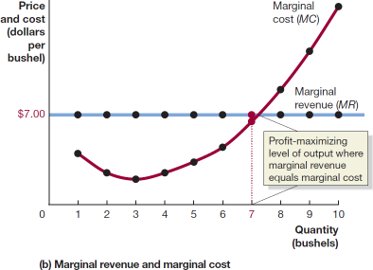

Profit Maximization

Firms maximize profit where marginal revenue (MR) equals marginal cost (MC). In perfect competition, price (P) equals MR and AR (average revenue).

Profit Maximization Rule:

For perfect competition:

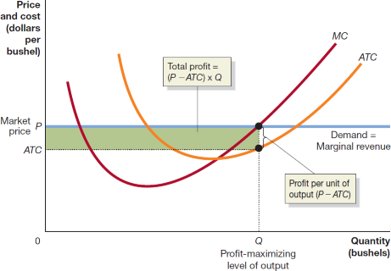

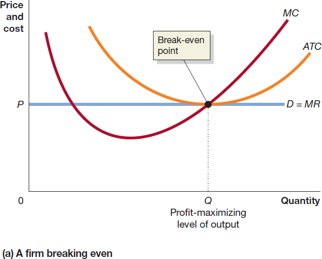

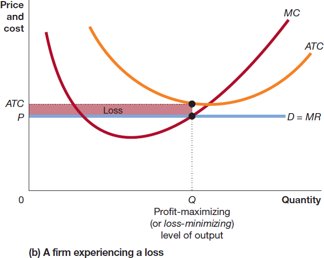

Profit, Loss, and Break-Even

Profit or loss is determined by comparing price and average total cost at the profit-maximizing output.

If , the firm makes a profit.

If , the firm breaks even.

If , the firm incurs a loss.

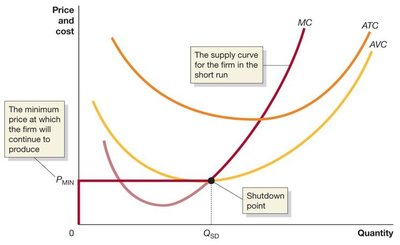

Short-Run Shutdown Decision

A firm should continue to produce in the short run if price covers average variable cost (AVC). If price falls below AVC, the firm should shut down.

If , produce where .

If , shut down (produce zero output).

Long-Run Equilibrium

In the long run, entry and exit of firms drive economic profit to zero. Firms produce at the minimum point of their long-run average cost curve, breaking even.

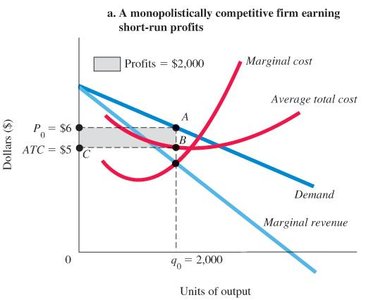

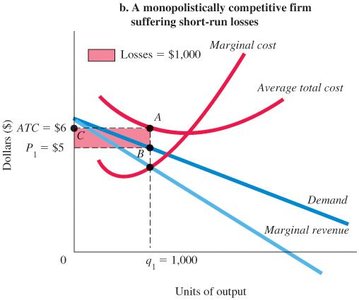

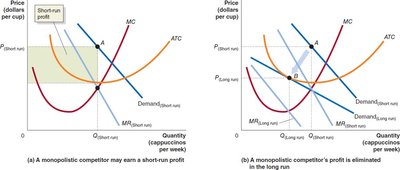

Monopolistic Competition

Characteristics

Many firms

Differentiated products

Low barriers to entry and exit

Profit Maximization

Monopolistically competitive firms maximize profit where MR = MC. In the short run, they may earn profits or losses.

Long-Run Adjustment

Entry of new firms (attracted by profits) shifts the demand curve for existing firms leftward, making demand more elastic and reducing profits to zero in the long run.

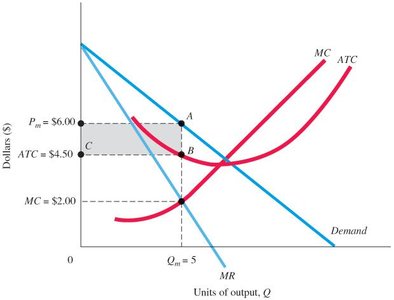

Monopoly

Characteristics

Single firm

Unique product with no close substitutes

Significant barriers to entry

Profit Maximization

A monopolist maximizes profit where MR = MC. The monopolist's demand curve is the market demand curve, which is downward sloping.