Back

BackMonopoly and Antitrust Policy: Microeconomics Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 15: Monopoly and Antitrust Policy

15.1 Is Any Firm Ever Really a Monopoly?

A monopoly is a market structure where a single firm is the sole seller of a good or service with no close substitutes. The definition can be narrow (ignoring all other firms) or broad (being the only seller of a particular product in a region).

Narrow definition: The firm can ignore the actions of all other firms because there are no close substitutes.

Broader definition: The firm is the only seller of a product in a market, even if distant substitutes exist.

Example: An electric company is a monopoly because candles are not a close substitute for electric lighting.

Economic profit in monopoly markets is not competed away as long as barriers to entry exist.

15.2 Where Do Monopolies Come From?

Monopolies arise due to high barriers to entry, which prevent other firms from entering the market. There are four main sources of barriers to entry:

Government action (patents, copyrights, trademarks, public franchises)

Control of a key resource

Network externalities

Economies of scale (natural monopoly)

Government Action Blocks Entry

Patents: Exclusive legal right to produce a product for 20 years.

Copyrights: Exclusive right to produce and sell a creation for up to 70 years after the creator’s death.

Trademarks: Legal protection for brand names and symbols.

Public franchise: Government designates a firm as the only legal provider of a good or service.

Control of a Key Resource

Rare, but possible if a firm owns or controls a vital input (e.g., Alcoa and bauxite, International Nickel Company and nickel).

Network Externalities

The value of a product increases as more people use it (e.g., smartphones, social networks).

Natural Monopoly

A natural monopoly occurs when economies of scale are so significant that one firm can supply the entire market at a lower average total cost than multiple firms.

Common in industries with high fixed costs and low marginal costs (e.g., utilities).

15.3 How Does a Monopoly Choose Price and Output?

A monopoly maximizes profit by producing the quantity where marginal revenue (MR) equals marginal cost (MC). Unlike competitive firms, a monopolist faces the market demand curve directly.

Monopolies are price makers, facing downward-sloping demand and MR curves.

Cutting price increases quantity sold but reduces revenue on previous units.

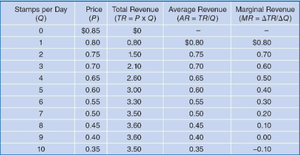

Marginal Revenue Table Example

The following table shows hypothetical data for the market for first-class mail, illustrating how price, total revenue, average revenue, and marginal revenue change as quantity increases:

Stamps per Day (Q) | Price (P) | Total Revenue (TR = P × Q) | Average Revenue (AR = TR/Q) | Marginal Revenue (MR = ΔTR/ΔQ) |

|---|---|---|---|---|

0 | $0.85 | $0 | - | - |

1 | 0.80 | 0.80 | 0.80 | 0.80 |

2 | 0.75 | 1.50 | 0.75 | 0.70 |

3 | 0.70 | 2.10 | 0.70 | 0.60 |

4 | 0.65 | 2.60 | 0.65 | 0.50 |

5 | 0.60 | 3.00 | 0.60 | 0.40 |

6 | 0.55 | 3.30 | 0.55 | 0.30 |

7 | 0.50 | 3.50 | 0.50 | 0.20 |

8 | 0.45 | 3.60 | 0.45 | 0.10 |

9 | 0.40 | 3.60 | 0.40 | 0.00 |

10 | 0.35 | 3.50 | 0.35 | -0.10 |

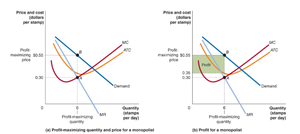

Profit Maximization for a Monopolist

Profit is maximized where MR = MC.

The profit-maximizing price is found on the demand curve at this quantity.

Total profit is the area between price and average total cost, multiplied by quantity.

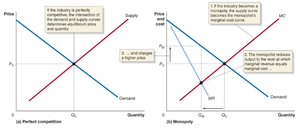

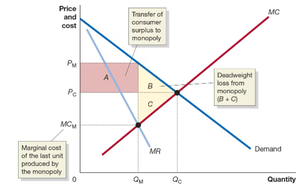

15.4 Does Monopoly Reduce Economic Efficiency?

Monopoly leads to a reduction in economic efficiency compared to perfect competition. This is measured by changes in consumer surplus, producer surplus, and the creation of deadweight loss.

Consumer surplus decreases due to higher prices.

Producer surplus increases as monopolists capture more profit.

Deadweight loss represents the loss of total surplus due to reduced output.

Monopoly causes a decrease in consumer surplus, an increase in producer surplus, and a deadweight loss.

Market power (the ability to set price above marginal cost) leads to inefficiency in most markets, not just monopolies.

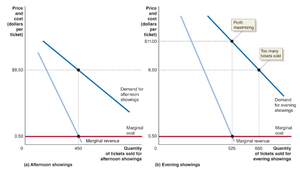

15.5 Price Discrimination: Charging Different Prices for the Same Product

Price discrimination occurs when a firm charges different prices to different customers for the same good or service, not based on cost differences.

Requirements for price discrimination:

Market power

Ability to segment the market by willingness to pay

Prevention of resale (arbitrage)

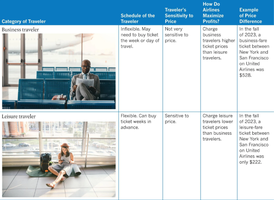

Examples: Movie theaters charge more for evening shows than afternoon shows; airlines charge business travelers more than leisure travelers.

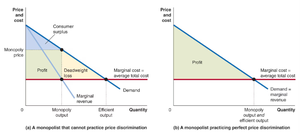

Perfect Price Discrimination

If a firm could perfectly segment the market and charge each consumer their maximum willingness to pay, it would capture all consumer surplus as profit, eliminating deadweight loss but leaving consumers worse off.

Profit increases, consumer surplus decreases.

Perfect price discrimination is rare in practice.

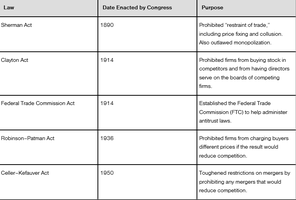

15.6 Government Policy toward Monopoly

Governments regulate monopolies to protect consumers and promote competition, primarily through antitrust laws and merger regulation.

Collusion: Firms agree not to compete, often leading to higher prices.

Antitrust laws: Laws designed to prevent monopolies and collusion.

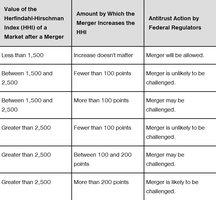

Mergers: The Trade-off Between Market Power and Efficiency

Horizontal mergers: Between firms in the same industry; more likely to increase market power.

Vertical mergers: Between firms at different stages of production; less likely to increase market power.

Regulators consider market definition, concentration, and merger standards.

Key Equations:

Total Revenue:

Average Revenue:

Marginal Revenue:

Profit Maximization:

Summary: Monopoly markets are characterized by a single seller, high barriers to entry, and the ability to set prices. While monopolies can lead to higher profits and sometimes innovation, they generally reduce consumer surplus and economic efficiency. Government policies, including antitrust laws and merger regulations, aim to limit the negative effects of monopoly power.