Back

BackChapter 11

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Technology, Production, and Costs

Technological Change and Production Costs

Technological advancements are a key driver in reducing production costs and increasing output. In economics, technology refers to the process a firm uses to turn inputs into outputs, not just new inventions or gadgets. Improvements in technology allow firms to produce more with the same resources or the same output with fewer resources, thereby reducing total costs. This is reflected in a rightward shift of the supply curve and an outward shift of the production possibilities frontier (PPF).

Inputs (Factors of Production): Workers, machines, natural resources, entrepreneurial skill.

Technology (Economic Definition): The entire process of transforming inputs into outputs, including skills, training, organization, and actual machinery.

Technological Change: Any change in a firm's ability to produce a given level of output with a given quantity of inputs.

Examples: Positive changes include better organization or retraining workers; negative changes include hiring less skilled workers or damage to facilities.

Just-In-Time Inventory (JIT): A technological change in inventory management that minimizes inventory levels and automates restocking, reducing opportunity costs but potentially increasing the risk of stock-outs.

Short Run vs. Long Run in Production

Firms analyze costs and production over two time frames: the short run and the long run.

Short Run (SR): At least one input is fixed (e.g., plant size, machinery). Some costs are fixed, others are variable.

Long Run (LR): All inputs are variable. Firms can adjust plant size, adopt new technology, and all costs become variable.

Key Cost Equations:

In the long run: and

Examples: In the SR, a pizzeria cannot expand its building overnight but can hire more workers. In the LR, it can build a larger store or buy more ovens.

Total, Variable, and Fixed Costs

Understanding the distinction between different types of costs is essential for economic analysis.

Total Costs (TC): The sum of all input costs used in production.

Variable Costs (VC): Costs that change with output (e.g., raw materials, hourly labor).

Fixed Costs (FC): Costs that remain constant regardless of output (e.g., rent, insurance).

All costs are either variable or fixed, and both explicit (monetary) and implicit (opportunity) costs must be considered for true economic analysis.

Explicit Costs: Actual monetary payments (wages, rent, materials).

Implicit Costs: Opportunity costs (forgone salary, interest on invested capital, economic depreciation).

Economic Cost:

Cost Classification Table

The following table summarizes the classification of costs by type:

Cost Type | Explicit/Implicit | Variable/Fixed |

|---|---|---|

Wages (hourly) | Explicit | Variable |

Raw materials | Explicit | Variable |

Lease payments | Explicit | Fixed |

Owner's forgone salary | Implicit | Fixed |

Interest on invested capital | Implicit | Fixed/Variable |

Economic depreciation | Implicit | Fixed/Variable |

Utilities | Explicit | Variable |

Advertising | Explicit | Fixed |

Additional info: Table entries inferred from context and standard microeconomics classifications.

Production Function and Marginal Product

The production function describes the relationship between inputs and the maximum output that can be produced. It reflects the firm's technology.

Production Function: Relationship between inputs employed and maximum output.

Marginal Product of Labor (MPL): The additional output from hiring one more worker.

Initially, MPL increases due to division of labor and specialization, but eventually decreases due to the Law of Diminishing Returns—adding more of a variable input to a fixed input will eventually cause the marginal product to decline.

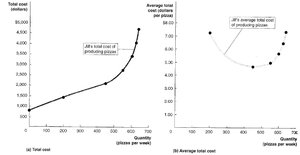

Short-Run Cost Curves

Cost curves help visualize the relationship between output and costs in the short run. The total cost curve starts at the level of fixed costs and increases as output rises. The average total cost (ATC) curve is typically U-shaped due to initial efficiency gains and later diminishing returns.

Marginal Cost (MC): The change in total cost from producing one more unit:

Relationship: When MPL is rising, MC is falling; when MPL is falling, MC is rising.

ATC, AVC, MC: MC curve intersects ATC and AVC at their minimum points.

