Back

BackPrice Controls and Market Efficiency: Microeconomics Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Price Controls and Market Efficiency

Introduction

This chapter examines the effects of government intervention in markets through price controls and output quotas. It explores how these policies impact equilibrium prices and quantities, market efficiency, and the distribution of economic surplus among market participants.

Government-Controlled Prices

Disequilibrium Prices

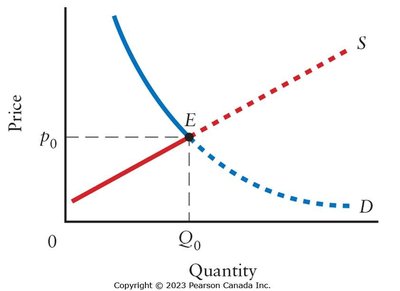

In a free market, the equilibrium price is where quantity demanded equals quantity supplied. Government intervention can set prices at disequilibrium levels, resulting in either excess supply or excess demand.

Disequilibrium Price: A price at which quantity demanded does not equal quantity supplied.

Quantity Traded: Determined by the lesser of quantity demanded and quantity supplied at the controlled price.

Voluntary Transactions: Require both a willing buyer and seller; thus, the actual quantity exchanged is limited by the smaller of demand or supply.

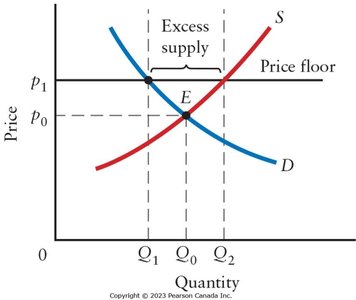

Price Floors

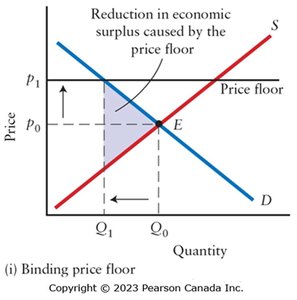

A price floor is the minimum legal price for a good or service. If set above equilibrium, it is binding and leads to excess supply.

Binding Price Floor: Raises the market price, increases quantity supplied, decreases quantity demanded, and results in unsold surplus.

Market Effects: Consumers pay higher prices and buy less; some suppliers benefit from higher prices, but others cannot sell their goods.

Income Effects: If demand is inelastic, total supplier income may rise despite lower sales volume.

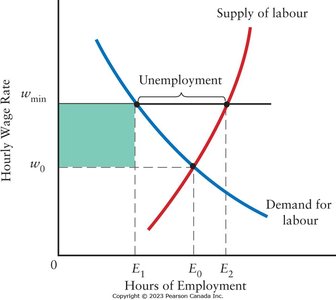

Example: Minimum Wage as a Price Floor

Minimum Wage: Sets a legal minimum for hourly wages in the labor market.

Effects: Reduces employment, increases labor supply, and creates unemployment (excess supply of labor).

Distribution: Some workers benefit from higher wages, while others lose jobs; firms pay higher labor costs.

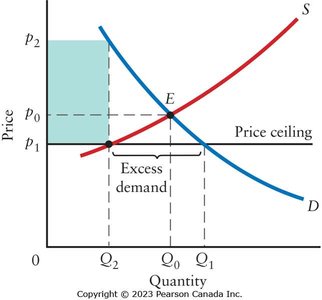

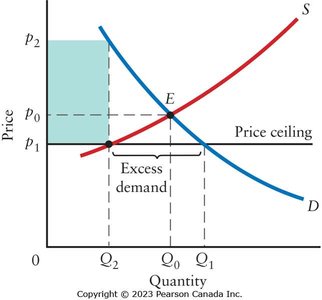

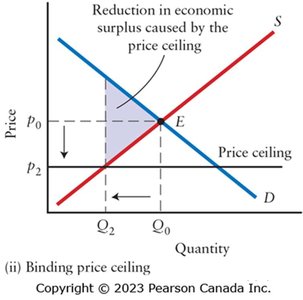

Price Ceilings

A price ceiling is the maximum legal price for a good or service. If set below equilibrium, it is binding and leads to excess demand.

Binding Price Ceiling: Lowers the market price, increases quantity demanded, decreases quantity supplied, and results in shortages.

Allocation: Not all buyers can purchase the good; allocation may be first-come, first-served or through hidden (black) markets.

Hidden Markets: Goods may be resold illegally at higher prices, undermining the policy's intent.

Goals and Limitations of Price Ceilings

Restrict production, keep prices low, and promote equity during shortages.

Hidden markets can defeat these goals by incentivizing illegal sales at higher prices.

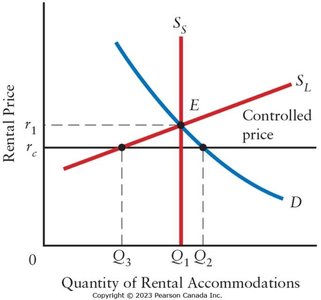

Rent Controls: A Case Study of Price Ceilings

Short-Run and Long-Run Effects

Rent controls are a specific form of price ceiling, typically intended to protect tenants. Their effects differ in the short run and long run due to supply elasticity.

