Back

BackPerfect Competition: Theory, Application, and Efficiency

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Perfect Competition

Introduction to Market Structures

Market structures describe how firms interact with buyers to sell their output. The four main types, in order of decreasing competitiveness, are: perfectly competitive markets, monopolistic competition, oligopoly, and monopoly. Each structure provides insight into firm behavior and market outcomes.

Perfect Competition: Many firms, identical products, high ease of entry.

Monopolistic Competition: Many firms, differentiated products, high ease of entry.

Oligopoly: Few firms, identical or differentiated products, low ease of entry.

Monopoly: One firm, unique product, entry blocked.

Market Structure | Number of Firms | Type of Product | Ease of Entry | Examples |

|---|---|---|---|---|

Perfect Competition | Many | Identical | High | Wheat, Poultry farming |

Monopolistic Competition | Many | Differentiated | High | Clothing stores, Restaurants |

Oligopoly | Few | Identical or Differentiated | Low | Computers, Automobiles |

Monopoly | One | Unique | Entry blocked | Tap water, First-class mail |

Characteristics of Perfect Competition

A perfectly competitive market is defined by:

Many buyers and sellers

Identical products

No barriers to entry

Firms in perfect competition are price takers: they cannot influence the market price and must accept it as given.

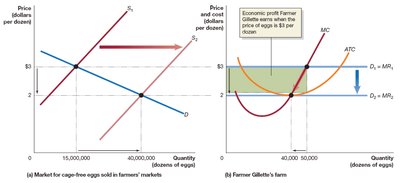

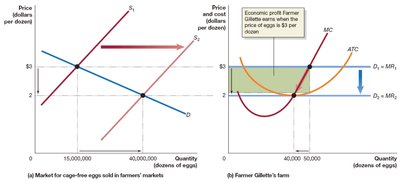

Real-World Example: Cage-Free Eggs

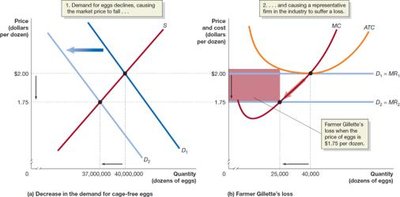

The market for cage-free eggs illustrates perfect competition. Initially, high demand allowed farmers to earn large profits, but as more farmers entered the market, supply increased and prices fell, eroding profits.

Profit Maximization in Perfect Competition

Revenue Concepts

For a perfectly competitive firm:

Total Revenue (TR):

Average Revenue (AR):

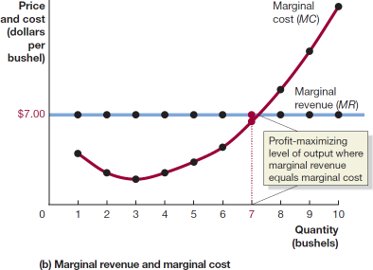

Marginal Revenue (MR):

In perfect competition, for all units sold.

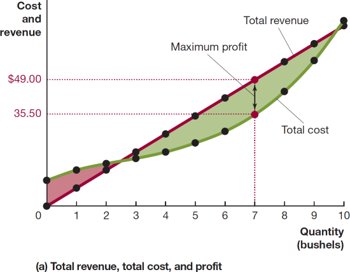

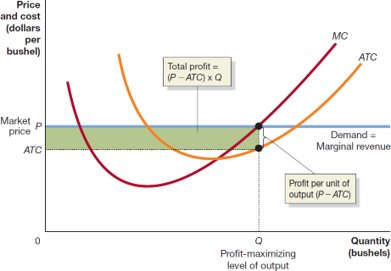

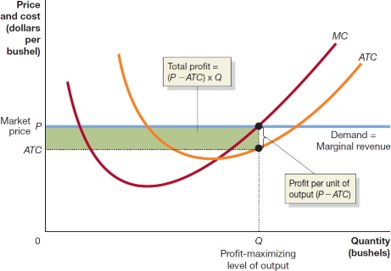

Profit Maximization Rule

Firms maximize profit by producing the quantity where marginal revenue equals marginal cost (). For perfect competition, this is also where .

