Back

BackMonopoly: Production, Pricing, and Welfare in Microeconomics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Monopoly: An Overview

Introduction to Monopoly

A monopoly is a market structure characterized by a single seller and many buyers, where the monopolist is the sole provider of a good or service with no close substitutes. Unlike perfect competition, where firms are price takers, a monopolist is a price maker and can influence the market price by adjusting output levels. This lecture explores how monopolists determine production and pricing, the origins and implications of monopoly power, and government responses to monopoly-induced inefficiencies.

Monopoly Versus Perfect Competition

Key Differences

Monopolies and perfectly competitive markets differ fundamentally in their structure and outcomes:

Number of Firms: Monopoly has one firm; perfect competition has many.

Market Power: Monopolists are price makers; competitive firms are price takers.

Barriers to Entry: Monopolies exist due to barriers that prevent entry; perfect competition has free entry and exit.

Pricing: In perfect competition, price equals marginal cost (P = MC). In monopoly, price exceeds marginal cost (P > MC).

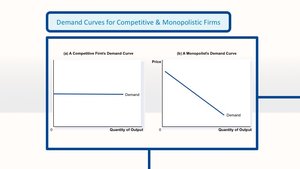

Demand Curves

The demand curve facing a competitive firm is perfectly elastic (horizontal), while a monopolist faces the entire downward-sloping market demand curve. This means the monopolist must lower the price to sell additional units, unlike the competitive firm.

Monopoly Revenue and Profit Maximization

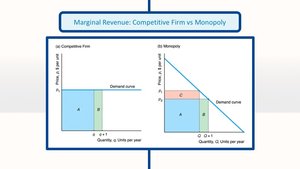

Marginal Revenue in Monopoly vs. Competition

For a competitive firm, marginal revenue (MR) equals price (P). For a monopolist, MR is always less than price because increasing output requires lowering the price on all units sold. The MR curve lies below the demand curve.

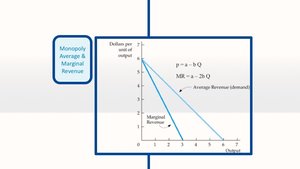

Monopoly Average and Marginal Revenue

Given a linear demand curve, such as , the marginal revenue curve is also linear and has twice the slope: . This relationship is crucial for determining the profit-maximizing output.

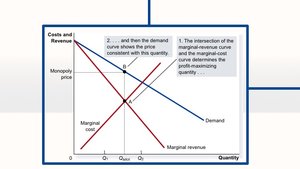

Profit Maximization Condition

The monopolist maximizes profit by producing the quantity where marginal revenue equals marginal cost (MR = MC). The corresponding price is found on the demand curve at this quantity. Unlike perfect competition, where P = MR = MC, in monopoly P > MR = MC.

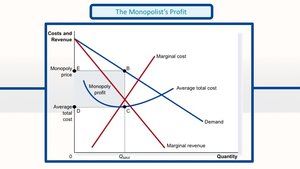

Monopoly Profit Calculation

Monopoly profit is calculated as total revenue minus total cost. The monopolist earns economic profit as long as price exceeds average total cost (ATC):

Example of Profit Maximization

Graphical and algebraic approaches can be used to find the profit-maximizing output. The optimal quantity is where MR = MC, and profit per unit is the difference between average revenue and average cost.

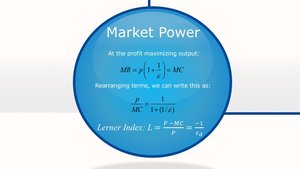

Elasticity of Demand and Monopoly Pricing

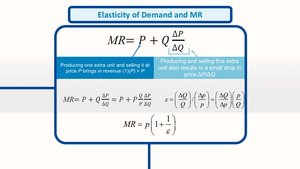

Marginal Revenue and Elasticity

Marginal revenue can be expressed in terms of the price elasticity of demand ():

Where is the price elasticity of demand (negative for downward-sloping demand). MR is closer to price when demand is more elastic.

