Back

BackEconomic Growth: Concepts, Measurement, and Sources

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Growth

The Basics of Economic Growth

Economic growth refers to the sustained expansion of production possibilities, measured as the increase in real GDP over a given period. Understanding economic growth is essential for analyzing improvements in a nation's standard of living and long-term prosperity.

Economic Growth Rate: The annual percentage change of real GDP, indicating how rapidly the total economy is expanding.

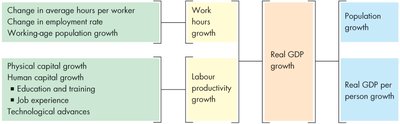

Standard of Living: Depends on real GDP per person, calculated as real GDP divided by the population. Real GDP per person increases only if real GDP grows faster than the population.

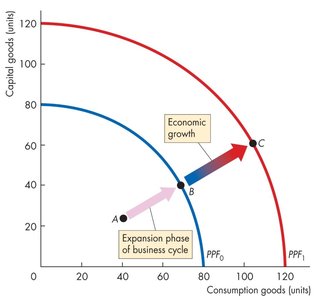

Economic Growth Versus Business Cycle Expansion

Business Cycle Expansion: A return to full employment during an expansion phase is not considered economic growth; it is a movement from inside the production possibilities frontier (PPF) to a point on the PPF.

Economic Growth: The outward shift of the PPF, representing an increase in potential GDP.

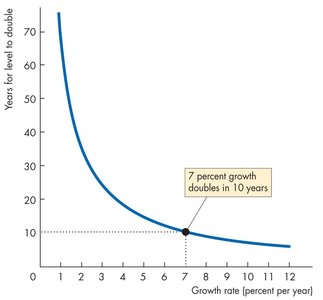

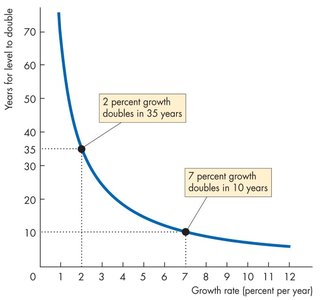

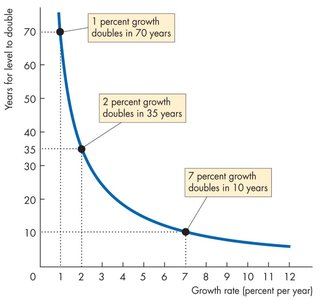

The Rule of 70

The Rule of 70 estimates the number of years required for a variable to double, calculated as 70 divided by the annual percentage growth rate.

For example, a 7% growth rate doubles a variable in 10 years; a 2% rate doubles it in 35 years; a 1% rate doubles it in 70 years.

How Potential GDP Grows

Economic growth is defined as the sustained, year-on-year increase in potential GDP, not just a one-time rise in real GDP or a recovery from recession.

What Determines Potential GDP?

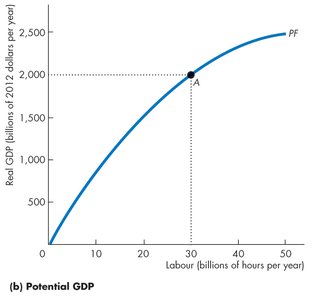

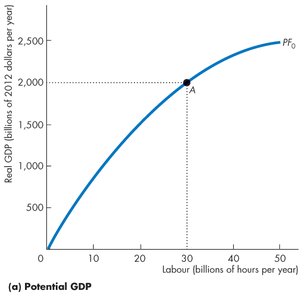

Potential GDP: The quantity of real GDP produced when the quantity of labour employed is at the full-employment level.

Determined by the aggregate production function and the aggregate labour market.

