Back

BackDynamic Change, Economic Fluctuations, and the AD-AS Model

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Dynamic Change, Economic Fluctuations, and the AD-AS Model

Anticipated and Unanticipated Changes

Macroeconomic outcomes are influenced by both anticipated and unanticipated changes. Understanding the distinction between these is crucial for analyzing economic fluctuations.

Anticipated changes: These are expected by economic participants, allowing decision makers time to adjust before the changes occur.

Unanticipated changes: These catch people by surprise, often leading to short-term disruptions in output and employment.

Aggregate Demand and Aggregate Supply

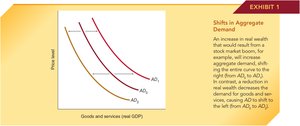

Factors That Shift Aggregate Demand

Aggregate demand (AD) can shift due to changes in real wealth, consumer optimism, fiscal policy, and other factors. These shifts affect the overall demand for goods and services in the economy.

Increase in real wealth: Events like a stock market boom increase aggregate demand, shifting the AD curve to the right.

Decrease in real wealth: Reduces aggregate demand, shifting the AD curve to the left.

Consumer sentiment: Optimism increases AD, while pessimism decreases AD. The consumer sentiment index often declines before or during recessions.

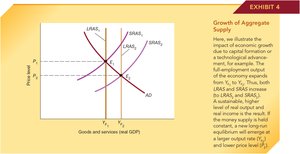

Shifts in Aggregate Supply

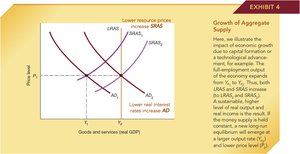

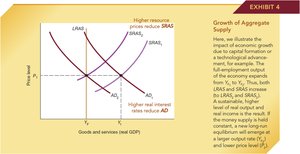

Aggregate supply (AS) can shift in both the short run (SRAS) and long run (LRAS) due to changes in resource prices, technology, and capital stock.

Increase in capital or technology: Expands potential output, shifting LRAS (and SRAS) to the right.

Reduction in resource prices or favorable weather: Shifts SRAS to the right, increasing output in the short run.

Steady Economic Growth and Anticipated Changes in LRAS

Steady, predictable economic growth—such as from capital formation or technological progress—shifts the LRAS curve to the right. If anticipated, these changes do not disrupt macroeconomic equilibrium.

Both LRAS and SRAS increase, expanding full employment output.

A sustainable, higher level of real output is achieved.

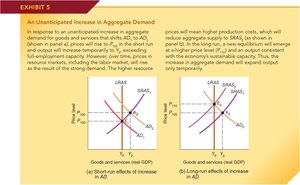

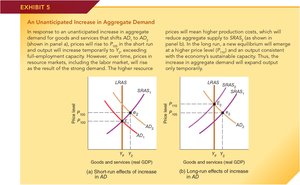

Unanticipated Changes and Market Adjustments

Unanticipated Changes in Aggregate Demand

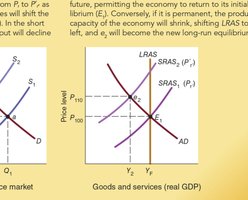

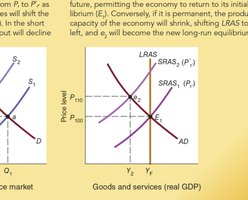

Unanticipated changes in AD cause output to deviate from full employment in the short run, as prices adjust more slowly than quantities.

Unanticipated Increase in Aggregate Demand

Short-run: Output temporarily exceeds full-employment capacity, and prices rise.

Long-run: Resource prices (including wages) rise, shifting SRAS leftward. Output returns to long-run potential, but at a higher price level.

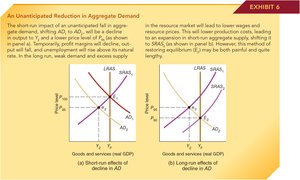

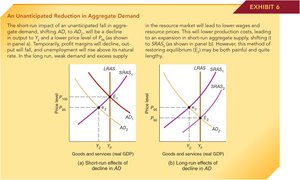

Unanticipated Decrease in Aggregate Demand

Short-run: Output falls below full employment, price level drops, and unemployment rises.

