Back

BackMacroeconomics: Aggregate Demand and Aggregate Supply

02:56

02:56

Terms in this set (28)

Consumption (C), Investment (I), Government purchases (G), and Net exports (NX).

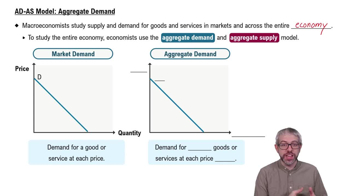

The relationship between the price level and the quantity of real GDP demanded by households, firms, and government.

Due to the wealth effect, interest-rate effect, and international-trade effect, where higher price levels reduce consumption, investment, and net exports.

As the price level rises, the real value of household wealth declines, leading to lower consumption.

Higher price levels increase money demand, raising interest rates and discouraging investment spending.

Higher domestic price levels make exports more expensive and imports cheaper, reducing net exports.

A change in the price level holding other factors constant.

A change in any component of real GDP other than the price level, such as government purchases or consumer expectations.

Interest rates, government purchases, and households' expectations of future income.

They raise borrowing costs, reducing consumption and investment, shifting AD left.

SRAS is upward sloping due to sticky wages/prices; LRAS is vertical, reflecting potential GDP independent of price level.

Because wages and prices are sticky due to contracts, slow adjustments, and menu costs, causing output to increase with price level.

Changes in labor force, capital stock, productivity, expected future price level, and supply shocks like natural disasters.

SRAS shifts left as wages and prices rise in anticipation of higher costs.

An unexpected event that shifts the SRAS curve, such as a sudden increase in oil prices or a pandemic.

When AD and SRAS intersect at the LRAS level, meaning GDP is at full employment and price expectations are met.

It causes a recession with lower output and employment as equilibrium moves left along SRAS.

Wages and prices adjust, shifting SRAS to restore equilibrium at potential GDP but with a different price level.

A combination of inflation and recession caused by a negative supply shock shifting SRAS left.

Both AD and SRAS shifted left due to reduced consumption, investment, and supply disruptions, lowering GDP.

A model incorporating continual growth in real GDP and shifts in AD, SRAS, and LRAS over time.

When aggregate demand grows faster than aggregate supply, pushing prices up over time.

The end of the housing bubble, the financial crisis, and a rapid increase in oil prices (supply shock).

Wages and prices are sticky, causing short-run fluctuations in output and employment.

Fluctuations in real output are mainly caused by changes in the money supply; advocates steady monetary growth.

Workers and firms have rational expectations and adjust quickly, minimizing output fluctuations.

Real productivity shocks as the main cause of business cycles, with aggregate supply vertical even in the short run.

Central bank-induced low interest rates cause overinvestment, leading to cycles of boom and bust.