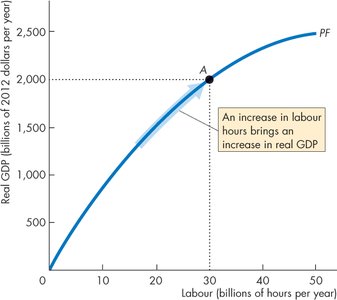

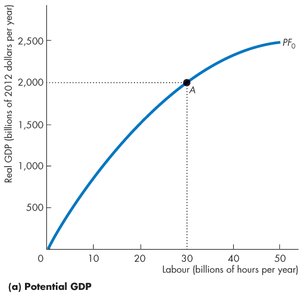

Aggregate Production Function

The aggregate production function shows how real GDP changes as the quantity of labour changes, holding other factors constant. An increase in labour increases real GDP.

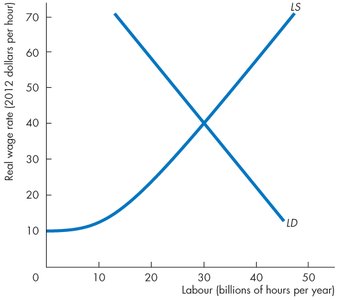

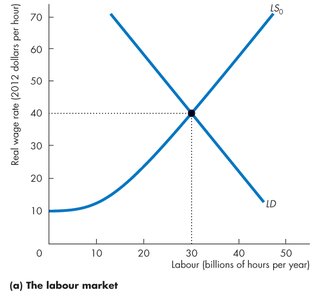

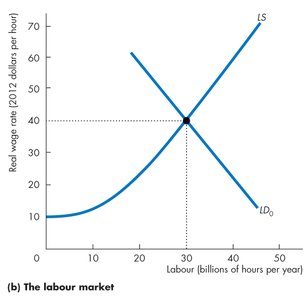

Aggregate Labour Market

Demand for Labour: Shows the quantity of labour demanded at different real wage rates.

Supply of Labour: Shows the quantity of labour supplied at different real wage rates.

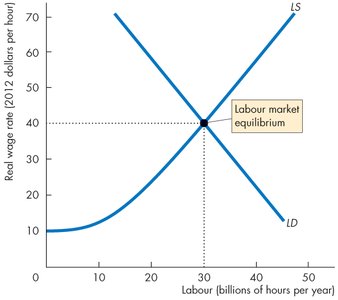

Equilibrium: The labour market is in equilibrium at the real wage rate where the quantity of labour demanded equals the quantity supplied.

Potential GDP at Full Employment

At labour market equilibrium, the economy is at full employment, and the corresponding real GDP is called potential GDP.

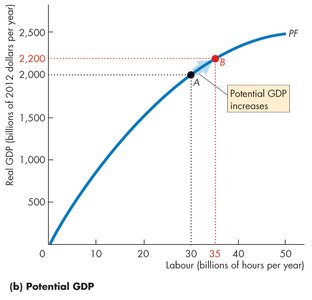

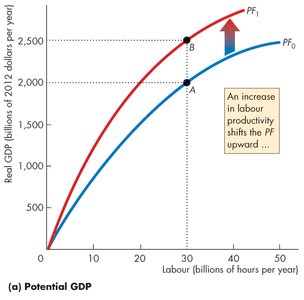

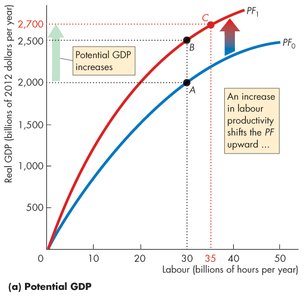

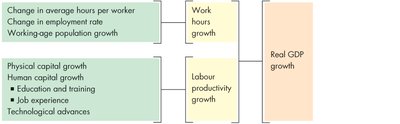

What Makes Potential GDP Grow?

Growth in the supply of labour

Growth in labour productivity

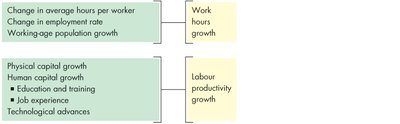

Growth in the Supply of Labour

Aggregate hours (total hours worked) change due to:

Average hours per worker

Employment-to-population ratio

Working-age population growth

Population growth increases aggregate hours and real GDP, but real GDP per person grows only if labour productivity increases.

