Back

BackMonopoly and Antitrust Policy: Microeconomics Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monopoly and Antitrust Policy

Introduction to Monopoly and Market Power

Monopoly and antitrust policy are central topics in microeconomics, focusing on markets where competition is limited and firms have significant control over prices. This chapter explores the characteristics of monopoly, the determination of price and output, the social costs of monopoly, price discrimination, and government policies to regulate monopolies.

Imperfect Competition and Market Power

Core Concepts

Imperfectly Competitive Industry: An industry in which individual firms have some control over the price of their output, unlike perfect competition where firms are price takers.

Market Power: The ability of a firm to raise prices without losing all customers. Market power is a defining feature of imperfect competition.

Forms of Imperfect Competition

Monopoly: An industry with a single firm, significant barriers to entry, and no close substitutes for the product.

Oligopoly: An industry with a small number of large firms, each affecting market prices.

Monopolistic Competition: Many firms, differentiated products, and free entry and exit.

Pure Monopoly: A single firm produces a unique product with no close substitutes and faces significant barriers to entry.

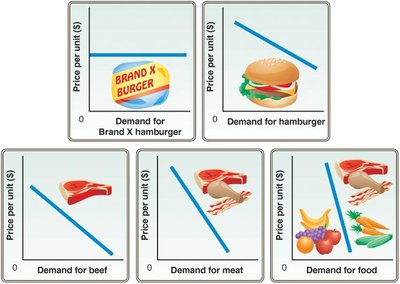

Market Boundaries and Elasticity

The definition of an industry affects the number of substitutes and the elasticity of demand. The broader the definition, the fewer substitutes and the less elastic the demand.

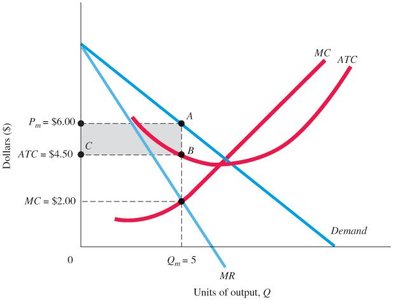

Price and Output Decisions in Pure Monopoly Markets

Demand in Monopoly Markets

A monopolist is the sole supplier and faces the market demand curve directly.

The monopolist chooses the price and quantity combination that maximizes profit, considering the trade-off between higher prices and lower quantities sold.

Marginal Revenue and Market Demand

For a linear demand curve, marginal revenue (MR) is always less than price (P) except for the first unit sold.

The formula for marginal revenue when the demand curve is linear is: For a demand curve , then

Graphical Analysis of Monopoly Pricing

The monopolist maximizes profit where marginal revenue equals marginal cost (MR = MC). At this output, the monopolist sets the highest price consumers are willing to pay for that quantity.

Absence of a Supply Curve in Monopoly

Unlike competitive firms, a monopolist does not have a supply curve independent of demand. The quantity supplied depends on both the marginal cost and the demand curve.

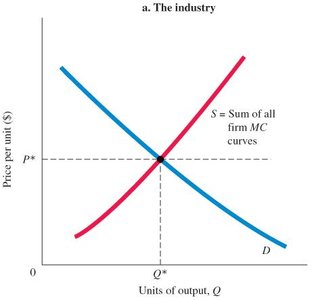

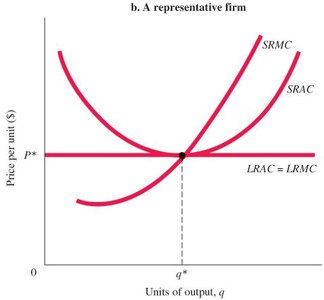

Comparison: Perfect Competition vs. Monopoly

Perfect Competition in the Long Run

In perfect competition, price equals long-run average cost (LRAC), and firms earn zero economic profit in the long run.

Monopoly vs. Perfect Competition Outcomes

Monopolies produce less output and charge higher prices compared to perfectly competitive markets.

Monopoly: and

Monopoly in the Long Run: Barriers to Entry

Types of Barriers

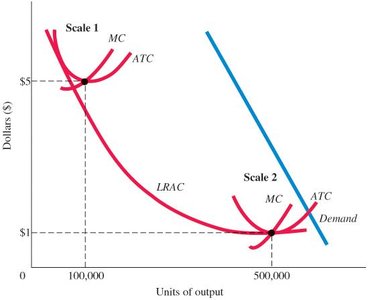

Economies of Scale: Large-scale production lowers average costs, leading to natural monopolies where one firm can supply the entire market more efficiently than multiple firms.

Patents: Legal protection granting exclusive rights to produce a product or use a process.

Government Rules: Regulations or licenses that restrict entry.

Ownership of Scarce Inputs: Control over essential resources can create monopoly power.

Network Effects: The value of a product increases as more people use it (network externalities).

The Social Costs of Monopoly

Inefficiency and Deadweight Loss

Monopoly leads to allocative inefficiency, as output is restricted and price is raised above marginal cost.

Deadweight Loss: The net loss of total (consumer and producer) surplus due to monopoly pricing.

The area representing deadweight loss is the triangle between the monopoly and competitive output levels, bounded by the demand and marginal cost curves.

Rent-Seeking Behavior

Firms may expend resources to maintain monopoly power (e.g., lobbying), which is socially wasteful.

Government Failure: When government intervention, influenced by rent-seeking, reduces economic efficiency.

Price Discrimination

Definition and Types

Price Discrimination: Charging different prices to different buyers for the same product, not based on cost differences.

Perfect Price Discrimination: Each consumer is charged their maximum willingness to pay, capturing all consumer surplus as profit.

Conditions for Price Discrimination

Ability to segment markets based on elasticity of demand.

Prevention of resale (no-arbitrage condition).

Examples: Movie theaters, hotels, and museums often charge different prices based on age or residency.

Remedies for Monopoly: Antitrust Policy

Major Antitrust Legislation

Sherman Act (1890): Prohibits contracts, combinations, or conspiracies in restraint of trade and attempts to monopolize.

Rule of Reason: Legal standard to determine whether business practices are anti-competitive.

Clayton Act (1914): Strengthens antitrust laws by prohibiting specific practices like tying contracts and certain mergers.

Federal Trade Commission (FTC): Investigates and enforces antitrust laws against unfair business practices.

Key Terms and Concepts

Barriers to Entry

Deadweight Loss

Market Power

Natural Monopoly

Network Externalities

Patent

Perfect Price Discrimination

Price Discrimination

Pure Monopoly

Rent-Seeking Behavior

Rule of Reason

Summary

Monopoly markets differ fundamentally from perfectly competitive markets in terms of price, output, and efficiency. Barriers to entry allow monopolists to earn long-run profits, but at the cost of reduced consumer surplus and increased deadweight loss. Price discrimination can increase profits further, but requires specific market conditions. Antitrust policies aim to regulate or break up monopolies to promote competition and protect consumer welfare.