Back

BackChapter 13

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monopolistic Competition

Introduction to Monopolistic Competition

Monopolistic competition is a market structure that closely resembles perfect competition but incorporates product differentiation. It is prevalent in many modern economies, especially in industries where firms sell similar but not identical products. Understanding this model helps explain real-world market dynamics and the trade-offs between efficiency and variety.

Definition: Monopolistic competition is a market structure with many firms, low barriers to entry, and differentiated products.

Key Characteristics:

Many buyers and sellers

Selling similar, but not identical products (differentiated products/services)

No significant barriers to entry

Comparison to Perfect Competition:

Perfect competition: identical products, price takers, no barriers to entry

Monopolistic competition: differentiated products, price makers, no significant barriers to entry

Product Differentiation and Market Power

Product differentiation gives firms some control over pricing, making them price makers rather than price takers. The demand curve for each firm is downward sloping, reflecting the law of demand. However, due to the presence of many substitutes, the demand is relatively price elastic.

Market Power: Firms have market power if they can set prices above marginal cost ().

Economic Efficiency: Monopolistic competition results in a loss of economic efficiency compared to perfect competition, as firms are not allocatively efficient ().

Consumer Trade-Off: Consumers are willing to pay higher prices for products that better suit their preferences, trading off efficiency for variety.

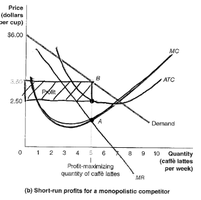

Demand and Marginal Revenue in Monopolistic Competition

In monopolistic competition, the demand curve is not perfectly elastic. Firms must lower prices to sell more units, causing the marginal revenue (MR) curve to lie below the demand curve and have twice its slope. Price no longer equals MR ().

Marginal Revenue: MR decreases faster than price due to the price and output effects.

Profit Maximization Rule: Firms maximize profit where MR = MC.

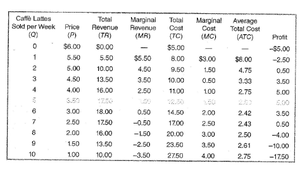

Elasticity of Demand

The elasticity of demand changes depending on the price range. When price decreases and total revenue increases, demand is elastic. When price decreases and total revenue falls, demand is inelastic.

Elastic Range: Price between $6 and $3; TR increases as P decreases.

Inelastic Range: Price below $3; TR decreases as P decreases.

Caffe Lattes Sold per Week (Q) | Price (P) | Total Revenue (TR) | Marginal Revenue (MR) | Total Cost (TC) | Marginal Cost (MC) | Average Total Cost (ATC) | Profit |

|---|---|---|---|---|---|---|---|

0 | $6.00 | $0.00 | - | $5.00 | - | $6.00 | -$5.00 |

1 | $5.50 | $5.50 | $5.50 | $8.00 | $3.00 | $8.00 | -$2.50 |

2 | $5.00 | $10.00 | $4.50 | $9.50 | $1.50 | $4.75 | $0.50 |

3 | $4.50 | $13.50 | $3.50 | $10.50 | $1.00 | $3.50 | $3.00 |

4 | $4.00 | $16.00 | $2.50 | $11.00 | $0.50 | $2.75 | $5.00 |

5 | $3.50 | $17.50 | $1.50 | $11.50 | $0.50 | $2.30 | $6.00 |

6 | $3.00 | $18.00 | $0.50 | $12.00 | $0.50 | $2.00 | $6.00 |

7 | $2.50 | $17.50 | -$0.50 | $12.50 | $0.50 | $1.79 | $5.00 |

8 | $2.00 | $16.00 | -$1.50 | $13.00 | $0.50 | $1.63 | $3.00 |

9 | $1.50 | $13.50 | -$2.50 | $13.50 | $0.50 | $1.50 | $0.00 |

10 | $1.00 | $10.00 | -$3.50 | $13.75 | $0.25 | $1.38 | -$1.75 |

Profit Maximization in Monopolistic Competition

Firms in monopolistic competition maximize profits by producing the quantity where MR = MC. The price is determined by the demand curve at this quantity, and the average total cost (ATC) is determined by the ATC curve at the same quantity. The profit is calculated as .

Profit Calculation:

Difference from Perfect Competition: In monopolistic competition, and at the profit-maximizing output.

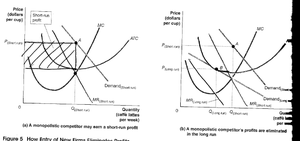

Entry and Exit in Monopolistic Competition

When firms earn economic profits, new firms enter the market, shifting the demand curve for incumbents to the left and making it more elastic. Entry continues until firms earn zero economic profit (break even). Conversely, firms may exit if they incur losses.

Effects of Entry:

Incumbents' demand curves shift left and become flatter (more elastic).

Market power decreases.

Entry continues until for the marginal firm.

Long-Run Outcome: Firms earn zero economic profit unless they continuously differentiate their products or reduce costs.

Maintaining Economic Profits

To sustain economic profits in the long run, firms must continuously differentiate their products or find ways to lower production costs. Perceived differentiation, even if minor, can be achieved through effective marketing. Technological innovation can also provide temporary profit advantages until competitors catch up.

Strategies for Profit:

Continuous product differentiation

Cost reduction through innovation

Effective marketing to create perceived value

Adaptation: Firms must adapt to changing environments to remain competitive.

Comparison: Perfect Competition vs. Monopolistic Competition

Price vs. Marginal Cost: Monopolistically competitive firms charge a price higher than marginal cost.

Production Efficiency: Monopolistically competitive firms do not produce at minimum ATC and have excess capacity.

Consumer Benefits: Consumers enjoy a wider variety of products, but pay higher prices.

Trade-Off: Consumers face higher prices and less efficiency, but benefit from products better suited to their preferences.

Key Formulas and Concepts

Profit Maximization:

Profit Calculation:

Market Power:

Conclusion

Monopolistic competition offers a more realistic model of market behavior than perfect competition, highlighting the importance of product differentiation, pricing power, and adaptation. While it sacrifices some economic efficiency, it provides consumers with greater choice and firms with opportunities for innovation and profit.