Back

BackChapter 13

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monopolistic Competition: The Competitive Model in a More Realistic Setting

Introduction to Monopolistic Competition

Monopolistic competition is a market structure that closely resembles perfect competition but incorporates product differentiation. It is prevalent in many modern economies, where firms compete by offering similar but not identical products. Understanding this model helps explain real-world markets more accurately than the perfectly competitive model alone.

Characteristics of Monopolistic Competition

Many buyers and sellers: Numerous firms and consumers participate in the market.

Differentiated products/services: Firms sell products that are similar but not identical, allowing for consumer choice based on preferences.

Low barriers to entry: New firms can enter the market relatively easily, ensuring competition remains robust.

These characteristics are similar to perfect competition, except for product differentiation. In perfect competition, products are identical, while in monopolistic competition, differentiation gives firms some control over pricing.

Product Differentiation and Market Power

Because products are differentiated, firms in monopolistic competition are price makers rather than price takers. Each firm faces a downward-sloping demand curve, meaning they can raise prices without losing all customers, but the presence of close substitutes makes demand relatively elastic.

Market Power: The ability to set prices above marginal cost (P > MC).

Allocative Inefficiency: Unlike perfect competition, monopolistically competitive firms do not achieve P = MC, resulting in deadweight loss (DWL).

Consumer Trade-off: Consumers pay higher prices for differentiated products that better match their preferences.

Demand and Marginal Revenue in Monopolistic Competition

In monopolistic competition, the firm's demand curve is not the same as its marginal revenue (MR) curve. The MR curve lies below the demand curve and has twice the slope. This is because lowering the price to sell more units reduces the revenue gained from previous units sold at a higher price.

Key Equations:

Profit Maximization Rule:

Profit Calculation:

Elasticity of Demand and Total Revenue

The elasticity of demand determines how total revenue (TR) changes as price changes. When demand is elastic, a decrease in price increases TR; when demand is inelastic, a decrease in price decreases TR.

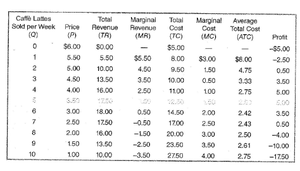

Caffè Lattes Sold per Week (Q) | Price (P) | Total Revenue (TR) | Marginal Revenue (MR) | Total Cost (TC) | Marginal Cost (MC) | Average Total Cost (ATC) | Profit |

|---|---|---|---|---|---|---|---|

0 | $6.00 | $0.00 | - | $5.00 | - | - | -$5.00 |

1 | $5.50 | $5.50 | $5.50 | $8.00 | $3.00 | $8.00 | -$2.50 |

2 | $5.00 | $10.00 | $4.50 | $9.50 | $1.50 | $4.75 | $0.50 |

3 | $4.50 | $13.50 | $3.50 | $10.50 | $1.00 | $3.50 | $3.00 |

4 | $4.00 | $16.00 | $2.50 | $11.00 | $0.50 | $2.75 | $5.00 |

5 | $3.50 | $17.50 | $1.50 | $11.00 | $0.00 | $2.20 | $6.50 |

6 | $3.00 | $18.00 | $0.50 | $10.50 | -$0.50 | $1.75 | $7.50 |

7 | $2.50 | $17.50 | -$0.50 | $9.50 | -$1.00 | $1.36 | $8.00 |

8 | $2.00 | $16.00 | -$1.50 | $8.00 | -$1.50 | $1.00 | $8.00 |

9 | $1.50 | $13.50 | -$2.50 | $6.00 | -$2.00 | $0.67 | $7.50 |

10 | $1.00 | $10.00 | -$3.50 | $2.75 | -$3.25 | $0.28 | -$1.75 |

Example: When price falls from $6 to $3, total revenue increases, indicating elastic demand. When price falls below $3, total revenue decreases, indicating inelastic demand.

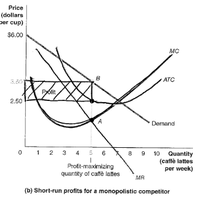

Profit Maximization in Monopolistic Competition

Firms maximize profit by producing the quantity where marginal revenue equals marginal cost (). The corresponding price is found on the demand curve above this quantity, and average total cost (ATC) is found on the ATC curve at the same quantity. Profit is calculated as .

Key Points:

In monopolistic competition, at the profit-maximizing output.

Firms may earn positive economic profits in the short run.

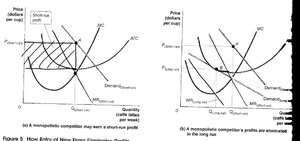

Entry and Exit in the Long Run

When firms in monopolistic competition earn economic profits, new firms are attracted to the market due to low barriers to entry. This entry shifts each incumbent firm's demand curve to the left and makes it more elastic (flatter), reducing market power and profits. Entry continues until firms earn zero economic profit (P = ATC).

Short Run: Firms can earn positive or negative economic profits.

Long Run: Entry and exit drive profits to zero for the marginal firm, but firms can maintain profits through continuous product differentiation or cost reduction.

Comparing Monopolistic Competition and Perfect Competition

Monopolistically competitive firms charge a price higher than marginal cost ().

They do not produce at the minimum average total cost (ATC), resulting in excess capacity.

Consumers benefit from a greater variety of products, but at a higher price and with some loss of efficiency (deadweight loss).

Strategies for Long-Run Profitability

To maintain economic profits in the long run, firms must continuously differentiate their products or reduce costs. Differentiation can be real (unique features) or perceived (branding, marketing). Firms that fail to adapt will lose their competitive edge and profits.

Product Differentiation: Offering new features, styles, or quality improvements.

Cost Reduction: Implementing new technologies or more efficient production methods.

Marketing: Creating a perception of uniqueness or higher value.

Example: Technology firms like Intel maintain profits by innovating and differentiating their products faster than competitors can imitate.

Conclusion

Monopolistic competition provides a more realistic model of many real-world markets than perfect competition. It explains why firms have some pricing power, why product variety exists, and why economic profits are competed away in the long run unless firms continuously innovate and adapt.