Skip to main content

Macroeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Perfect Competition and Efficiency definitions

You can tap to flip the card.

Perfect Competition

You can tap to flip the card.

👆

Perfect Competition

A market structure where many firms sell identical products, ensuring no single firm can influence the market price.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Recommended videos

Perfect Competition and Efficiency quiz

Perfect Competition and Efficiency

15 Terms

Guided course

06:46

Efficiency in Perfect Competition

4

views

Terms in this set (15)

Hide definitions

Perfect Competition

A market structure where many firms sell identical products, ensuring no single firm can influence the market price.

Productive Efficiency

Occurs when firms operate at the lowest possible cost, producing at the minimum point of average total cost.

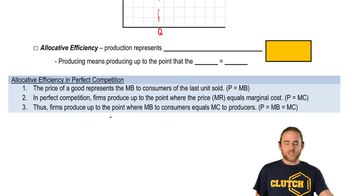

Allocative Efficiency

Achieved when resources are distributed so that consumer preferences are fully reflected, with price equaling marginal cost.

Average Total Cost

Represents the total cost per unit of output, minimized at the point of productive efficiency.

Marginal Benefit

The additional satisfaction or value a consumer receives from consuming one more unit of a good.

Marginal Cost

The extra cost incurred by a producer for making one additional unit of output.

Equilibrium Price

The market price at which the quantity demanded equals the quantity supplied, reflecting both consumer and producer interests.

Demand Curve

A graphical representation showing the relationship between the price of a good and the quantity consumers are willing to buy.

Supply Curve

A graphical depiction of the relationship between the price of a good and the quantity producers are willing to sell.

Marginal Revenue

The additional income a firm receives from selling one more unit, equal to price in perfect competition.

Economic Welfare

The overall well-being and satisfaction derived from the allocation of resources in a market.

Consumer Preferences

The desires and priorities that guide buyers' choices and influence market demand.

Resource Allocation

The process of distributing inputs among different uses to maximize satisfaction and efficiency.

Profit Maximizing Point

The output level where marginal revenue equals marginal cost, ensuring optimal earnings for firms.

Market Structure

The organizational and competitive characteristics of a market, influencing efficiency outcomes.

BackBack

BackBack

06:46

06:46