Back

BackChapter 2: Some Tools of the Economist – Core Concepts in Macroeconomics

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Opportunity Cost

Definition and Application

Opportunity cost is a fundamental concept in economics, referring to the value of the next best alternative that must be forgone when making a choice. All decisions involve trade-offs, and understanding opportunity cost helps individuals and societies allocate resources efficiently.

Definition: The opportunity cost of an action is the value of the best alternative that is not chosen.

Example: The opportunity cost of attending college includes both the monetary costs (tuition, books) and the non-monetary costs (forgone earnings from not working).

Application: If the opportunity cost of college rises (e.g., higher tuition or a lucrative job offer), individuals are less likely to attend college.

Trade and Value Creation

Trade, Mutual Gain, and Transaction Costs

Trade allows individuals and nations to specialize in the production of goods and services in which they have a comparative advantage, leading to mutual gains. Transaction costs, such as time, effort, and resources required to make an exchange, can reduce the benefits of trade. Middlemen often reduce transaction costs, facilitating more efficient markets.

Trade Creates Value: Voluntary exchange benefits both parties, as each values what they receive more than what they give up.

Transaction Costs: Costs associated with making an exchange, including searching for information, bargaining, and enforcing contracts.

Role of Middlemen: Middlemen lower transaction costs by bringing buyers and sellers together efficiently.

Property Rights and Incentives

The Importance of Private Property

Clearly defined and enforced property rights are essential for the efficient allocation of resources. They provide incentives for individuals to use resources productively, maintain them, and invest in improvements.

Private Property Rights: The right to use, control, and obtain benefits from a resource.

Incentives: Property rights encourage owners to maximize the value of their resources, leading to innovation and economic growth.

Markets: Private property is a cornerstone of market economies, enabling voluntary exchange and efficient resource allocation.

The Production Possibilities Curve (PPC)

Understanding the PPC

The Production Possibilities Curve illustrates the maximum combinations of two goods or services that can be produced with available resources and technology. It demonstrates the concepts of scarcity, choice, and opportunity cost.

Efficient Points: Points on the PPC represent efficient use of resources.

Inefficient Points: Points inside the PPC indicate underutilization of resources.

Unattainable Points: Points outside the PPC are not possible with current resources.

Example: A student dividing 10 hours between studying economics and English faces a trade-off, illustrated by the PPC.

Shifting the PPC

The PPC can shift outward with increases in resource availability, technological advancements, improved economic institutions, or by sacrificing current leisure for more work. These shifts represent economic growth and increased productive capacity.

Resource Base: More resources allow for greater production possibilities.

Technology: Technological improvements enable more efficient production.

Institutions: Better laws and policies can enhance productivity.

Work Effort: Increased labor input can temporarily boost output.

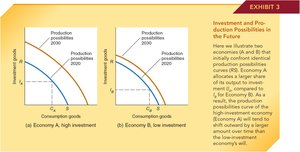

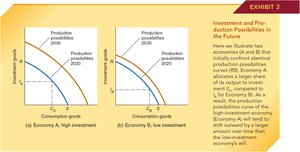

Investment and Future Production Possibilities

Investment in capital goods (such as equipment, buildings, and training) leads to greater future output. The choice between current consumption and investment determines the future position of the PPC.

High Investment: Allocating more resources to investment today shifts the PPC outward more rapidly in the future.

Low Investment: Focusing on current consumption limits future growth.

Entrepreneurship and Economic Growth

Role of Entrepreneurs and Innovation

Entrepreneurs drive economic growth by introducing new products, processes, and business models. Their willingness to take risks and innovate leads to shifts in the PPC and improvements in living standards.

Innovation: New ideas and technologies expand production possibilities.

Examples: Notable entrepreneurs have transformed industries and increased economic output.

Trade, Output, and Living Standards

Division of Labor and Comparative Advantage

Specialization and division of labor increase productivity and output. The law of comparative advantage states that individuals or nations should specialize in producing goods for which they have the lowest opportunity cost, leading to mutual gains from trade.

Division of Labor: Assigning specific tasks to individuals increases efficiency.

Comparative Advantage: Specialization based on comparative advantage maximizes total output.

Mass Production: Large-scale production methods further enhance efficiency and innovation.

Economic Organization

Basic Economic Questions and Systems

All economies must answer three basic questions: What to produce? How to produce? For whom to produce? The answers depend on the economic system in place, such as market organization or political planning.

Market Organization: Decisions are made by individuals and firms through voluntary exchange in markets.

Political Planning: Government authorities make production and distribution decisions.

Comparative Systems: Some countries blend market and planned elements; for example, Scandinavian countries combine market economies with extensive social welfare policies.

Keys to Prosperity

Human Ingenuity and Wealth Creation

Long-term economic prosperity depends on human ingenuity, innovation, and the effective use of resources. Societies that encourage creativity, protect property rights, and facilitate trade tend to achieve higher living standards.

Wealth Creation: Driven by innovation, investment, and efficient resource allocation.

Institutions: Strong legal and economic institutions support growth and prosperity.