Back

BackThe Production Process: The Behavior of Profit-Maximizing Firms

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

The Production Process: The Behavior of Profit-Maximizing Firms

Introduction

This chapter explores how firms make decisions to maximize profits by choosing optimal production methods and input combinations. It covers the concepts of economic profit, production functions, the law of diminishing returns, and the use of isoquants and isocosts in cost minimization.

The Behavior of Profit-Maximizing Firms

Basic Decisions of Firms

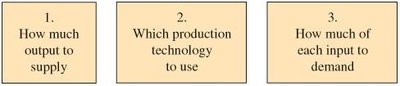

Firms must make three fundamental decisions to achieve profit maximization:

How much output to supply

Which production technology to use

How much of each input to demand

Profits and Economic Costs

Profit is defined as the difference between total revenue and total cost:

Total revenue is the total amount received from sales:

Total cost includes both fixed and variable costs.

Economic profit accounts for both explicit costs and opportunity costs.

Normal rate of return is the minimum return required to keep owners and investors satisfied, often equated to the interest rate on risk-free government bonds.

Short Run vs. Long Run Decisions

Short run: At least one factor of production is fixed; firms cannot enter or exit the industry.

Long run: All factors of production are variable; firms can enter or exit the industry.

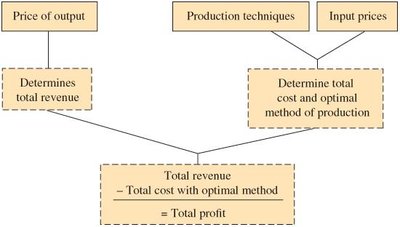

The Bases of Firm Decisions

Firms need to know:

Market price of output (potential revenues)

Available production techniques (input requirements)

Input prices (costs)

The optimal method of production is the one that minimizes cost for a given level of output.

The Production Process

Production Technology

Production technology describes the quantitative relationship between inputs and outputs.

Labor-intensive technology: Relies heavily on human labor.

Capital-intensive technology: Relies heavily on capital (machinery, equipment).

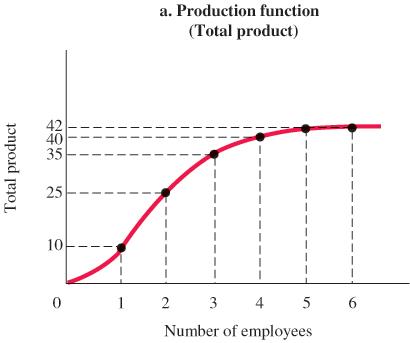

Production Functions: Total, Marginal, and Average Product

A production function (or total product function) expresses the relationship between inputs and outputs mathematically or numerically.

Total product: Total quantity of output produced for a given amount of input.

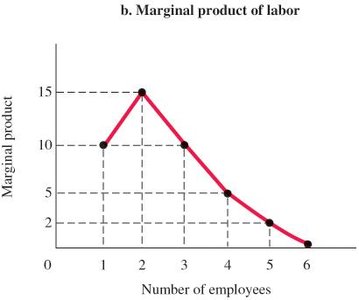

Marginal product: Additional output produced by adding one more unit of a specific input, holding other inputs constant.

Average product: Output per unit of input.

The Law of Diminishing Returns

When additional units of a variable input are added to fixed inputs, the marginal product of the variable input eventually declines.

This principle applies in the short run for all firms.

Graphical Representation of Production Functions

Production functions and marginal product curves visually illustrate the relationships between inputs and outputs.

Marginal Product vs. Average Product

If marginal product is above average product, the average rises; if marginal product is below average product, the average falls.

Production with Two Variable Factors

Inputs such as capital and labor are often complementary.

Increasing capital can raise the productivity of labor, which is central to national productivity growth.

Choice of Technology

Factors Affecting Technology Choice

Firms compare alternative technologies based on input requirements and costs.

They select the technology that minimizes production costs, given current input prices.

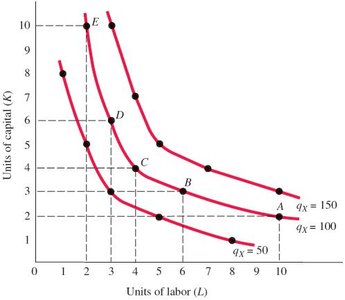

Tabular Comparison of Technologies

Firms use tables to compare input combinations and costs for different technologies. For example:

Technology | Units of Capital (K) | Units of Labor (L) |

|---|---|---|

A | 2 | 10 |

B | 3 | 6 |

C | 4 | 4 |

D | 6 | 3 |

E | 10 | 2 |

Cost-minimizing choices depend on input prices.

Isoquants and Isocosts (Appendix)

Isoquants

An isoquant shows all combinations of capital and labor that can produce a given level of output.

Isoquants are analogous to indifference curves in consumer theory.

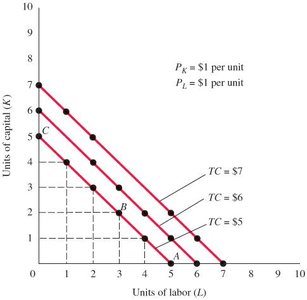

Isocost Lines

An isocost line shows all combinations of capital and labor available for a given total cost.

The equation for an isocost line is:

The slope of the isocost line is .

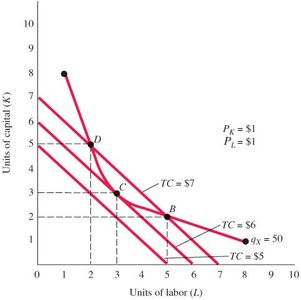

Cost Minimization: Isoquants and Isocosts

The cost-minimizing combination of inputs occurs where an isoquant is tangent to an isocost line.

At this point, the marginal rate of technical substitution (MRTS) equals the ratio of input prices:

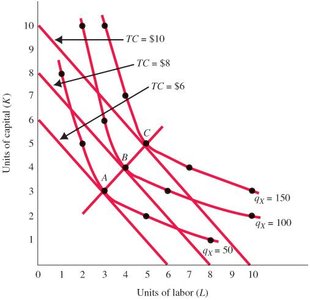

Cost Curves

Plotting cost-minimizing input combinations for different output levels yields the firm's cost curve.

Key Terms and Concepts

Average product

Capital-intensive technology

Economic profit

Firm

Labor-intensive technology

Law of diminishing returns

Long run

Marginal product

Normal rate of return

Optimal method of production

Production

Production function

Production technology

Profit

Short run

Total cost

Total revenue

Isoquant

Isocost line

Marginal rate of technical substitution

Summary

This chapter provides a foundation for understanding how firms make production decisions to maximize profit, the role of opportunity costs, and the analytical tools used to determine the least-cost combination of inputs. The concepts of isoquants and isocosts are essential for analyzing cost minimization and will be further developed in subsequent chapters on cost and supply.