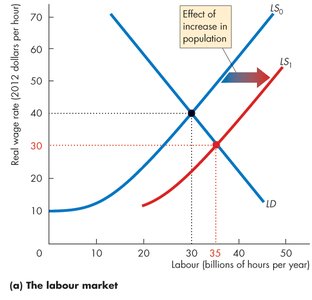

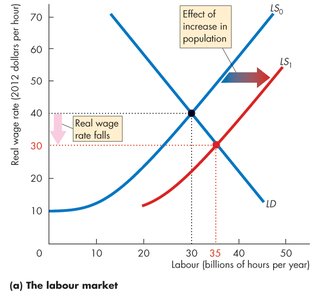

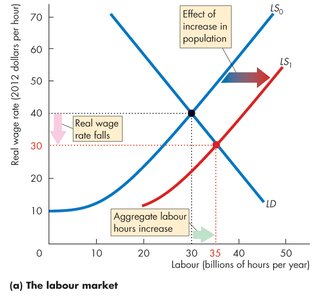

The Effects of Population Growth

An increase in population shifts the labour supply curve rightward, lowering the equilibrium real wage rate and increasing aggregate labour hours.

This increases potential GDP, but due to diminishing returns, real GDP per hour of labour may decrease.

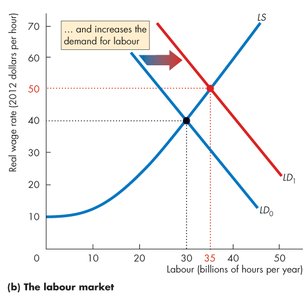

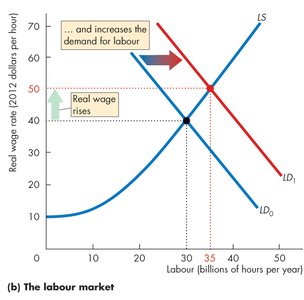

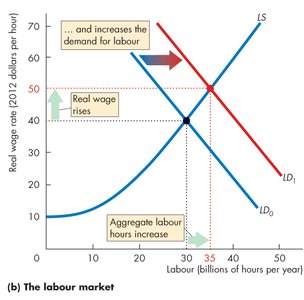

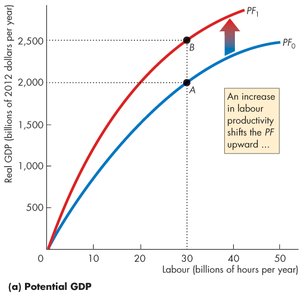

Growth of Labour Productivity

Labour productivity is the quantity of real GDP produced per hour of labour, calculated as real GDP divided by aggregate labour hours.

Increases in labour productivity raise the demand for labour, leading to higher real wages and more aggregate labour hours, which increases potential GDP.

Why Labour Productivity Grows

Preconditions for Labour Productivity Growth

The fundamental precondition is the incentive system created by firms, markets, property rights, and money.

Labour productivity growth depends on:

Physical capital growth: Accumulation of new capital increases capital per worker and productivity.

Human capital growth: Education, on-the-job training, and learning-by-doing are crucial for productivity growth.

Technological advances: Discovery and application of new technologies and goods significantly boost productivity.

Summary Table: Sources of Economic Growth

Source | Effect |

|---|---|

Population Growth | Increases aggregate labour hours and potential GDP, but may lower real GDP per hour due to diminishing returns |

Labour Productivity Growth | Raises real GDP per hour, increases demand for labour, real wages, and potential GDP |

Physical Capital Growth | Increases capital per worker, boosting productivity |

Human Capital Growth | Enhances skills and productivity through education and training |

Technological Advances | Drives long-term productivity and economic growth |

Formula for Economic Growth Rate:

Formula for Real GDP per Person:

Rule of 70 Formula:

Additional info: The above notes integrate textbook-level explanations, formulas, and visual summaries to provide a comprehensive overview of economic growth, its measurement, and its sources, suitable for macroeconomics college students.