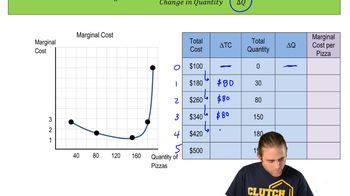

Marginal cost is the additional cost incurred from producing one more unit of output, calculated as the change in total cost divided by the change in quantity.

How do you calculate marginal cost when output increases by more than one unit?

You divide the change in total cost by the change in quantity to find the average additional cost per unit over that range.

What is the formula for marginal cost?

Marginal cost = Change in Total Cost / Change in Quantity.

Why do fixed costs not affect marginal cost calculations?

Fixed costs do not change with output, so only variable costs (like wages) impact the change in total cost when calculating marginal cost.

What happens to marginal cost as the marginal product of labor increases?

As the marginal product of labor increases, marginal cost decreases because each additional worker produces more output for the same cost.

What is the relationship between marginal cost and marginal product of labor?

Marginal cost is inversely related to the marginal product of labor; when one rises, the other falls.

What shape does the marginal cost curve typically take?

The marginal cost curve is typically U-shaped, falling at first and then rising sharply.

Why does the marginal cost curve eventually rise after initially falling?

It rises due to diminishing marginal productivity, where each additional worker adds less output, increasing the cost per unit.

How does hiring additional workers affect total cost in the example given?

Each additional worker increases total cost by the amount of their wage, which is a variable cost.

If the change in total cost is \$80 and the change in quantity is 50, what is the marginal cost?

Marginal cost is \$1.60 per unit (80 divided by 50).

What happens to marginal cost when the marginal product of labor decreases?

Marginal cost increases because each additional worker produces less output, raising the cost per unit.

At what point does marginal cost reach its minimum on the curve?

Marginal cost reaches its minimum when the marginal product of labor is at its maximum.

Why is understanding marginal cost important for production decisions?

It helps firms decide how much labor to employ and how much output to produce efficiently.

What does a sharp increase in marginal cost indicate about production?

It indicates that adding more workers is yielding much less additional output, so costs per unit rise quickly.

How does the marginal cost curve relate to aggregate supply and demand?

Marginal cost influences firms' supply decisions, which in turn affect the aggregate supply curve in the economy.

Back

Back

10:48

10:48