Back

BackMonopoly: Market Structure, Behavior, and Regulation

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monopoly: The Other Extreme

Introduction to Monopoly

A monopoly is a market structure where a single firm is the sole seller of a good or service with no close substitutes. Monopoly represents the benchmark for minimum competition, in contrast to perfect competition, which is the benchmark for maximum competition. Understanding monopoly is crucial for analyzing firm behavior, collusion, and government policy responses.

Monopoly: One firm, unique product, entry blocked.

Monopolies can arise naturally or through collusion (illegal in the U.S.).

Governments often intervene to regulate or break up monopolies.

The Four Market Structures

Market structures are classified based on the number of firms, product type, ease of entry, and examples:

Characteristic | Perfect Competition | Monopolistic Competition | Oligopoly | Monopoly |

|---|---|---|---|---|

Number of firms | Many | Many | Few | One |

Type of product | Identical | Differentiated | Identical or differentiated | Unique |

Ease of entry | High | High | Low | Entry blocked |

Examples | Wheat, poultry | Clothing stores, restaurants | Computers, automobiles | Mail delivery, tap water |

Sources of Monopoly Power

Barriers to Entry

For a monopoly to exist, barriers to entry must prevent other firms from entering the market. The four main sources are:

Government restrictions (patents, copyrights, trademarks, public franchises)

Control of a key resource

Network externalities

Natural monopoly

1. Government Restrictions on Entry

Patents: Exclusive rights to produce a product for 20 years, encouraging innovation.

Copyrights: Exclusive rights to creative works (books, films).

Trademarks: Protection for brand names and symbols.

Public franchises: Government designates a single legal provider (e.g., electricity, water, U.S. Postal Service).

2. Control of a Key Resource

Monopolies can arise when a firm controls a vital input. For example, Alcoa controlled most of the world's bauxite, and the NFL contracts most top football players, limiting competition.

De Beers is a classic example, having controlled a large share of the diamond market for decades, though its dominance has declined due to new competitors.

3. Network Externalities

Network externalities occur when a product's value increases as more people use it. Examples include auction sites (eBay), operating systems (Windows), and social networks (Facebook). These effects can lock consumers into a product, even if better alternatives exist.

4. Natural Monopoly

A natural monopoly arises when economies of scale are so significant that one firm can supply the entire market at a lower average total cost than multiple firms. This is common in industries with high fixed costs, such as electricity distribution.

Monopoly Pricing and Output Decisions

Calculating Monopoly Revenue

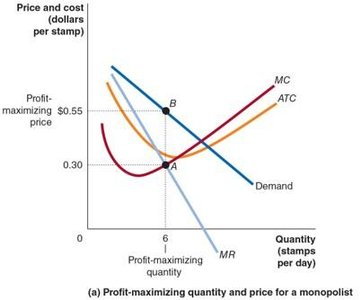

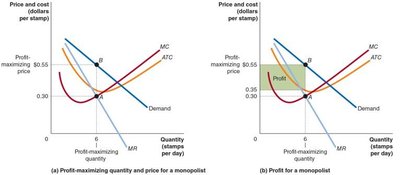

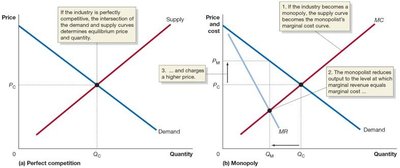

A monopolist maximizes profit by producing the quantity where marginal revenue (MR) equals marginal cost (MC). The monopolist faces a downward-sloping demand curve, so to sell more, it must lower the price, affecting both new and existing customers.

Total Revenue (TR):

Average Revenue (AR):

Marginal Revenue (MR):

Profit Maximization for a Monopolist

The profit-maximizing output is where . The price is then determined by the demand curve at this quantity, and profit is the difference between price and average total cost (ATC), multiplied by quantity.

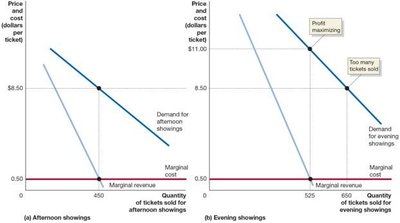

Price Discrimination

Definition and Examples

Price discrimination is when a firm charges different prices to different customers for the same product, not based on cost differences. Examples include student and senior discounts at movie theaters, and airline pricing for business vs. leisure travelers.

Conditions for Price Discrimination

Firm must have market power (not a price-taker).

Identifiable groups with different willingness to pay.

Arbitrage (resale) must be impossible or impractical.

Price Discrimination in Practice

Movie theaters and airlines use price discrimination by segmenting customers based on observable characteristics or behavior (e.g., time of day, advance booking).

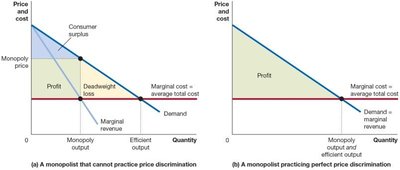

Perfect Price Discrimination

Perfect (first-degree) price discrimination occurs when a firm charges each consumer their exact willingness to pay. This extracts all consumer surplus, making it zero, and can increase economic efficiency by eliminating deadweight loss. However, it is rarely achievable in practice.

Results of Price Discrimination

Increases firm profits.

