Back

BackChapter 2: The Economic Problem – Production Possibilities, Opportunity Cost, and Economic Growth

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Production Possibilities and Opportunity Cost

Production Possibilities Frontier (PPF)

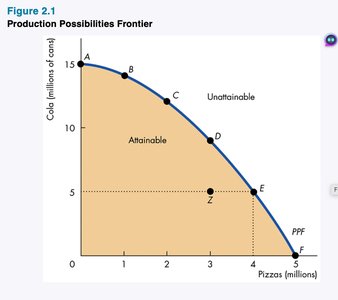

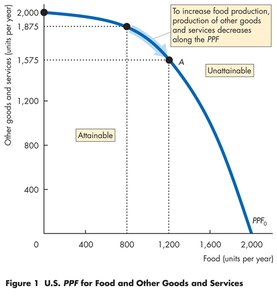

The Production Possibilities Frontier (PPF) is a fundamental economic model that illustrates the maximum combinations of two goods or services that can be produced with available resources and technology. The PPF demonstrates the concept of scarcity, tradeoffs, and opportunity cost.

Attainable Points: Combinations of goods that can be produced using available resources (on or inside the PPF).

Unattainable Points: Combinations outside the PPF, which cannot be produced with current resources and technology.

Inefficiency: Points inside the PPF indicate underutilized or misallocated resources.

Possibility | Pizzas (millions) | Cola (millions of cans) |

|---|---|---|

A | 0 | 15 |

B | 1 | 14 |

C | 2 | 12 |

D | 3 | 9 |

E | 4 | 5 |

F | 5 | 0 |

Additional info: The table above lists the production possibilities for cola and pizzas, corresponding to points on the PPF.

Production Efficiency

Production efficiency is achieved when goods and services are produced at the lowest possible cost, which occurs at all points on the PPF. Inefficiency arises when resources are unused or misallocated.

Unused Resources: Idle factories or unemployed workers.

Misallocated Resources: Assigning workers to tasks for which they are not best suited.

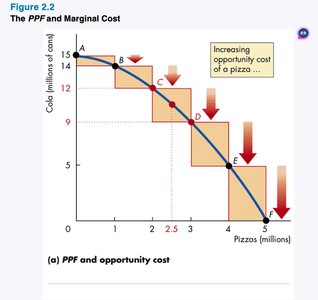

Tradeoff Along the PPF

Moving along the PPF involves a tradeoff: producing more of one good requires producing less of another due to limited resources.

Opportunity Cost

The opportunity cost of an action is the highest-valued alternative forgone. On the PPF, the opportunity cost of producing more of one good is the amount of the other good that must be given up.

Opportunity Cost as a Ratio:

Increasing Opportunity Cost: The PPF is bowed outward because resources are not equally productive in all activities, leading to increasing opportunity costs as more of one good is produced.

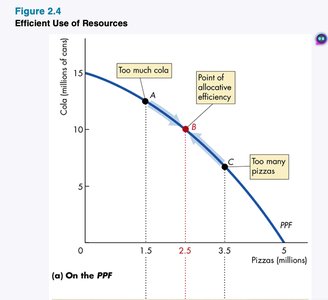

Using Resources Efficiently

Allocative Efficiency

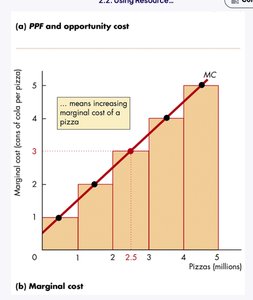

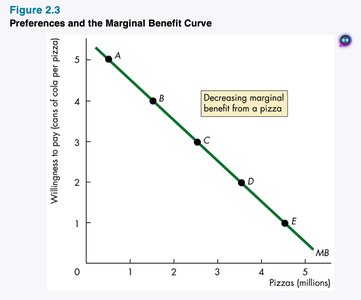

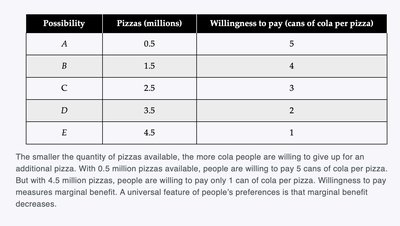

Allocative efficiency occurs when resources are used to produce the combination of goods and services most highly valued by society. This is achieved at the point on the PPF where marginal benefit equals marginal cost.

Marginal Cost (MC): The opportunity cost of producing one more unit of a good, measured by the slope of the PPF.

Marginal Benefit (MB): The benefit received from consuming one more unit of a good, measured by the maximum willingness to pay.

Principle of Decreasing Marginal Benefit: As more of a good is consumed, its marginal benefit decreases.

Possibility | Pizzas (millions) | Willingness to pay (cans of cola per pizza) |

|---|---|---|

A | 0.5 | 5 |

B | 1.5 | 4 |

C | 2.5 | 3 |

D | 3.5 | 2 |

E | 4.5 | 1 |

Gains from Trade

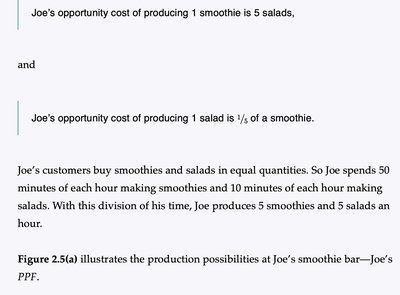

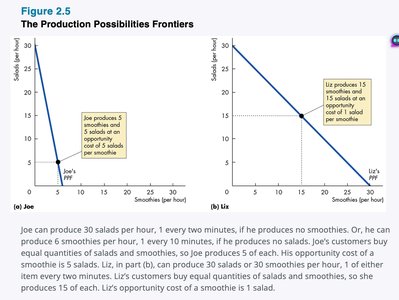

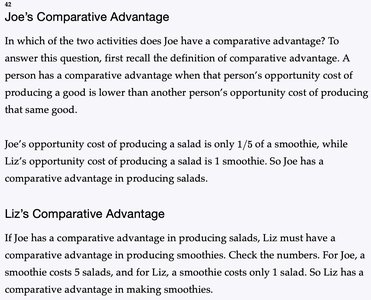

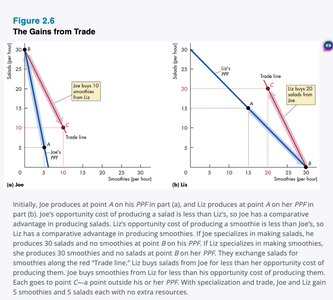

Comparative and Absolute Advantage

Comparative advantage exists when a person can produce a good at a lower opportunity cost than another. Absolute advantage refers to higher productivity in producing a good.

Specialization: Individuals or nations gain by specializing in goods where they have a comparative advantage and trading for others.

Item | Minutes to produce 1 | Quantity per hour |

|---|---|---|

Smoothies (Joe) | 10 | 6 |

Salads (Joe) | 2 | 30 |

Item | Minutes to produce 1 | Quantity per hour |

|---|---|---|

Smoothies (Liz) | 2 | 30 |

Salads (Liz) | 2 | 30 |

Joe's opportunity cost: 1 smoothie = 5 salads; 1 salad = 1/5 smoothie. Liz's opportunity cost: 1 smoothie = 1 salad; 1 salad = 1 smoothie.

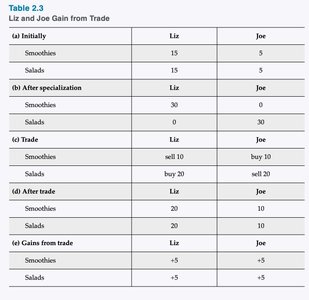

Gains from Specialization and Trade

Smoothies (Liz) | Salads (Liz) | Smoothies (Joe) | Salads (Joe) | |

|---|---|---|---|---|

Initially | 15 | 15 | 5 | 5 |

After specialization | 30 | 0 | 0 | 30 |

After trade | 20 | 20 | 10 | 10 |

Gains from trade | +5 | +5 | +5 | +5 |

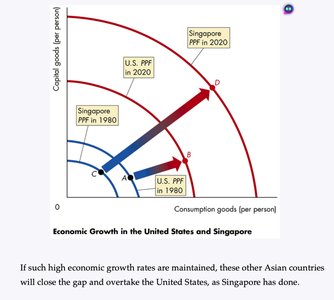

Economic Growth

Sources and Costs of Economic Growth

Economic growth is the expansion of production possibilities, typically resulting from technological change and capital accumulation. However, growth requires sacrificing current consumption for future gains.

Technological Change: Development of new goods or better production methods.

Capital Accumulation: Growth of capital resources, including human capital.

Opportunity Cost of Growth: Producing more capital goods today means fewer consumption goods now, but more in the future.

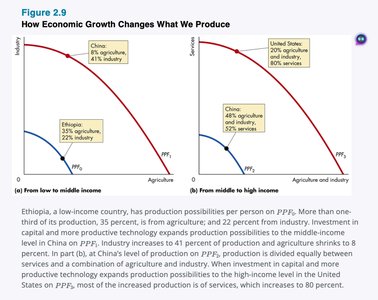

Changes in What We Produce

As economies grow, the composition of output changes. Low-income countries focus on agriculture, middle-income countries on industry, and high-income countries on services.

Economic Coordination

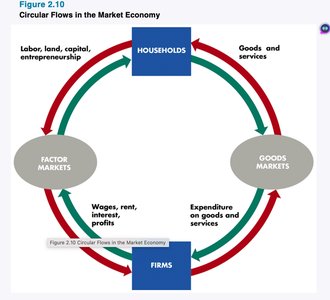

Markets and the Circular Flow

Efficient economic coordination requires decentralized decision-making through markets, supported by social institutions such as firms, property rights, and money.

Firms: Organize production and hire factors of production.

Markets: Arrangements that enable buyers and sellers to exchange goods and services.

Property Rights: Legal rights to use and dispose of resources.

Money: A generally accepted medium of exchange.

Market Coordination and Price Adjustments

Markets coordinate decisions through price adjustments, ensuring that supply and demand are balanced. When there is excess demand, prices rise; when there is excess supply, prices fall.

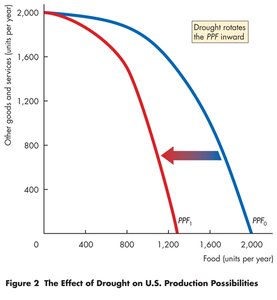

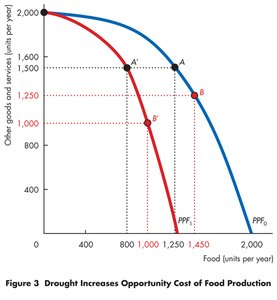

Case Study: The Effect of Drought on the U.S. PPF

Natural disasters, such as droughts, can shift the PPF inward, reducing the economy's capacity to produce certain goods and increasing opportunity costs.

Efficient Response: Killing crops that won't mature can be efficient if it prepares land for future production, ensuring resources are not wasted.