Back

BackSupply and Demand: Foundations of Market Equilibrium and Government Intervention

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Supply and Demand

Introduction

The supply-and-demand model is a fundamental framework in microeconomics, used to analyze how prices and quantities are determined in competitive markets. This chapter covers the determinants of demand and supply, the concept of market equilibrium, the effects of shocks and government interventions, and the aggregation of individual behaviors into market outcomes.

Demand

Determinants of Demand

Price of the good: The most direct influence on the quantity demanded.

Tastes: Consumer preferences can shift demand.

Information: Knowledge about the good or market conditions affects demand.

Prices of other goods: Includes complements (goods used together) and substitutes (goods used in place of each other).

Income: Higher income generally increases demand for normal goods.

Government rules and regulations: Policies can restrict or encourage consumption.

Other factors: Such as expectations about future prices.

The Demand Curve

The demand curve shows the quantity of a good that consumers are willing to buy at each possible price, holding other factors constant. The law of demand states that, all else equal, consumers demand more of a good when its price is lower.

Quantity demanded (Q): The amount consumers are willing to buy at a given price.

Demand curve: Downward sloping due to the law of demand.

Shifts in the Demand Curve

A demand curve shifts when a non-price determinant changes (e.g., income, tastes, price of substitutes). For example, an increase in the price of beef (a substitute for pork) shifts the demand curve for pork to the right.

The Demand Function

The demand function expresses quantity demanded as a function of price and other variables:

p: Price of the good

p_b: Price of beef (substitute)

p_c: Price of chicken (another substitute)

Y: Consumer income

Example (linear demand function):

Given , , , the demand function simplifies to .

Inverse Demand Function

The inverse demand function expresses price as a function of quantity:

This form is useful for calculating how much the price must change to achieve a desired change in quantity demanded.

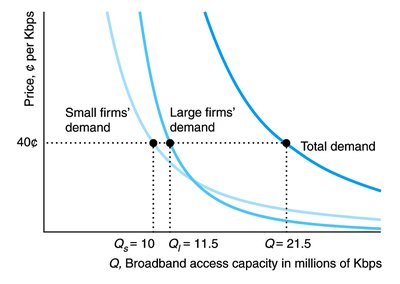

Summing Demand Curves

The market demand curve is the horizontal sum of individual demand curves:

Supply

Determinants of Supply

Price of the good: Higher prices generally increase quantity supplied.

Costs: Higher input costs reduce supply.

Government rules and regulations: Can restrict or encourage production.

The Supply Curve

The supply curve shows the quantity of a good that firms are willing to sell at each possible price, holding other factors constant. It is typically upward sloping.

Shifts in the Supply Curve

A supply curve shifts when a non-price determinant changes (e.g., input costs, technology). For example, an increase in the price of hogs (an input) shifts the supply curve for pork to the left.

The Supply Function

The supply function expresses quantity supplied as a function of price and input costs:

p: Price of the good

p_h: Price of hogs (input)

Example (linear supply function):

Given , the supply function simplifies to .

Summing Supply Curves

The market supply curve is the horizontal sum of individual supply curves (e.g., domestic and foreign suppliers):

Market Equilibrium

Definition and Properties

Equilibrium: The price and quantity at which quantity demanded equals quantity supplied.

Equilibrium price (p*): The price at which the market clears.

Equilibrium quantity (Q*): The quantity bought and sold at the equilibrium price.

Mathematical Solution for Equilibrium

Set and solve for and :

Example:

Set equal:

General Solution

For (demand) and (supply):

Shocking the Equilibrium

Shifts in Demand or Supply

Equilibrium changes only if a shock occurs that shifts the demand or supply curve (e.g., changes in income, input prices, or government policy).

Effects of Government Interventions

Types of Interventions

Policies that shift supply: Licensing laws, quotas, bans.

Policies that cause demand to differ from supply: Price ceilings (maximum prices), price floors (minimum prices).

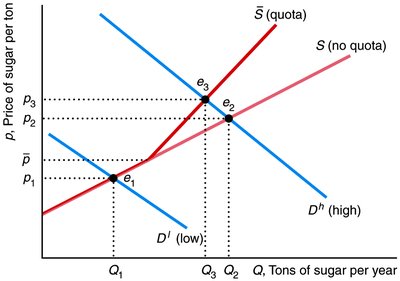

Quotas and Bans

Quotas restrict the quantity that can be imported or sold, shifting the supply curve and affecting equilibrium price and quantity.

Price Ceilings and Floors

A price ceiling is a legal maximum price. If set below equilibrium, it creates excess demand (shortage). A price floor is a legal minimum price. If set above equilibrium, it creates excess supply (surplus).

Minimum Wage Example

A binding minimum wage (price floor in the labor market) leads to excess supply of labor (unemployment).

Perfectly Competitive Markets

Characteristics

All participants are price takers.

Firms sell identical products.

Full information about price and quality is available.

Low costs of trading.

Summary Table: Effects of Government Interventions

Policy | Effect on Supply/Demand | Market Outcome |

|---|---|---|

Quota | Shifts supply left | Higher price, lower quantity |

Ban | Removes foreign supply | Higher price, lower quantity |

Price Ceiling | Limits maximum price | Excess demand (shortage) |

Price Floor | Sets minimum price | Excess supply (surplus) |

Additional info: This summary includes expanded academic context, definitions, and examples to ensure the notes are self-contained and suitable for exam preparation.