Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Depreciation for Partial Years quiz

You can tap to flip the card.

What is partial depreciation and when is it necessary?

You can tap to flip the card.

👆

What is partial depreciation and when is it necessary?

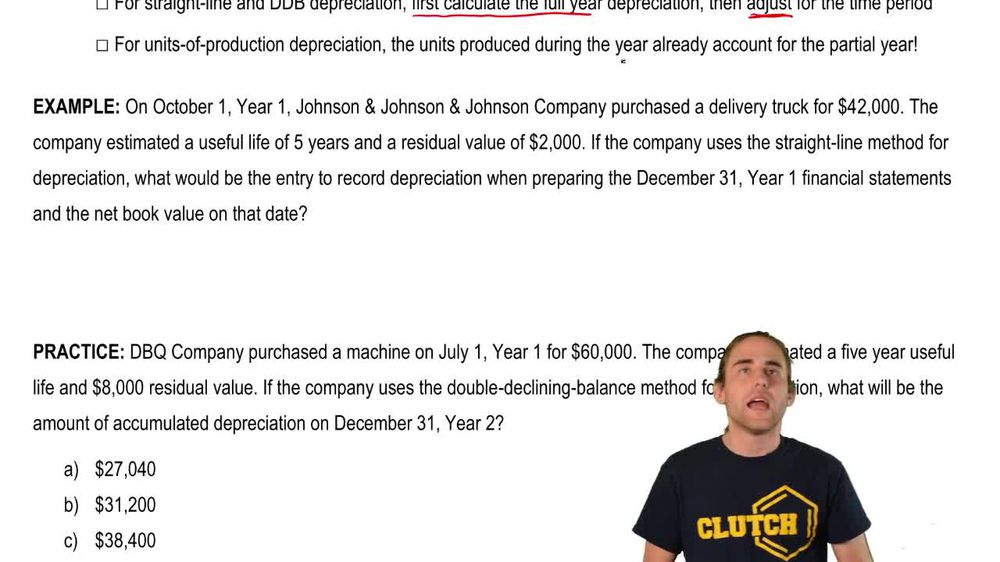

Partial depreciation is depreciation calculated for only part of a year when an asset is purchased mid-year, rather than on the first day of the year.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Depreciation for Partial Years definitions

Depreciation for Partial Years

13 Terms

Retirement of Plant Assets (No Proceeds)

8. Long Lived Assets

10 problems

Topic

8. Long Lived Assets

14 topics

15 problems

Chapter

Guided course

04:51

Depreciation for Partial Years

851

views

17

rank

Terms in this set (15)

Hide definitions

What is partial depreciation and when is it necessary?

Partial depreciation is depreciation calculated for only part of a year when an asset is purchased mid-year, rather than on the first day of the year.

How do you calculate partial depreciation using the straight-line method?

First, calculate the full-year depreciation, then prorate it based on the fraction of the year the asset was owned.

How is the double declining balance method adjusted for partial years?

Calculate the full-year depreciation using the double declining balance method, then multiply by the fraction of the year the asset was owned.

Does the units of production method require adjustment for mid-year purchases?

No, because depreciation is based on the number of units produced, not the time owned.

If an asset is purchased on October 1st, how many months of depreciation should be recorded by December 31st?

Three months of depreciation should be recorded, covering October, November, and December.

What is the formula for annual straight-line depreciation?

Annual straight-line depreciation = (Cost - Residual Value) / Useful Life.

How do you prorate annual depreciation for a partial year?

Multiply the annual depreciation by the fraction of the year the asset was owned (e.g., 3/12 for three months).

What journal entry is made to record partial year depreciation?

Debit Depreciation Expense and credit Accumulated Depreciation for the prorated amount.

In the example, what is the annual straight-line depreciation for a \$42,000 truck with a \$2,000 residual value and 5-year life?

The annual straight-line depreciation is \$8,000.

How much depreciation expense is recorded for three months if the annual depreciation is \$8,000?

The depreciation expense for three months is \$2,000 (\$8,000 × 3/12).

What is the net book value of the truck at year-end after three months of depreciation?

The net book value is \$40,000 (\$42,000 cost minus \$2,000 accumulated depreciation).

Why is it important to pay attention to the purchase date when calculating depreciation?

Because failing to adjust for partial years can lead to incorrect depreciation amounts and errors in financial statements.

What accounts are affected by the journal entry for partial year depreciation?

Depreciation Expense (debited) and Accumulated Depreciation (credited).

How does the units of production method inherently account for partial years?

It only records depreciation based on the actual number of units produced, regardless of the time owned.

What is a common mistake students make when calculating depreciation for assets purchased mid-year?

A common mistake is forgetting to prorate the depreciation and instead recording a full year's expense.

BackBack

BackBack

04:51

04:51