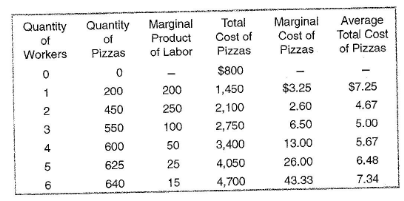

Short-Run Cost Table Example

The following table illustrates the calculation of various cost measures for a pizzeria:

Quantity of Workers | Quantity of Pizzas | Marginal Product of Labor | Total Cost of Pizzas | Marginal Cost of Pizzas | Average Total Cost of Pizzas |

|---|---|---|---|---|---|

0 | 0 | - | $800 | - | - |

1 | 200 | 200 | $1,450 | $3.25 | $7.25 |

2 | 450 | 250 | $2,100 | $2.60 | $4.67 |

3 | 550 | 100 | $2,750 | $6.50 | $5.00 |

4 | 600 | 50 | $3,400 | $13.00 | $5.67 |

5 | 625 | 25 | $4,050 | $26.00 | $6.48 |

6 | 640 | 15 | $4,700 | $43.33 | $7.34 |

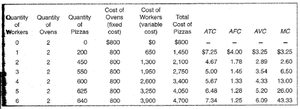

Comprehensive Short-Run Cost Table

Quantity of Workers | Quantity of Ovens | Quantity of Pizzas | Cost of Ovens (Fixed) | Cost of Workers (Variable) | Total Cost | ATC | AFC | AVC | MC |

|---|---|---|---|---|---|---|---|---|---|

0 | 2 | 0 | $800 | $0 | $800 | - | - | - | - |

1 | 2 | 200 | $800 | $650 | $1,450 | $7.25 | $4.00 | $3.25 | $3.25 |

2 | 2 | 450 | $800 | $1,300 | $2,100 | $4.67 | $1.78 | $2.89 | $2.60 |

3 | 2 | 550 | $800 | $1,950 | $2,750 | $5.00 | $1.45 | $3.55 | $6.50 |

4 | 2 | 600 | $800 | $2,600 | $3,400 | $5.67 | $1.33 | $4.33 | $13.00 |

5 | 2 | 625 | $800 | $3,250 | $4,050 | $6.48 | $1.28 | $5.20 | $26.00 |

6 | 2 | 640 | $800 | $3,900 | $4,700 | $7.34 | $1.25 | $6.09 | $43.33 |

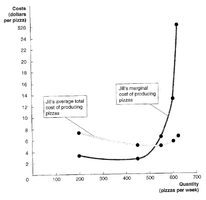

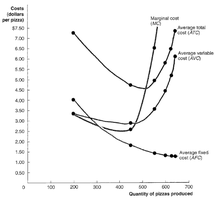

Graphical Representation of Cost Curves

The following graph shows the relationship between marginal cost, average total cost, average variable cost, and average fixed cost:

MC, ATC, and AVC are U-shaped due to initial efficiency gains and later diminishing returns.

AFC declines continuously as output increases.

MC intersects ATC and AVC at their minimum points.

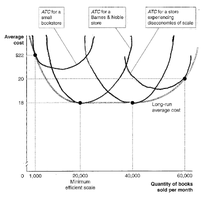

Long-Run Average Cost Curve (LRAC) and Economies of Scale

In the long run, all costs are variable, and the long-run average cost curve (LRAC) shows the lowest possible cost of producing each output level when all inputs can be varied. The LRAC is typically U-shaped due to economies and diseconomies of scale.

Economies of Scale: LRAC falls as output increases.

Minimum Efficient Scale: The lowest output at which all economies of scale are exhausted.

Constant Returns to Scale: LRAC remains constant as output increases.

Diseconomies of Scale: LRAC rises as output increases due to inefficiencies in large-scale operations.

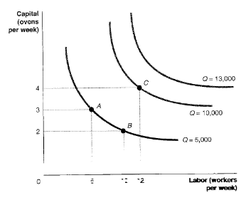

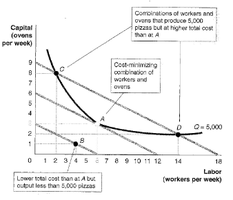

Isoquants and Isocosts: Choosing the Optimal Input Mix

Firms use isoquants and isocost lines to determine the optimal combination of inputs (labor and capital) to minimize costs for a given level of output.

Isoquant: Curve showing all combinations of two inputs that produce the same output.

Isocost Line: All combinations of two inputs that cost the same total amount.

Marginal Rate of Technical Substitution (MRTS): The rate at which one input can be substituted for another while keeping output constant.

Optimal input mix is where the isoquant is tangent to the isocost line.

Mathematically:

Additional info: The mathematical condition for optimal input use is analogous to the consumer's utility maximization rule, but with marginal products and input prices.