Long-run: Resource prices fall, shifting SRAS rightward. Output returns to long-run potential, but at a lower price level.

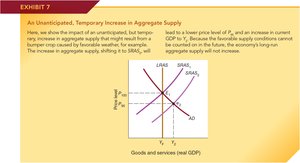

Unanticipated Changes in Short-Run Aggregate Supply (Supply Shocks)

Supply shocks are unexpected events that temporarily increase or decrease aggregate supply.

Positive supply shock: (e.g., bumper crop) increases SRAS, lowering prices and increasing output temporarily.

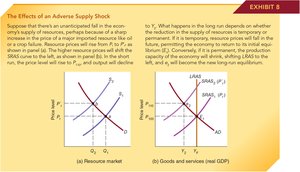

Negative supply shock: (e.g., oil price spike) decreases SRAS, raising prices and reducing output.

The Price Level, Inflation, and the AD-AS Model

Inflation and Expectations

The relationship between actual and expected inflation affects firm behavior and output:

If actual inflation < expected, firms incur losses and reduce output.

If actual inflation > expected, profits rise and firms expand output.

Unanticipated Changes, Recessions, and Booms

The AD-AS Model and Instability

Short-run deviations from full employment output (YF) can occur due to unanticipated changes, but two forces help restore equilibrium:

Interest rates adjust, shifting AD.

Resource prices adjust, shifting SRAS.

Macro-Adjustment Process

If output < YF: Falling interest rates increase AD; lower resource prices increase SRAS, moving output toward YF.

If output > YF: Rising interest rates decrease AD; higher resource prices decrease SRAS, moving output toward YF.

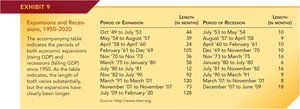

Expansions and Recessions: The Historical Record

Economic expansions have historically lasted longer than recessions. The Great Recession of 2008-2009 was notable for its depth and severity.

Period of Expansion | Length (months) | Period of Recession | Length (months) |

|---|---|---|---|

Oct '49 to July '53 | 45 | Aug '57 to May '58 | 10 |

May '54 to Aug '57 | 39 | Apr '60 to Feb '61 | 10 |

Apr '58 to Apr '60 | 24 | Dec '69 to Nov '70 | 11 |

Feb '61 to Dec '69 | 106 | Nov '73 to Mar '75 | 16 |

Nov '70 to Nov '73 | 36 | Jan '80 to July '80 | 6 |

Mar '75 to Jan '80 | 58 | July '81 to Nov '82 | 16 |

July '80 to July '81 | 12 | July '90 to Mar '91 | 8 |

Nov '82 to July '90 | 92 | Mar '01 to Nov '01 | 8 |

Mar '91 to Mar '01 | 120 | Dec '07 to June '09 | 18 |

Nov '01 to Dec '07 | 73 | ||

June '09 to February '20 | 128 |

Changes in Stock and Housing Prices During Expansions and Recessions

Stock and housing prices typically rise before and during expansions, increasing AD. Conversely, they fall before and during recessions, reducing AD. The wealth effects from these price swings contribute to the business cycle's ups and downs. The 2008-2009 recession saw especially large declines in both housing and stock prices, intensifying the downturn.

Key Equations and Concepts

Aggregate Demand (AD):

Short-Run Aggregate Supply (SRAS): Upward sloping due to sticky wages and prices.

Long-Run Aggregate Supply (LRAS): Vertical at full-employment output (YF).

Example: A positive supply shock (e.g., a bumper crop) shifts SRAS to the right, temporarily increasing output and lowering prices. If the shock is temporary, SRAS returns to its original position; if permanent, LRAS may also shift.

Additional info: The AD-AS model is central to understanding macroeconomic fluctuations, policy responses, and the business cycle.