Back

BackBanks and Financial Intermediation: Structure, Functions, and Risks

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Banks and Financial Intermediation

Introduction to Financial Intermediaries

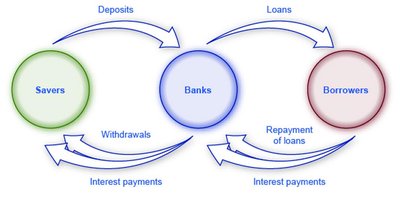

Banks and other financial intermediaries play a crucial role in the macroeconomy by channeling funds from savers to borrowers. They help allocate resources efficiently, support investment, and facilitate economic growth. In addition to banks, other financial institutions such as asset management companies, hedge funds, private equity funds, venture capital funds, and the shadow banking system also perform intermediation functions.

Financial Intermediaries: Organizations that connect savers (suppliers of capital) with borrowers (users of capital).

Examples: Banks, asset management companies, hedge funds, private equity funds, venture capital funds, shadow banking system.

Bank Balance Sheets: Assets and Liabilities

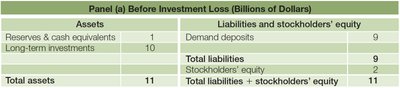

A bank's balance sheet records its assets (what it owns) and liabilities (what it owes). Understanding the structure of a bank's balance sheet is essential for analyzing its financial health and risk exposure.

Assets: Resources owned by the bank, such as reserves, cash equivalents, and long-term investments.

Liabilities: Obligations the bank owes to others, including demand deposits, short-term borrowing, and long-term debt.

Stockholders’ Equity: The difference between total assets and total liabilities; represents the net value owned by shareholders.

Balance Sheet Equation:

Example: Illustrative Bank Balance Sheet

Assets | Liabilities and Stockholders’ Equity | ||

|---|---|---|---|

Reserves & cash equivalents | 1 | Demand deposits | 9 |

Long-term investments | 10 | Total liabilities | 9 |

Stockholders’ equity | 2 | ||

Total assets | 11 | Total liabilities + stockholders’ equity | 11 |

Key Functions of Banks

1. Identifying Profitable Lending Opportunities

Banks attract a large pool of potential borrowers and use their expertise to select the most creditworthy applicants. This process helps allocate funds to the most productive uses in the economy.

Screening: Evaluating loan applications to minimize default risk.

Example: Banks assess credit scores, income, and collateral before approving loans.

2. Maturity Transformation

Banks transform short-term liabilities (such as demand deposits) into long-term assets (such as business and real estate loans). This process is known as maturity transformation.

Maturity: The time until a debt must be repaid.

Short-term liabilities: Deposits and borrowings that can be withdrawn at any time (0-year maturity).

Long-term assets: Loans and investments with maturities ranging from several years to decades.

3. Risk Management through Diversification

Banks manage risk by holding a diversified portfolio of assets, including mortgages, consumer loans, business loans, and government debt. Diversification reduces the likelihood that all assets will underperform simultaneously.

Diversification: Spreading investments across different asset types to reduce risk.

Limitation: Diversification cannot eliminate systemic risk, as seen during financial crises.

Bank Insolvency and the Role of the FDIC

Bank Insolvency

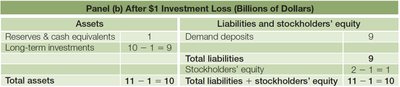

A bank becomes insolvent when the value of its assets falls below the value of its liabilities, resulting in negative stockholders’ equity. In such cases, the bank cannot meet its obligations to depositors and creditors.

Stockholders’ Equity: Absorbs losses first; if it reaches zero, the bank is insolvent.

FDIC Insurance: Protects depositors by insuring deposits up to $250,000 per account.

Example: Impact of Asset Losses on Bank Balance Sheet

Assets | Liabilities and Stockholders’ Equity | ||

|---|---|---|---|

Reserves & cash equivalents | 1 | Demand deposits | 9 |

Long-term investments | 10 - 1 = 9 | Total liabilities | 9 |

Stockholders’ equity | 2 - 1 = 1 | ||

Total assets | 11 - 1 = 10 | Total liabilities + stockholders’ equity | 11 - 1 = 10 |

The Role of the FDIC

The Federal Deposit Insurance Corporation (FDIC) insures bank deposits and intervenes when banks fail. The FDIC may shut down a failed bank and compensate depositors or transfer the bank to new ownership to protect depositors.

FDIC Actions: Shut down operations and pay depositors, or transfer ownership to protect all depositors.

Bank Runs and Systemic Risk

Bank Runs

A bank run occurs when a large number of depositors simultaneously withdraw their funds due to concerns about the bank's solvency. This can force the bank to sell illiquid assets at a loss, potentially leading to insolvency.

Illiquid Assets: Assets that cannot be quickly converted to cash without significant loss in value.

Fire Sales: Selling assets rapidly at reduced prices to meet withdrawal demands.

Historical Bank Failures and Regulation

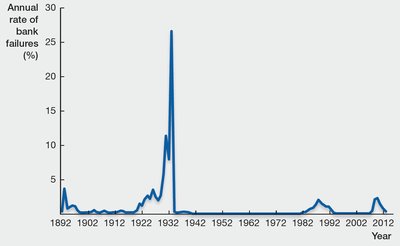

Waves of Bank Failures in the U.S.

Bank failures have occurred in waves throughout U.S. history, often during periods of economic distress. Major waves include the 1920s, the Great Depression, the savings and loan crisis, and the 2007–2009 financial crisis.

First wave: 1919–1928, mainly rural banks failed.

Second wave: 1929–1939, Great Depression, 9,000 banks failed.

Third wave: 1986–1995, savings and loan crisis.

Fourth wave: 2007–2009, collapse of several nonbank financial institutions.

Systemically Important Financial Institutions (SIFIs)

After the collapse of large institutions like Lehman Brothers, regulations were introduced for SIFIs, which are considered "too big to fail." These institutions must submit living wills and hold more equity to reduce systemic risk.

Living Will: A plan for how a SIFI would liquidate assets in a crisis.

Increased Equity Requirements: SIFIs must hold more stockholders’ equity to absorb losses.

Key Ideas and Summary

The credit market matches borrowers (demand for credit) and savers (supply of credit).

Credit market equilibrium determines the real interest rate.

Banks and financial intermediaries identify profitable lending opportunities, transform short-term deposits into long-term investments, and manage risk.

Banks become insolvent when liabilities exceed assets; FDIC insurance protects depositors.