Back

BackMonopoly and Antitrust Policy: Microeconomics Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monopoly and Antitrust Policy

Introduction

This chapter explores the concept of monopoly, the sources of monopoly power, how monopolies determine price and output, the economic consequences of monopoly, the practice of price discrimination, and the role of government policy in regulating monopolies. Understanding these topics is essential for analyzing markets where competition is limited and for evaluating the effectiveness of antitrust laws.

What is a Monopoly?

Definition and Real-World Examples

Monopoly: A market structure where a single firm is the sole seller of a good or service with no close substitutes.

Monopolies are rare, but some firms have significant market power due to unique products or government protection.

Firms may also collude to act like a monopoly, which is illegal in many countries.

Example: The United States Postal Service (USPS) historically held a legal monopoly on mail delivery, though competition from private firms and electronic communication has reduced its dominance.

Sources of Monopoly Power

Barriers to Entry

Monopolies arise due to barriers that prevent other firms from entering the market. The four main sources are:

Government Restrictions on Entry: Patents, copyrights, trademarks, and public franchises legally protect firms from competition.

Control of a Key Resource: Ownership or control of essential resources (e.g., ALCOA's control of bauxite for aluminum production).

Network Externalities: The value of a product increases as more people use it (e.g., social networks, operating systems).

Natural Monopoly: Economies of scale are so significant that one firm can supply the entire market at a lower cost than multiple firms (e.g., utilities).

Example: Hasbro's trademark on the Monopoly board game prevents other firms from using the same name, maintaining its monopoly in that market.

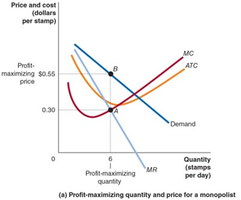

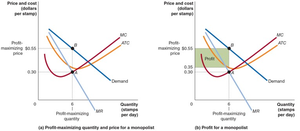

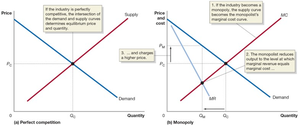

Monopoly Pricing and Output Decisions

Profit Maximization

Monopolists maximize profit by producing the quantity where marginal revenue (MR) equals marginal cost (MC). Unlike perfectly competitive firms, monopolists face a downward-sloping demand curve and can set prices above marginal cost.

Profit-maximizing rule: Produce where .

The price is determined by the demand curve at the profit-maximizing quantity.

Barriers to entry allow monopolists to earn long-run economic profits.

Formula:

Economic Efficiency and Monopoly

Welfare Effects

Monopoly leads to higher prices and lower quantities compared to perfect competition, resulting in a loss of economic efficiency known as deadweight loss.

Consumer surplus decreases due to higher prices.

Producer surplus may increase, but not enough to offset the loss to consumers.

Deadweight loss: The reduction in total surplus due to fewer trades occurring.

Price Discrimination

Charging Different Prices to Different Consumers

Price discrimination occurs when a firm charges different prices to different customers for the same product, not based on cost differences.

Possible when firms have market power, can identify groups with different willingness to pay, and prevent resale (arbitrage).

Examples include student and senior discounts, airline ticket pricing, and dynamic pricing strategies.

Perfect price discrimination (first-degree) charges each consumer their maximum willingness to pay, eliminating consumer surplus.

Formula for profit under price discrimination:

Additional info: In practice, perfect price discrimination is rare, but firms often use group or versioning strategies to approximate it.

Government Policy Toward Monopoly

Antitrust Laws and Regulation

Governments use antitrust laws to prevent collusion, break up monopolies, and regulate mergers that may reduce competition. Natural monopolies are often regulated to set prices closer to efficient levels.

Antitrust laws: Laws designed to promote competition and prevent anti-competitive practices.

Regulation of natural monopolies: Government agencies may set prices to allow zero economic profit, balancing efficiency and firm viability.

Herfindahl-Hirschman Index (HHI): A measure of market concentration used to evaluate potential mergers.

Formula for HHI:

where is the market share of firm as a decimal.

Summary Table: Monopoly vs. Perfect Competition

Characteristic | Monopoly | Perfect Competition |

|---|---|---|

Number of Firms | One | Many |

Market Power | High | None |

Price | Above MC | Equals MC |

Output | Lower | Higher |

Economic Profit (Long Run) | Possible | Zero |

Efficiency | Not Allocatively Efficient | Allocatively Efficient |

Key Takeaways

Monopolies arise due to barriers to entry and can set prices above marginal cost, leading to inefficiency.

Price discrimination allows firms to increase profits and may, in some cases, improve efficiency.

Government policy seeks to regulate or prevent monopolies to protect consumer welfare and promote competition.