Back

BackClassical and Keynesian Macro Analyses: Short-Run Equilibrium, Aggregate Supply, and Inflation

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Classical and Keynesian Macro Analyses

Introduction

This chapter explores the foundations of macroeconomic theory, focusing on the classical and Keynesian models. It examines how equilibrium real GDP and the price level are determined in the short run, the nature of aggregate supply, and the causes and consequences of inflation and economic shocks.

The Classical Model

Overview of the Classical Model

The classical model, developed by economists such as Adam Smith, J.B. Say, and David Ricardo, was the first systematic attempt to explain the determinants of the price level, real GDP, employment, consumption, saving, and investment. It assumes flexible wages and prices and competitive markets throughout the economy.

Key Assumptions: Pure competition, flexible wages and prices, rational self-interest, and absence of money illusion.

Money Illusion: Occurs when individuals react to changes in nominal prices rather than real (relative) prices.

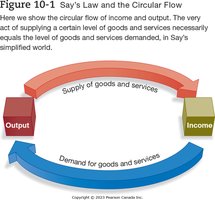

Say’s Law and the Circular Flow

Say’s Law states that supply creates its own demand. The act of producing goods and services generates the means and willingness to purchase other goods and services, ensuring that desired expenditures equal actual expenditures.

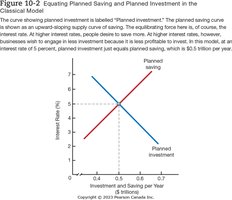

Equilibrium in the Credit Market

In the classical model, saving is a leakage from the circular flow, but it is matched by business investment. The interest rate adjusts to ensure that the amount of credit demanded equals the amount supplied, maintaining equilibrium where saving equals investment ().

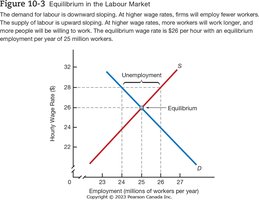

Labour Market Equilibrium

The classical model assumes that wages adjust to ensure full employment. The demand for labour is downward sloping, while the supply is upward sloping. The equilibrium wage rate ensures that the quantity of labour supplied equals the quantity demanded.

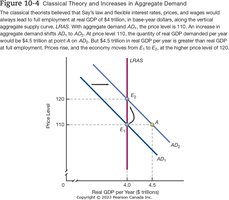

Aggregate Supply and Price Level in the Classical Model

In the classical model, the long-run aggregate supply (LRAS) curve is vertical, indicating that real GDP is fixed at the full-employment level. Changes in aggregate demand affect only the price level, not real GDP.

Effect of a Decrease in Aggregate Demand

A decrease in aggregate demand leads to a temporary fall in real GDP and increased unemployment, but competition among workers and firms pushes wages and prices down, returning the economy to full employment.

Keynesian Economics and the Keynesian Short-Run Aggregate Supply Curve

Key Features of Keynesian Economics

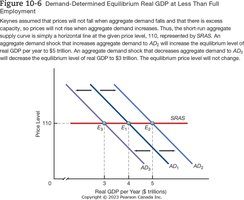

Keynesian economics emerged in response to the Great Depression, arguing that prices and wages are inflexible or "sticky" downward. As a result, changes in aggregate demand affect output and employment rather than prices, especially when there is excess capacity.

Sticky Prices and Wages: Due to contracts and institutional factors, prices and wages do not adjust quickly to changes in demand.

Horizontal SRAS: The short-run aggregate supply curve is horizontal when there is significant unemployment and unused capacity.

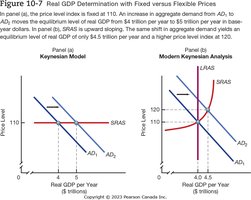

Modern Keynesian Analysis

Modern Keynesian analysis recognizes that prices are not completely sticky. The short-run aggregate supply curve (SRAS) is upward sloping, reflecting partial price adjustment. Increases in aggregate demand can raise both output and the price level.

Shifts in the Aggregate Supply Curve

Determinants of Aggregate Supply

Both short-run and long-run aggregate supply curves can shift due to changes in the factors of production (labour, capital, technology). Temporary changes in input prices affect only the SRAS, while permanent changes affect both SRAS and LRAS.

Consequences of Changes in Aggregate Demand

Aggregate Demand and Supply Shocks

An aggregate demand shock shifts the AD curve, while an aggregate supply shock shifts the AS curve. These shocks can create gaps between equilibrium real GDP and full-employment real GDP.

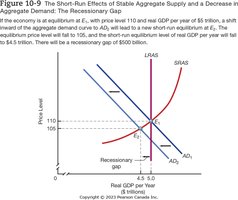

Recessionary Gap

A recessionary gap occurs when equilibrium real GDP is less than full-employment real GDP, typically due to a leftward shift in aggregate demand.

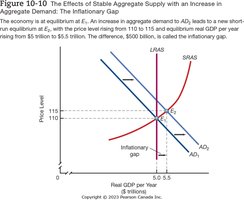

Inflationary Gap

An inflationary gap occurs when equilibrium real GDP exceeds full-employment real GDP, usually following a rightward shift in aggregate demand.

Explaining Short-Run Variations in Inflation

Types of Inflation

Demand-Pull Inflation: Caused by increases in aggregate demand not matched by increases in aggregate supply.

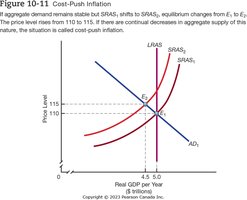

Cost-Push Inflation: Caused by decreases in short-run aggregate supply, often due to rising input costs.

Summary Table: Classical vs. Keynesian Models

Feature | Classical Model | Keynesian Model |

|---|---|---|

Wage & Price Flexibility | Fully flexible | Sticky downward |

SRAS Curve | Vertical at full employment | Horizontal (or upward sloping in modern analysis) |

Role of Aggregate Demand | Determines price level | Determines output (when below full employment) |

Unemployment | Temporary, self-correcting | Can persist without intervention |

Key Equations

Equilibrium in Credit Market:

Aggregate Demand (AD):

Aggregate Supply (AS): where = labour, = capital, = technology

Conclusion

The classical and Keynesian models provide contrasting views on how the economy adjusts to shocks and determines output and prices in the short run. Understanding these models is essential for analyzing macroeconomic policy and the causes of inflation, unemployment, and economic growth.