Decreases consumer surplus.

Ambiguous effect on overall economic efficiency (deadweight loss may decrease or remain).

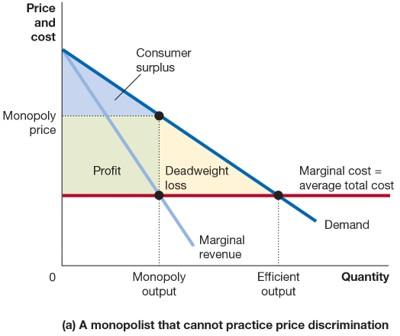

Monopoly and Economic Efficiency

Comparing Monopoly and Perfect Competition

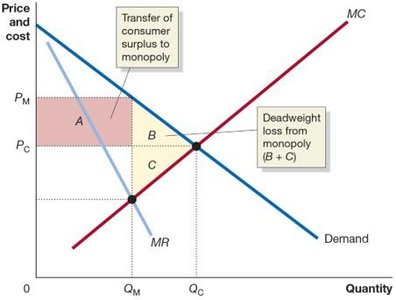

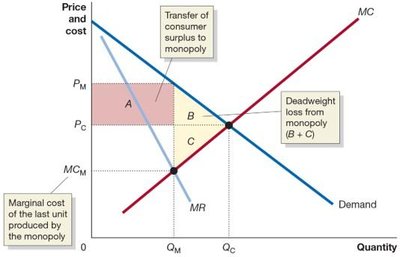

Monopoly typically results in higher prices, lower quantities, and reduced consumer surplus compared to perfect competition. Producer surplus may increase, but deadweight loss arises due to inefficiently low output.

Measuring Efficiency Losses

Although pure monopolies are rare, many firms have some market power. The overall efficiency loss in the U.S. due to market power is estimated to be less than 1% of total production, as most markets remain competitive.

Government Policy Toward Monopoly

Antitrust Laws and Regulation

Governments use antitrust laws to prevent collusion, break up monopolies, and regulate mergers. Key U.S. laws include the Sherman Act, Clayton Act, Federal Trade Commission Act, Robinson–Patman Act, and Cellar–Kefauver Act.

Law | Date | Purpose |

|---|---|---|

Sherman Act | 1890 | Prohibited restraint of trade, price fixing, and monopolization |

Clayton Act | 1914 | Prohibited stock purchases in competitors, interlocking directorates |

Federal Trade Commission Act | 1914 | Established the FTC to enforce antitrust laws |

Robinson–Patman Act | 1936 | Prohibited price discrimination that reduces competition |

Cellar–Kefauver Act | 1950 | Restricted mergers that reduce competition |

Mergers and Market Concentration

Antitrust authorities evaluate mergers using the Herfindahl-Hirschman Index (HHI), which sums the squares of market shares. Higher HHI indicates greater concentration and potential for market power.

HHI After Merger | HHI Increase | Regulatory Action |

|---|---|---|

< 1,500 | Any | Allowed |

1,500–2,500 | < 100 | Unlikely to be challenged |

1,500–2,500 | > 100 | May be challenged |

> 2,500 | < 100 | Unlikely to be challenged |

> 2,500 | 100–200 | May be challenged |

> 2,500 | > 200 | Likely to be challenged |

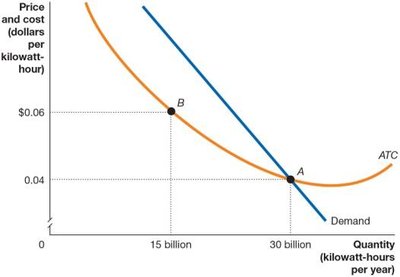

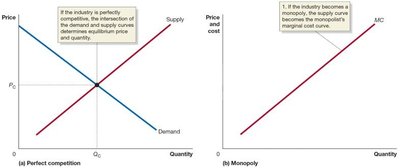

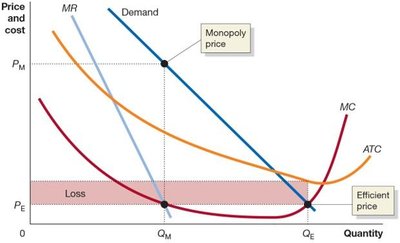

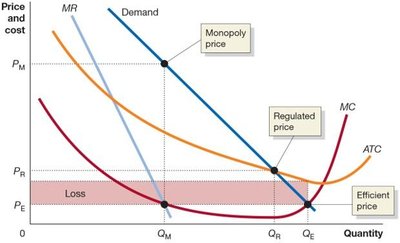

Regulating Natural Monopolies

Price Regulation

Natural monopolies are often regulated by government commissions, which set prices to balance efficiency and firm viability. The efficient price (where MC = demand) may cause losses, so regulators often allow a price that yields zero economic profit, minimizing deadweight loss.

Modern Antitrust Issues

Breaking Up Large Firms

The Department of Justice may break up large firms if they are deemed to harm competition, as with AT&T in 1984. However, network externalities and innovation incentives complicate decisions regarding firms like Google, Facebook, Amazon, and Apple.

Additional info: This guide covers the core concepts of monopoly, including sources, pricing, efficiency, price discrimination, and government policy, as outlined in a typical college microeconomics curriculum.