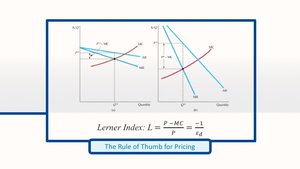

Lerner Index and Price Markup

The Lerner Index measures monopoly power as the markup of price over marginal cost, relative to price:

A higher Lerner Index indicates greater market power. The markup is smaller when demand is more elastic.

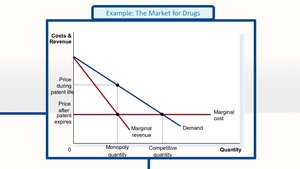

Example: The Market for Drugs

Pharmaceutical markets illustrate monopoly power: patented drugs are sold at high prices, but prices fall sharply when patents expire and generics enter the market.

Why Monopolies Arise

Barriers to Entry

The fundamental cause of monopoly is barriers to entry, which prevent other firms from entering the market. These barriers can arise from:

Ownership of a key resource

Government-granted exclusive rights (e.g., patents, copyrights)

Cost advantages (natural monopoly)

Government-Created Monopolies

Governments may create monopolies by granting exclusive rights to firms through patents and copyright laws, often to encourage innovation or serve the public interest.

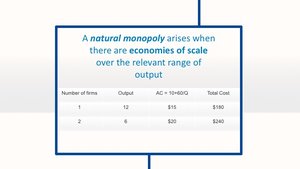

Natural Monopolies

A natural monopoly arises when a single firm can supply the entire market at a lower cost than multiple firms, typically due to economies of scale. For example, utilities often have high fixed costs and low marginal costs, making single-firm production most efficient.

Number of Firms | Output | AC = 10 + 60/Q | Total Cost |

|---|---|---|---|

1 | 12 | $15$ | $180$ |

2 | 6 | $20$ | $240$ |

Welfare Implications of Monopoly

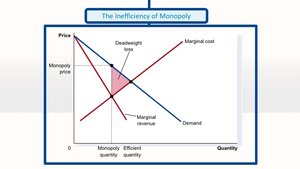

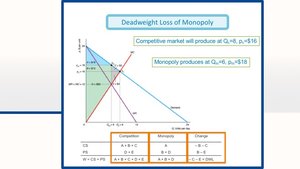

Inefficiency and Deadweight Loss

Monopolies restrict output and raise prices above marginal cost, resulting in a deadweight loss (DWL) to society. This loss represents the value of trades that do not occur due to the monopolist's pricing above marginal cost.

Why Do Monopolies Exist?

Origins of Monopoly Power

Monopolies persist due to cost advantages (e.g., superior technology, control of essential facilities), government intervention (e.g., licensing, exclusive rights), mergers, or collusion among firms (cartels).

Government Response to Monopoly

Policy Options

Governments can address monopoly power in several ways:

Increase competition (antitrust laws, breaking up firms, preventing collusion)

Regulate monopoly behavior (price regulation, output requirements)

Convert private monopolies into public enterprises

Do nothing (if intervention is not justified)

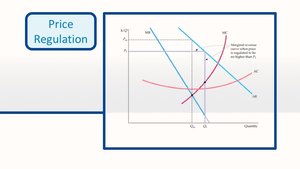

Price Regulation

Price regulation can reduce or eliminate the deadweight loss from monopoly by capping the price at or near marginal cost. However, if the regulated price is set too low, the monopolist may incur losses and exit the market.

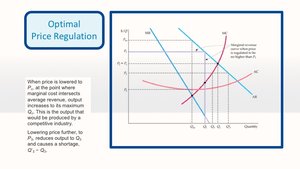

Optimal Price Regulation

Optimal regulation sets price where the average revenue (demand) curve intersects the marginal cost curve, restoring the competitive output level and eliminating deadweight loss. Setting price below this level causes shortages and potential firm exit.

Summary Table: Monopoly vs. Competition

Feature | Perfect Competition | Monopoly |

|---|---|---|

Number of Firms | Many | One |

Market Power | None (price taker) | High (price maker) |

Entry Barriers | None | High |

Price-Output Rule | P = MC | P > MC |

Efficiency | Allocatively efficient | Deadweight loss |

Key Formulas

Marginal Revenue (in terms of elasticity):

Lerner Index:

Profit: