Back

BackProducers in the Long Run: Cost Minimization, Substitution, and Technological Change

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Producers in the Long Run

Introduction to the Long Run and Very Long Run

In microeconomics, the long run is a period in which all factors of production are variable, allowing firms to adjust all inputs to find the most efficient production method. The very long run extends this concept to include changes in technology, which can shift cost curves and alter production possibilities.

Short run: At least one factor is fixed; firms adjust only variable inputs.

Long run: All inputs are variable; firms choose the optimal combination of inputs and plant size.

Very long run: Technology and knowledge can change, affecting production methods and costs.

8.1 The Long Run: No Fixed Factors

Technical Efficiency and Profit Maximization

Firms in the long run must choose the most technically efficient way to produce a given output, meaning no more inputs are used than necessary. However, technical efficiency alone does not guarantee profit maximization; firms must also consider input costs to achieve cost minimization.

Technical efficiency: Producing the maximum output from a given set of inputs.

Cost minimization: Choosing the technically efficient method that produces output at the lowest possible cost, given input prices.

Profit maximization: Implies cost minimization for any given output level.

Cost Minimization Condition

To minimize costs, firms must equate the marginal product per dollar spent across all inputs. If the marginal product per dollar is higher for one input than another, the firm can reduce costs by substituting toward the more productive input.

Marginal product (MP): The additional output produced by using one more unit of an input.

Cost minimization rule: For two inputs, labor (L) and capital (K), with prices pL and pK:

If this condition is not met, the firm can lower costs by reallocating spending between inputs.

As substitution occurs, diminishing marginal returns ensure the marginal products adjust, restoring equality.

Example: If and , the firm should use more labor and less capital until the ratios are equalized.

Principle of Substitution

The principle of substitution states that firms will substitute away from inputs that become relatively more expensive and toward those that become cheaper. This principle is central to resource allocation and explains differences in production methods across countries with different factor prices.

Firms respond to changes in relative input prices by adjusting their input mix.

Resource allocation in the economy reflects these adjustments, promoting efficiency.

International differences in input prices lead to different production techniques (e.g., more machinery in high-wage countries, more labor in low-wage countries).

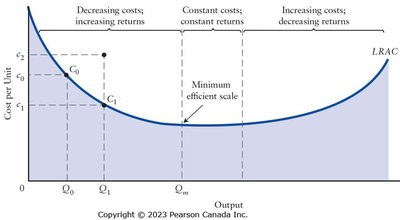

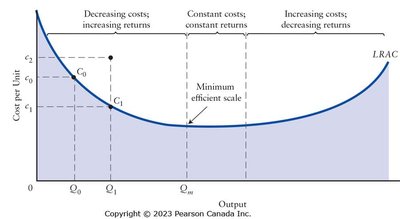

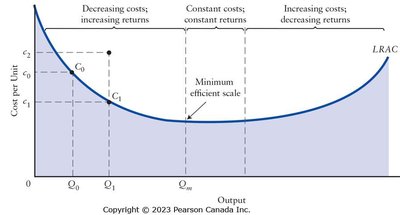

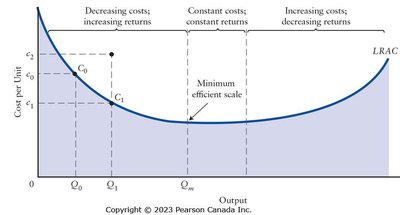

Long-Run Cost Curves

Long-Run Average Cost (LRAC) Curve

The long-run average cost (LRAC) curve shows the lowest possible average cost of producing each output level when all inputs are variable. It is the boundary between attainable and unattainable cost levels, given current technology and input prices.

LRAC is typically "saucer-shaped" due to economies and diseconomies of scale.

There is only one LRAC for any given set of input prices; all costs are variable in the long run.

Economies and Diseconomies of Scale

Economies of scale: LRAC falls as output increases (increasing returns to scale). Often due to specialization and division of labor.

Minimum efficient scale: The smallest output at which LRAC reaches its minimum; all economies of scale are realized.

Constant returns to scale: LRAC is flat; output increases in direct proportion to inputs.

Diseconomies of scale: LRAC rises as output increases (decreasing returns to scale), often due to management difficulties in large firms.

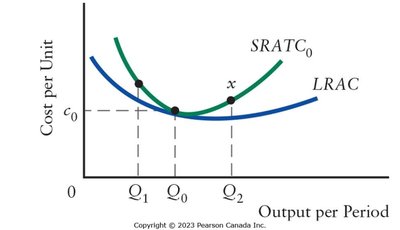

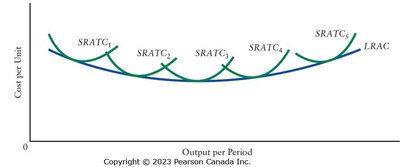

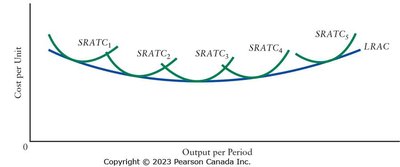

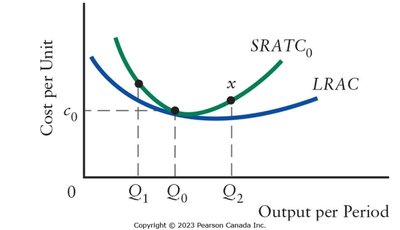

The Relationship Between LRAC and SRATC Curves

Short-Run and Long-Run Cost Curves

The LRAC curve represents the lowest cost of producing any output when all factors are variable. Each short-run average total cost (SRATC) curve shows the lowest cost when at least one factor is fixed. There are many SRATC curves, each corresponding to a different level of the fixed factor.

No SRATC curve can fall below the LRAC curve; LRAC is the envelope curve tangent to all SRATC curves.

For each output level, the optimal SRATC is tangent to the LRAC at that point.

Historical Note: Jacob Viner first described the relationship between LRAC and SRATC curves, but initially made the error of connecting the minimum points of SRATC curves rather than constructing the lower envelope (tangency) curve.

8.2 The Very Long Run: Changes in Technology

Technological Change and Productivity

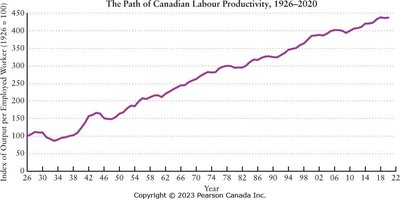

In the very long run, technological change alters the available production techniques and resources, shifting the LRAC curve. Technological change includes new processes, improved inputs, and new products, and is measured by increases in productivity (output per unit of input).

Productivity: Output per worker or per hour of work; a key measure of technological progress.

Technological change is often driven by firms seeking profit through innovation.

Productivity growth is the main driver of rising living standards.

Firms' Choices in the Very Long Run

Firms respond to market signals by substituting away from expensive inputs or innovating to reduce costs. While substitution is a reliable cost-reduction strategy, innovation is riskier but can yield large profits if successful.

Firms may both substitute and innovate in response to input price changes.

Innovation involves uncertainty and requires significant potential rewards to justify the risks.

Significance of Productivity Growth

Historically, economists like Thomas Malthus predicted declining living standards due to diminishing returns and population growth. However, technological progress has allowed output to grow faster than population, leading to sustained increases in productivity and living standards.

Productivity growth disproved the "dismal science" predictions by enabling higher output per person.

Technological change is endogenous—driven by economic incentives and firm behavior.