Back

BackA Brief History of Financial Crises: Macroeconomic Perspectives

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

A Brief History of Financial Crises

Introduction to Financial Crises

Financial crises are significant disruptions in financial markets, often leading to severe economic downturns. Understanding their causes, mechanisms, and consequences is essential for macroeconomics students, as these events shape monetary policy, fiscal responses, and long-term economic growth.

Historical Examples of Financial Crises

Tulip Mania (1636-1637)

The Dutch Tulip Mania is one of the earliest recorded speculative bubbles. During this period, the prices of tulip bulbs soared to extraordinary heights before collapsing suddenly, causing widespread financial distress.

Speculative Bubble: A situation where asset prices rise far above their intrinsic value, driven by exuberant market behavior.

Crash: The inevitable sharp decline in prices, leading to financial losses for investors.

Example: In 1637, a single Semper Augustus tulip bulb was worth more than a mansion in Amsterdam.

Modern Asset Bubbles

Asset bubbles are not confined to history; modern markets have experienced similar phenomena, such as the Dotcom Bubble (2000), the rise and fall of Bitcoin, and the WeWork valuation collapse. These events illustrate recurring patterns of speculative excess and correction.

Dotcom Bubble: Technology stocks soared in the late 1990s, only to crash in 2000.

Cryptocurrency Volatility: Bitcoin's price history shows rapid appreciation followed by sharp declines.

Corporate Valuations: Companies like WeWork experienced dramatic valuation swings, reflecting speculative investment behavior.

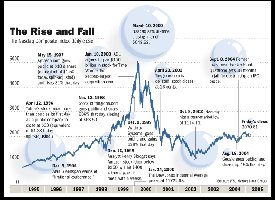

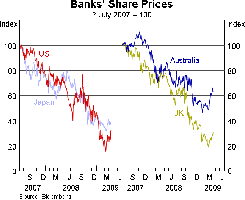

The 2008-2009 Global Financial Crisis

Overview and Timeline

The 2008-2009 crisis was the most severe financial crisis since the Great Depression. It began with the collapse of the subprime mortgage market and quickly spread to the global financial system, resulting in massive bank failures, government bailouts, and a deep recession.

Banking Crisis: Marked by bank runs, closures, mergers, and large-scale government interventions.

Market Failure: Occurs when market incentives lead to inefficient outcomes, often requiring government intervention.

Government Failure: When political processes result in actions that conflict with economic efficiency.

Economic Efficiency: Achieved when all actions generating more benefit than cost are undertaken, and none generating more cost than benefit are pursued.

Consequences of the Crisis

Bank Failures: 140 U.S. banks failed in 2009.

Foreclosures: Over 1.2 million foreclosures started in the first half of 2008.

Unemployment: U.S. unemployment peaked at 10% in October 2009.

Government Response: The Troubled Asset Relief Program (TARP) allocated $700 billion to stabilize the financial system.

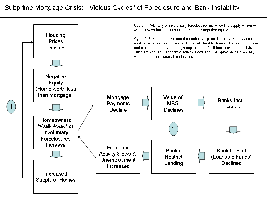

Mechanics of a Banking Crisis

During a banking crisis, liquidity dries up, making it impossible for individuals and businesses to access funds. This can halt economic activity and lead to widespread job losses and payment failures.

Bank Runs: Sudden withdrawals by depositors fearing bank insolvency.

Liquidity Crisis: Banks and businesses cannot access cash, leading to payment failures.

Causes of the 2008 Crisis

Regulatory Failures: Inadequate oversight of financial institutions.

Corporate Governance Failures: Poor risk management and excessive leverage.

Risky Investments: Proliferation of subprime mortgages and mortgage-backed securities.

Lack of Transparency: Complex financial products obscured true risk.

Government Unpreparedness: Inconsistent and delayed responses exacerbated panic.

Major U.S. Financial Crises in the 20th & 21st Centuries

The Great Depression (1929-1939)

The Great Depression was triggered by the 1929 stock market crash and worsened by the Federal Reserve's contraction of the money supply. Unemployment soared to 25%, and economic output did not recover until World War II.

Bank Failures: Widespread bank runs and closures.

Policy Response: Creation of the FDIC, SEC, and other regulatory bodies.

Monetary Policy Error: The Federal Reserve raised interest rates and reduced the money supply, deepening the depression.

The Panic of 1907

The Panic of 1907 was a severe banking crisis that led to the creation of the Federal Reserve System. The crisis was triggered by failed speculation and the inability of trust companies to access liquidity.

No Central Bank: The absence of a lender of last resort exacerbated the crisis.

Aftermath: The Federal Reserve was established to prevent future panics.

The Crash of 1987

On October 19, 1987, global stock markets crashed, with the Dow Jones Industrial Average falling 22.6% in one day. Quick intervention by the Federal Reserve prevented a broader economic collapse.

Portfolio Insurance: Use of derivatives accelerated the crash.

Fed Response: Provided liquidity, preventing a depression.

Theories and Models of Financial Crises

Minsky's Model of Financial Instability

Hyman Minsky developed a model explaining how financial systems are inherently prone to cycles of boom and bust. According to Minsky, periods of economic stability encourage risk-taking, leading to financial fragility and eventual crisis.

Pro-cyclical Credit: Credit expands during booms and contracts during busts.

Stages: Displacement, euphoria, mania, distress, and panic.

Lender of Last Resort: Central banks must provide liquidity during crises to prevent systemic collapse.

Bagehot's Doctrine

Walter Bagehot argued that central banks should lend freely to solvent banks with good collateral during crises, but at a penalty rate. This principle underpins modern central banking and crisis management.

Moral Hazard: The risk that safety nets encourage reckless behavior by financial institutions.

Federal Reserve: Acts as the U.S. lender of last resort.

Key Definitions and Concepts

Banking Crisis: Marked by bank runs, closures, and government interventions.

Market Failure: When market outcomes are not economically efficient.

Government Failure: Inefficiency resulting from government intervention.

Economic Efficiency: Maximizing net benefits from economic activities.

Summary Table: Major U.S. Financial Crises

Year | Crisis | Main Cause | Key Consequence |

|---|---|---|---|

1907 | Panic of 1907 | Speculation, no central bank | Creation of Federal Reserve |

1929-1933 | Great Depression | Stock market crash, monetary contraction | 25% unemployment, new regulations |

1987 | Stock Market Crash | Portfolio insurance, derivatives | No depression, Fed intervention |

2008-2009 | Global Financial Crisis | Subprime mortgages, regulatory failure | Bank failures, recession, bailouts |

Conclusion

Financial crises are recurring events in economic history, often resulting from a combination of speculative bubbles, regulatory failures, and macroeconomic imbalances. Understanding their causes and consequences is crucial for designing effective monetary and fiscal policies to mitigate future crises.