Back

BackEconomic Growth, the Financial System, and Business Cycles: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Economic Growth, the Financial System, and Business Cycles

Long-Run Economic Growth

Long-run economic growth refers to the sustained upward trend in the economy’s output over time, leading to higher average standards of living. The best measure of the standard of living is real GDP per capita. Economists analyze growth by examining increases in real GDP per capita over long periods.

Importance: Higher productivity leads to improved living standards, allowing for greater consumption of goods and services.

Business Cycle: The economy alternates between periods of expansion (rising production, employment, and income) and recession (declining production, employment, and income).

Example: The U.S. economy has experienced significant growth over the past two centuries, lifting the average standard of living.

Calculating Growth Rates and the Rule of 70

Growth Rate: The percentage change in real GDP or real GDP per capita from one year to the next.

Rule of 70: An approximation for the number of years it takes for a variable to double, calculated as:

Small differences in growth rates can have large effects over time.

Determinants of Long-Run Growth

Labor Productivity: The quantity of goods and services produced by one worker or one hour of work.

Key Factors:

Quantity of capital per hour worked (physical and human capital)

Level of technology (processes and innovations)

Potential GDP: The level of real GDP attained when all firms are producing at capacity. It grows as the labor force, capital stock, and technology advance.

Saving, Investment, and the Financial System

The financial system is crucial for facilitating long-run economic growth by channeling funds from savers to borrowers, enabling firms to invest in capital and technology.

Components of the Financial System

Financial Markets: Where financial securities (stocks, bonds) are bought and sold.

Financial Intermediaries: Institutions like banks, mutual funds, and insurance companies that connect savers and borrowers.

Key Services:

Risk sharing

Liquidity

Information

Macroeconomics of Saving and Investment

National Income Accounting: In a closed economy (no trade), the relationship is:

Rearranged for investment:

Private Saving:

Public Saving:

Total Saving:

Thus, total saving equals total investment.

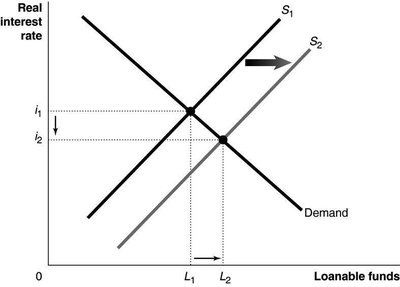

The Market for Loanable Funds

The market for loanable funds determines the equilibrium real interest rate and the quantity of funds exchanged between savers and borrowers.

Demand: Driven by firms’ willingness to borrow for investment projects (increases as interest rates fall).

Supply: Determined by households’ willingness to save and government saving (increases as interest rates rise).

Crowding Out: When government deficits reduce the supply of loanable funds, raising interest rates and reducing private investment.

Example: A shift from an income tax to a consumption tax increases the after-tax return to saving, shifting the supply curve for loanable funds to the right, lowering interest rates, and increasing investment and economic growth.

The Business Cycle

The business cycle consists of alternating periods of economic expansion and recession.

Phases of the Business Cycle

Expansion: Production, employment, and income rise.

Peak: The end of an expansion, before a downturn begins.

Recession: Production, employment, and income fall.

Trough: The end of a recession, before the next expansion begins.

Effects of the Business Cycle

Inflation Rate: Tends to rise during expansions and fall during recessions.

Unemployment Rate: Rises during recessions and may remain high even after a recession ends due to slow employment growth and firms operating below capacity.

Durable vs. Nondurable Goods: Production of durable goods fluctuates more than nondurables during the business cycle.

Stability and the Great Moderation

Since 1950, recessions have generally been less severe due to:

Growth of the service sector

Government transfer programs (e.g., unemployment insurance)

Active stabilization policies

Increased financial system stability (with exceptions, e.g., 2007–2009 recession)

Leading Indicators

Statistical series (e.g., stock prices, interest rates) that tend to change before the overall economy, providing insight into future business cycle movements.

Predictions are uncertain because economic behavior is less predictable than physical phenomena.

Key Terms and Concepts

Business cycle: Alternating periods of economic expansion and recession.

Capital: Physical assets and intellectual property used to produce goods and services.

Crowding out: Decline in private expenditure due to increased government purchases.

Financial intermediaries: Firms that borrow from savers and lend to borrowers.

Financial markets: Where financial securities are bought and sold.

Financial system: The network of markets and intermediaries through which funds flow.

Labor productivity: Output per worker or per hour worked.

Long-run economic growth: Process by which rising productivity increases living standards.

Market for loanable funds: Interaction of borrowers and lenders determining interest rates and loanable funds exchanged.

Potential GDP: Real GDP when all firms are producing at capacity.

Summary Table: Effects of Changes in Saving and Investment

Scenario | Effect on Supply of Loanable Funds | Effect on Interest Rate | Effect on Investment | Effect on Economic Growth |

|---|---|---|---|---|

Increase in saving (e.g., via consumption tax) | Supply shifts right | Decreases | Increases | Increases |

Government budget deficit | Supply shifts left | Increases | Decreases | Decreases |

Technological advancement | Demand shifts right | Increases | Increases | Increases |

Additional info: These notes synthesize textbook content, solved problems, and review/application questions to provide a comprehensive overview of Chapter 10 topics in macroeconomics.