Back

BackChapter 1: Economics—Foundations, Models, and Analytical Tools

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economics: Foundations and Models

Introduction to Economics

Economics is the study of how people make choices to attain their goals, given their scarce resources. Scarcity means that our unlimited wants exceed the limited resources available to fulfill those wants. Economists use models—simplified versions of reality—to analyze real-world economic situations and answer questions about prices, production, and policy.

Key Economic Questions

What determines the prices of goods and services?

Why do firms engage in international trade?

How do government policies affect markets?

1.1 Three Key Economic Ideas

People Are Rational

Economists assume that individuals and firms use all available information to achieve their goals. Rational agents weigh the benefits and costs of each action and make decisions that maximize their utility or profit.

Example: Apple sets iPhone prices to maximize profits, not randomly.

People Respond to Economic Incentives

Changes in incentives lead to changes in behavior. Incentives can be positive (rewards) or negative (penalties).

Example: DNA databases for felons reduce repeat offenses by increasing the likelihood of being caught.

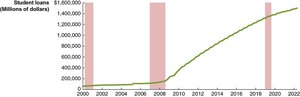

Application: Changes in student loan policies may unintentionally incentivize colleges to raise tuition or students to borrow more.

Optimal Decisions Are Made at the Margin

Most decisions involve small adjustments—doing a little more or less of something. Marginal analysis compares the additional benefit (marginal benefit, MB) and the additional cost (marginal cost, MC) of an action.

Marginal Analysis: Continue an activity as long as MB ≥ MC.

Example: Deciding whether to study an extra hour or watch TV.

1.2 The Economic Problem That Every Society Must Solve

Basic Economic Questions

Every society must answer three fundamental questions due to scarcity:

What goods and services will be produced? (Trade-offs and opportunity cost)

How will the goods and services be produced? (Choice of production methods)

Who will receive the goods and services produced? (Distribution of income and resources)

Opportunity Cost: The highest-valued alternative given up to engage in an activity.

Types of Economic Systems

Centrally Planned Economy: Government decides resource allocation.

Market Economy: Households and firms interact in markets to allocate resources.

Mixed Economy: Most decisions are made in markets, but government plays a significant role.

Efficiency and Equity

Productive Efficiency: Goods/services produced at lowest cost (competition).

Allocative Efficiency: Production matches consumer preferences (voluntary exchange).

Equity: Fair distribution of economic benefits (may conflict with efficiency).

1.3 Economic Models

Building and Testing Economic Models

Economic models are simplified frameworks for analyzing economic issues. The process involves:

Deciding on assumptions

Formulating a testable hypothesis

Using data to test the hypothesis

Revising the model as needed

Economic Variable: A measurable quantity that can change (e.g., employment, price).

Positive Analysis: What is (facts, cause and effect).

Normative Analysis: What ought to be (value judgments).

Economics as a Social Science

Economics studies individual and group behavior, similar to other social sciences, but with a focus on choices, incentives, and outcomes like prices and growth.

1.4 Microeconomics and Macroeconomics

Distinguishing Microeconomics and Macroeconomics

Microeconomics: Studies individual households, firms, and markets.

Macroeconomics: Studies the economy as a whole (inflation, unemployment, growth).

1.5 Economic Skills and Economics as a Career

Skills Developed in Economics

Critical thinking and problem-solving

Data analysis and interpretation

Understanding incentives and trade-offs

Economics majors often have higher average incomes, but causation versus correlation should be considered.

1.6 A Preview of Important Economic Terms

Key Terms

Technology: Processes used to produce goods and services.

Capital: Manufactured goods used to produce other goods and services.

Appendix: Using Graphs and Formulas

Graphs in Economics

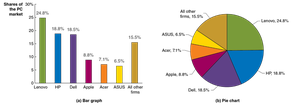

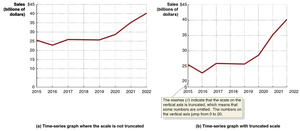

Graphs are visual tools to represent economic relationships. Common types include bar graphs, pie charts, and time-series graphs.

Plotting Economic Data

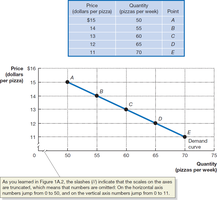

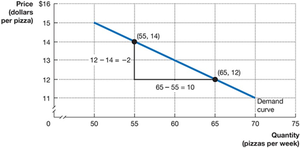

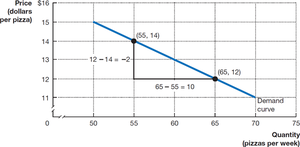

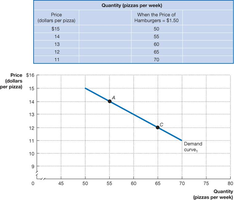

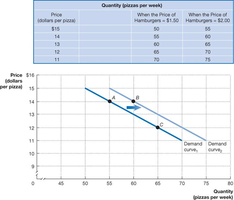

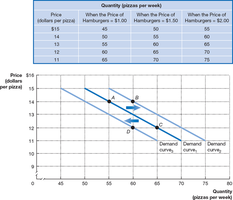

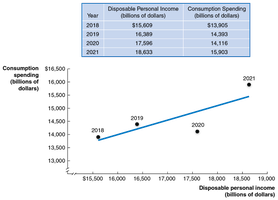

Graphs often plot price (vertical axis) against quantity (horizontal axis) to show relationships such as demand curves.

Calculating Slope

The slope of a line is the change in the y-variable divided by the change in the x-variable. For a demand curve, this shows how quantity demanded changes with price.

Formula:

Showing Three Variables on a Graph

Graphs can illustrate how a third variable (e.g., price of a related good) shifts the demand curve.

Positive and Negative Relationships

A positive relationship means both variables move in the same direction; a negative relationship means they move in opposite directions.

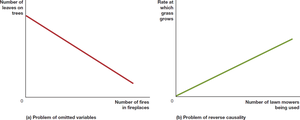

Cause and Effect in Graphs

Graphs can suggest relationships but do not prove causation. Omitted variables or reverse causality can mislead interpretation.

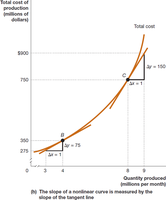

Linear and Nonlinear Relationships

Most economic relationships are nonlinear, meaning the slope changes at different points. The slope of a nonlinear curve can be approximated over a section or measured at a point using a tangent.

Formulas in Economics

Percentage Change:

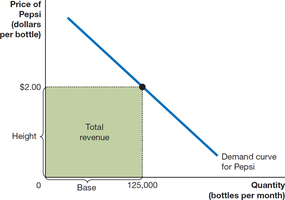

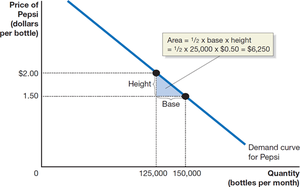

Areas on Graphs

The area of a rectangle (base × height) can represent total revenue. The area of a triangle (1/2 × base × height) is also used in economic analysis.

Summary of Using Formulas

Understand the economic concept the formula represents.

Use the correct formula for the problem.

Check that the result is economically reasonable.

Additional info: This chapter provides foundational concepts and analytical tools that will be used throughout the study of macroeconomics, including the use of graphs, models, and basic economic reasoning.