Back

BackPerfect Competition: Theory, Application, and Efficiency

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Perfect Competition

Introduction to Perfect Competition

Perfect competition is a foundational concept in microeconomics, describing a market structure where many firms sell identical products, and no single firm can influence the market price. This chapter explores the characteristics, profit maximization, and efficiency of perfectly competitive markets.

Market Structures

Types of Market Structures

Market structures describe how firms interact with buyers and each other. The four main types, in order of decreasing competitiveness, are:

Perfect Competition: Many firms, identical products, easy entry.

Monopolistic Competition: Many firms, differentiated products, easy entry.

Oligopoly: Few firms, products may be identical or differentiated, barriers to entry.

Monopoly: One firm, unique product, entry blocked.

Each structure provides insight into real-world market behavior and firm strategies.

Characteristics of Perfectly Competitive Markets

Defining Features

Many buyers and sellers

Identical (homogeneous) products

No barriers to entry or exit

Firms in perfect competition are price takers, meaning they accept the market price as given and cannot influence it.

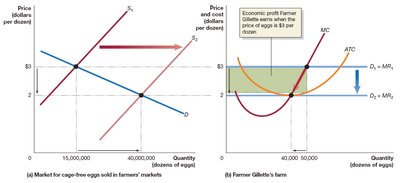

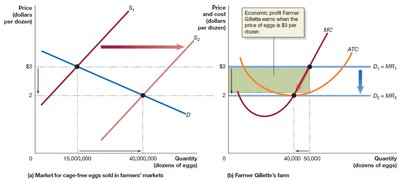

Example: Cage-Free Eggs

The market for cage-free eggs illustrates perfect competition. Initially, high demand allowed farmers to earn high profits, but as more farmers entered the market, supply increased and prices fell, eliminating long-term economic profit.

Demand Curve for a Perfectly Competitive Firm

Horizontal Demand Curve

A perfectly competitive firm faces a horizontal (perfectly elastic) demand curve at the market price. No matter how much the firm sells, the price remains constant because the firm's output is negligible relative to the market.

Profit Maximization in Perfect Competition

Total Revenue, Average Revenue, and Marginal Revenue

Total Revenue (TR):

Average Revenue (AR):

Marginal Revenue (MR):

For a perfectly competitive firm, .

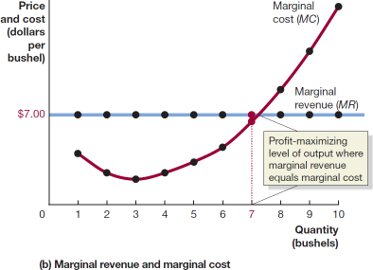

Profit Maximization Rule

Produce the quantity where (marginal revenue equals marginal cost).

For perfect competition, this is also where .

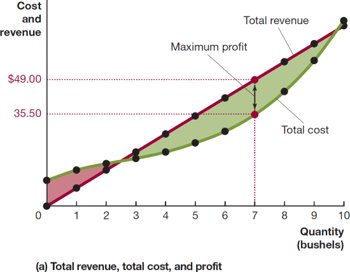

Graphical Illustration of Profit Maximization

The profit-maximizing output is where the vertical distance between total revenue and total cost is greatest.

Alternatively, it is where the marginal revenue curve intersects the marginal cost curve.

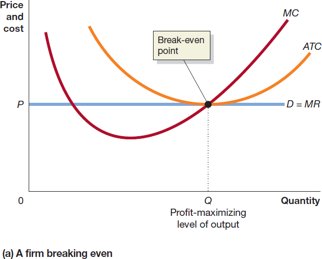

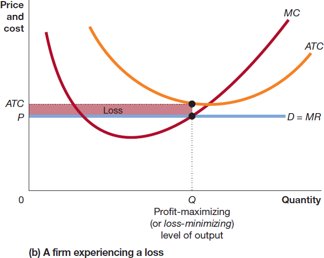

Profit, Break-Even, and Loss

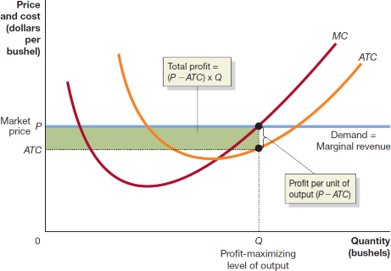

At the profit-maximizing output:

If , the firm earns a profit.

If , the firm breaks even.

If , the firm incurs a loss.

Profit per unit is , and total profit is .

Common Error in Profit Maximization

Maximizing profit per unit (where meets ) does not maximize total profit. The correct rule is to produce where .

Break-Even and Loss-Minimization

Even if a firm cannot make a profit, it should still produce at the output where to minimize losses.

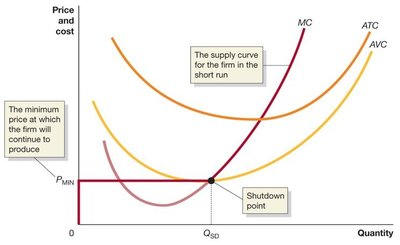

Short-Run Supply Decision

Shut Down Rule

If the market price falls below the minimum average variable cost (), the firm should shut down in the short run. Otherwise, it should produce where .

Shutdown Point: The price and output level where .

The firm's short-run supply curve is the portion of its curve above .

Long-Run Entry and Exit

Economic Profit and Entry

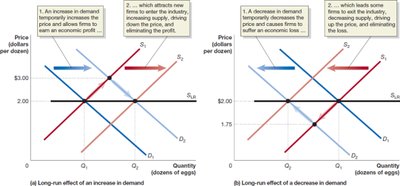

Economic profit attracts new firms, increasing market supply and lowering price until only normal profit (break-even) remains.

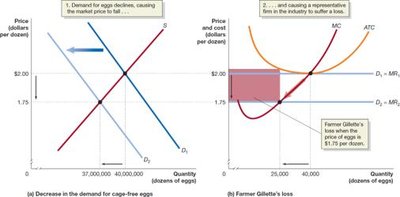

Economic Loss and Exit

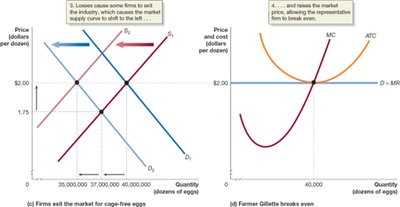

Economic losses cause firms to exit, reducing supply and raising price until the remaining firms break even.

Long-Run Competitive Equilibrium

In the long run, entry and exit of firms ensure that all firms break even (zero economic profit). The market price equals the minimum point on the long-run average cost curve.

Long-Run Supply Curve

Shape of the Long-Run Supply Curve

Constant-Cost Industry: Long-run supply curve is horizontal at the break-even price.

Increasing-Cost Industry: Long-run supply curve slopes upward (costs rise as industry expands).

Decreasing-Cost Industry: Long-run supply curve slopes downward (costs fall as industry expands).

Efficiency in Perfect Competition

Productive and Allocative Efficiency

Productive Efficiency: Goods are produced at the lowest possible cost (at minimum ATC).

Allocative Efficiency: Goods are produced up to the point where the last unit provides a marginal benefit to consumers equal to the marginal cost of production ().

Perfect competition achieves both productive and allocative efficiency in the long run, serving as a benchmark for evaluating other market structures.