Produce as long as

Stop increasing output when

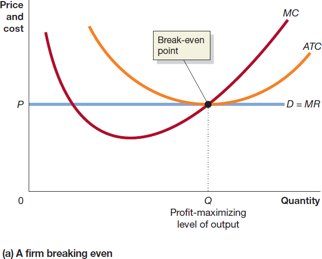

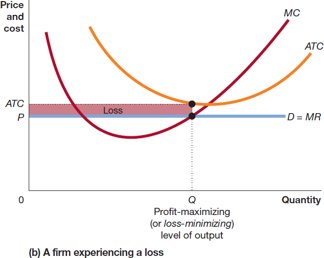

Profit, Break-Even, and Loss

At the profit-maximizing output:

If , the firm earns a profit.

If , the firm breaks even.

If , the firm incurs a loss.

Profit can be calculated as:

Common Error in Profit Maximization

It is incorrect to maximize profit per unit (where meets ); total profit is maximized where .

Break-Even and Loss-Minimization

Even if a firm cannot make a profit, it should still produce at the output where to minimize losses.

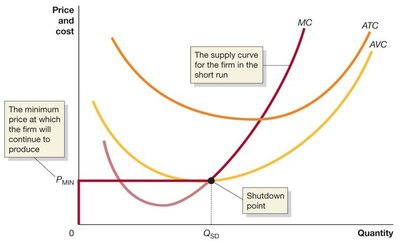

Short-Run Decisions: Produce or Shut Down?

Shutdown Rule

If the market price falls below average variable cost (), the firm should shut down in the short run. Otherwise, it should produce where .

Shutdown Point: The minimum price at which the firm covers its variable costs.

Firm and Market Supply

The individual firm's supply curve is its marginal cost curve above the minimum AVC. The market supply curve is the horizontal sum of all individual firms' supply curves.

Long-Run Adjustments: Entry and Exit

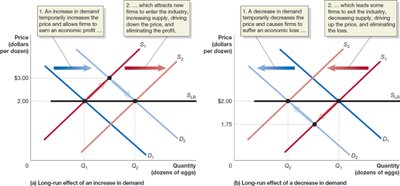

Economic Profit and Entry

Economic profit attracts new firms, increasing market supply and lowering price until only normal profit (break-even) remains. Economic profit includes both explicit and implicit costs (opportunity costs).

Explicit Costs | Implicit Costs |

|---|---|

Water, Wages, Fertilizer, Electricity, Loan payments | Forgone salary, Opportunity cost of invested capital |

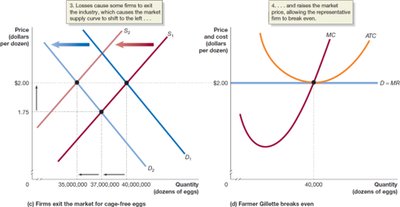

Economic Loss and Exit

Economic losses cause firms to exit, reducing supply and raising price until the remaining firms break even.

Long-Run Competitive Equilibrium

In the long run, entry and exit of firms ensure that all firms break even (zero economic profit). The market price equals the minimum point on the long-run average cost curve.

Long-run supply curve: Horizontal at the break-even price in constant-cost industries.

Increasing-Cost and Decreasing-Cost Industries

Increasing-cost industry: Entry raises input prices, causing the long-run supply curve to slope upward.

Decreasing-cost industry: Entry lowers input prices or increases economies of scale, causing the long-run supply curve to slope downward.

Efficiency in Perfect Competition

Productive and Allocative Efficiency

Productive efficiency: Goods are produced at the lowest possible cost (at minimum ATC).

Allocative efficiency: Goods are produced up to the point where the last unit provides a marginal benefit to consumers equal to the marginal cost of production ().

Perfect competition achieves both productive and allocative efficiency in the long run, serving as a benchmark for evaluating other market structures.