Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Marginal Cost definitions

You can tap to flip the card.

Marginal Cost

You can tap to flip the card.

👆

Marginal Cost

The extra expense incurred from producing one additional unit, calculated by dividing the change in total cost by the change in output.

Track progress

Control buttons has been changed to "navigation" mode.

1/13

Related flashcards

Recommended videos

Marginal Cost quiz

Marginal Cost

15 Terms

Guided course

10:48

Marginal Cost

3

views

Terms in this set (13)

Hide definitions

Marginal Cost

The extra expense incurred from producing one additional unit, calculated by dividing the change in total cost by the change in output.

Total Cost

The sum of all expenses, including both fixed and variable, required to produce a given quantity of goods.

Variable Cost

The portion of total expenses that changes directly with the level of output, such as wages for additional workers.

Fixed Cost

The portion of total expenses that remains unchanged regardless of output, like the daily cost of pizza ovens.

Marginal Product of Labor

The increase in output resulting from hiring one more worker, reflecting the productivity of additional labor.

Diminishing Marginal Productivity

The phenomenon where adding more workers eventually leads to smaller increases in output, raising extra production costs.

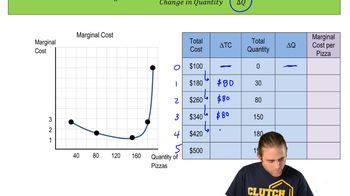

U-Shaped Curve

A graphical pattern where a cost measure first declines, reaches a minimum, and then rises as output increases.

Quantity

The total number of units produced within a given period, used to measure changes in output.

Output

The total amount of goods produced by a firm, often measured in units like pizzas in examples.

Aggregate Supply

The total quantity of goods and services that producers in an economy are willing to supply at a given overall price level.

Aggregate Demand

The total quantity of goods and services demanded across all levels of an economy at a given overall price level.

Wage

The payment made to workers for their labor, often a key component of variable expenses in production.

Cost Behavior

The way in which total expenses change as output levels vary, crucial for production and employment decisions.

BackBack

BackBack

10:48

10:48