Short Run: Supply of rental housing is inelastic; shortages are limited.

Long Run: Supply becomes more elastic; investment in rental housing falls, shortages worsen, and quality may decline.

Alternative Allocation: May lead to discrimination or illegal payments ("key money").

Winners and Losers

Gainers: Existing tenants in rent-controlled units.

Losers: Landlords (lower returns), future tenants (fewer available units, lower quality).

Policy Alternatives

Government can subsidize housing production or provide public housing to address shortages.

Direct income assistance to low-income households is another alternative.

All policies involve resource costs.

An Introduction to Market Efficiency

Economic Surplus and Market Efficiency

Economists use the concept of economic surplus to evaluate the overall effects of market policies. Economic surplus is the sum of consumer and producer surplus, representing the total benefit to society from market transactions.

Consumer Surplus: Value consumers receive minus what they pay.

Producer Surplus: Payments received by producers minus their production costs.

Market Efficiency: Achieved when economic surplus is maximized, typically at the free-market equilibrium.

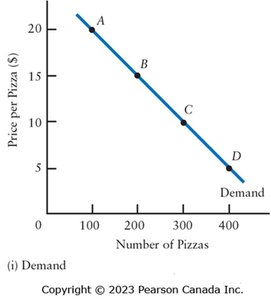

Demand as Value

The demand curve shows the maximum price consumers are willing to pay for each unit, representing the value to consumers.

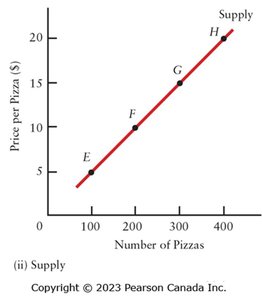

Supply as Cost

The supply curve shows the minimum price producers are willing to accept, reflecting the additional cost of producing each unit.

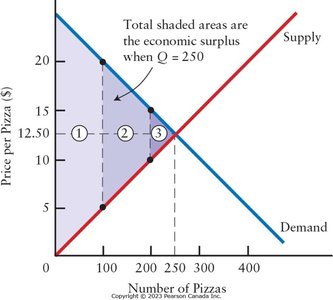

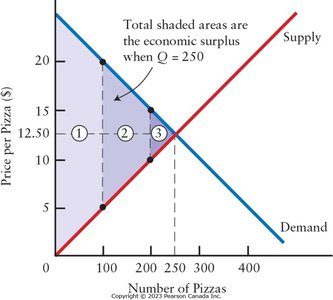

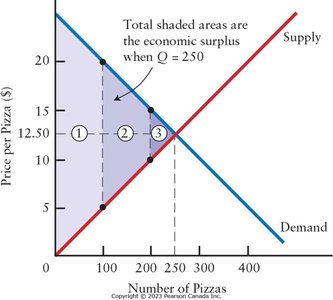

Economic Surplus in the Market

For any quantity, economic surplus is the area between the demand and supply curves.

At equilibrium, this area is maximized.

Market Inefficiency with Price Controls and Quotas

Deadweight Loss from Price Controls

Binding price floors and ceilings reduce economic surplus, creating deadweight loss—a loss of total surplus that benefits no one.

Price Floor: Reduces quantity traded, redistributes surplus from consumers to producers, but total surplus falls.

Price Ceiling: Reduces quantity traded, redistributes surplus from producers to consumers, but total surplus falls.

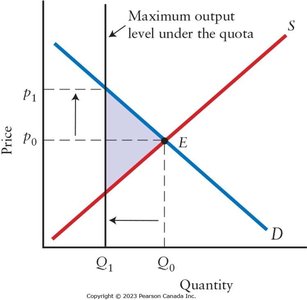

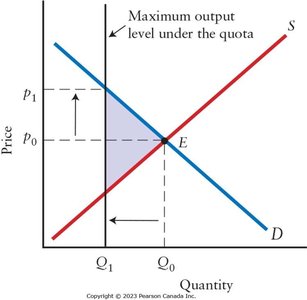

Output Quotas

An output quota limits the maximum quantity that can be produced or sold in a market. If set below equilibrium, it is binding and leads to inefficiency.

Binding Quota: Reduces quantity traded, raises price, and creates deadweight loss.

Distribution: Consumers lose (higher prices), quota holders may gain, but the cost of acquiring quotas can offset benefits.

Policy Considerations and Normative Judgments

Why Governments Intervene

Policies often aim to help specific groups (e.g., low-income workers, farmers) despite overall inefficiency.

Normative judgments (what should be) drive policy decisions, while economists focus on positive analysis (what is).

Other social values, such as public virtue or social responsibility, may outweigh efficiency in some cases (e.g., price gouging during disasters).

Key Formulas and Concepts

Economic Surplus:

Consumer Surplus:

Producer Surplus:

Deadweight Loss: