Back

BackProducers in the Short Run: Production, Costs, and Profit in Microeconomics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 7: Producers in the Short Run

7.1 What Are Firms?

Firms are the fundamental units of production in an economy, organized in various legal and operational forms. Understanding the structure and objectives of firms is essential for analyzing their behavior and decision-making processes.

Types of Firms:

Single Proprietorship: Owned and operated by one individual.

Ordinary Partnership: Owned by two or more individuals sharing responsibilities and profits.

Limited Partnership: Includes both general and limited partners, with varying degrees of liability.

*Corporation: A legal entity separate from its owners, can be private or public.

State-Owned Enterprise (Crown Corporation): Owned by the government.

Non-Profit Organization: Operates for purposes other than profit generation.

Multinational Enterprises (MNEs): Firms operating in more than one country, common among large corporations.

Financing of Firms

Firms require financial capital to operate, which is distinct from physical capital (assets like machinery and buildings). The two main sources of financial capital are equity and debt.

Equity: Funds provided by owners or shareholders in exchange for ownership (shares). Profits distributed to shareholders are called dividends.

Debt: Borrowed funds from creditors, including loans and bonds. Firms must repay principal and interest, but creditors do not have ownership rights.

Goals of Firms

Economists typically assume that firms aim to maximize profit and act as single, consistent decision-making units. This assumption allows for the prediction of firm behavior in various market conditions.

Profit Maximization: The primary objective, though debates exist regarding social responsibility and the broader public interest.

Social Responsibility: Some argue profit maximization may conflict with societal goals, while others claim it drives innovation and benefits stakeholders.

7.2 Production, Costs, and Profits

Production

Firms combine various inputs to produce goods and services. The relationship between inputs and output is described by the production function.

Types of Inputs:

Intermediate products (outputs from other firms)

Natural resources

Labour services

Physical capital services

Production Function: Shows the maximum output possible from a given set of inputs. It is a technological relationship, often written as , where is output, is labour, and is capital.

Production as a Flow Concept: Measured over a period of time, not at a single moment.

Costs and Profits

Understanding costs is crucial for analyzing firm behavior. Economists distinguish between explicit and implicit costs, leading to different measures of profit.

Explicit Costs: Direct monetary payments for resources (e.g., wages, rent, materials, interest). Includes depreciation.

Implicit Costs: Opportunity costs of using resources owned by the firm (e.g., owner's time, owner's capital).

Accounting Profit:

Economic Profit:

Economic Loss: Negative economic profit.

Table: Accounting Versus Economic Profit

Type of Profit | Calculation | Includes |

|---|---|---|

Accounting Profit | Revenues - Explicit Costs | Monetary outlays only |

Economic Profit | Revenues - (Explicit + Implicit Costs) | Monetary outlays and opportunity costs |

Profit-Maximizing Output

Economic profit is the difference between total revenue and total cost (including both explicit and implicit costs):

Time Horizons for Decision Making

Firms make decisions over different time horizons, affecting which inputs can be varied.

Short Run: At least one input is fixed (often capital); others are variable.

Long Run: All inputs can be varied, but technology is fixed.

Very Long Run: All inputs and technology can be changed.

7.3 Production in the Short Run

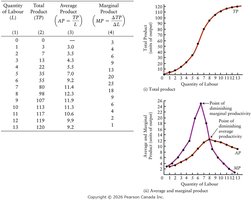

Total, Average, and Marginal Products

In the short run, firms analyze how output changes as they vary the amount of a variable input (usually labour), holding other inputs fixed.

Total Product (TP): Total output produced in a given period.

Average Product (AP): Output per unit of variable input:

Marginal Product (MP): Additional output from one more unit of variable input:

Diminishing Marginal Product (Law of Diminishing Returns)

As more units of a variable input are added to fixed inputs, the additional output from each new unit eventually decreases. This is a fundamental principle in production theory.

Each additional worker has less fixed capital to work with, reducing their marginal contribution.

Examples: Additional sets in a workout, extra pollution filters, or more stocks in a portfolio each yield diminishing returns.

The Average-Marginal Relationship

The relationship between marginal and average product is important for understanding production efficiency.

When , average product is rising.

When , average product is falling.

The marginal product curve intersects the average product curve at the maximum point of the average product.

7.4 Costs in the Short Run

Defining Short-Run Costs

Short-run costs are divided into fixed and variable components, which together determine total cost.

Total Cost (TC):

Total Fixed Cost (TFC): Costs that do not vary with output (e.g., rent, salaries).

Total Variable Cost (TVC): Costs that change with output (e.g., materials, hourly wages).

Average Total Cost (ATC):

Average Fixed Cost (AFC):

Average Variable Cost (AVC):

Marginal Cost (MC):

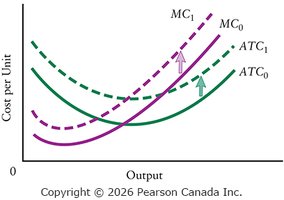

Short-Run Cost Curves

Cost curves illustrate how costs change as output varies. Key relationships include the intersection of MC with ATC and AVC at their minimum points, and the U-shape of the ATC curve.

Why U-Shaped MC and AVC Curves?

The U-shape of marginal and average variable cost curves is due to the law of diminishing returns. As more of the variable input is used, its marginal and average product eventually decline, causing costs to rise.

AVC is minimized when AP is maximized.

MC is minimized when MP is maximized.

Capacity

The output level at which ATC is minimized is called the firm's capacity. Producing below this level means the firm has excess capacity.

Shifts in Short-Run Cost Curves

Changes in input prices shift cost curves. An increase in variable input prices raises both ATC and MC, while an increase in fixed input prices raises only ATC.

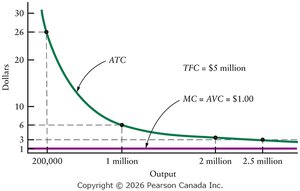

Special Case: Digital Products and Diminishing Returns

For many digital products, marginal cost is nearly zero after the initial investment, so the law of diminishing returns does not apply. In these cases, AVC equals MC, and ATC declines as output increases due to spreading fixed costs.

Additional info: The above notes expand on the provided slides by including definitions, formulas, and examples for each concept, ensuring a comprehensive and self-contained study guide for microeconomics students.