Back

BackLong-Run Economic Growth: Sources and Policies – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Long-Run Economic Growth: Sources and Policies

Obtaining Economic Growth

Economic growth refers to the sustained increase in real GDP per capita over time. It is not inevitable, and history has seen periods of stagnation. Understanding why some countries achieve rapid growth while others lag is central to macroeconomic analysis.

Economic Growth Over Time and Around the World

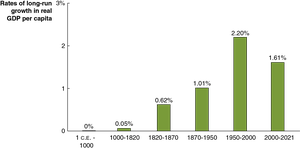

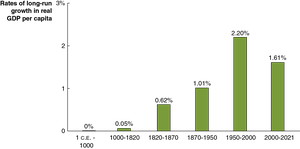

Economic growth has accelerated in the last two centuries, especially following the Industrial Revolution. Most of human history saw little change in living standards, but technological advancements have driven modern growth.

Definition: Economic growth is the increase in real GDP per capita.

Calculation: Growth rate =

Global Trends: Growth rates differ significantly across countries and eras.

Example: The Industrial Revolution marked the beginning of sustained growth in England and later other countries.

The Industrial Revolution

The Industrial Revolution (circa 1750) introduced mechanical power to production, replacing human and animal labor. This shift enabled long-run economic growth in England, the United States, France, and Germany.

The Effects of Different Growth Rates on Living Standards

Small differences in growth rates can lead to large differences in living standards over time. Countries with similar GDP per capita in 1960 have diverged significantly due to varying growth rates.

The Problem with Slow Economic Growth

Slow growth results in lower living standards, higher poverty, and increased infant mortality. For example, high-income countries have much lower infant mortality rates than low-income countries.

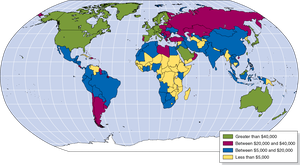

Variation in Per Capita Income Around the World

Economists classify countries as high-income (developed) or low-income (developing). Some countries, like Singapore and South Korea, have transitioned to newly industrializing status. Real GDP per capita varies widely, even after adjusting for cost-of-living differences.

Is Income All That Matters?

While income is a key indicator, improvements in health, education, and civil liberties also contribute to living standards. Technological and knowledge advances can improve quality of life even without significant income growth.

What Determines How Fast Economies Grow?

The Economic Growth Model

The economic growth model explains long-run growth rates in real GDP per capita. The key determinant is labor productivity, which depends on capital per hour worked and the level of technology.

Labor Productivity: Output per worker or per hour worked.

Capital: Physical assets used in production (machinery, equipment).

Technological Change: Improvements in the ability to produce output with given inputs.

Three Main Sources of Technological Change

Better Machinery and Equipment: Innovations like the steam engine and computers.

Increases in Human Capital: Accumulated knowledge and skills from education and training.

Better Organization and Management: Improved production methods, e.g., just-in-time systems.

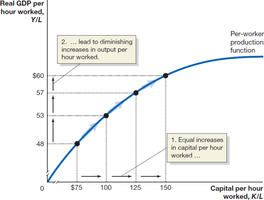

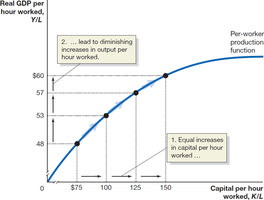

The Per-Worker Production Function

The per-worker production function shows the relationship between real GDP per hour worked and capital per hour worked, holding technology constant. Initial increases in capital are highly effective, but subsequent increases yield diminishing returns.

Diminishing Returns: Each additional unit of capital adds less to output than the previous unit.

Example: Adding ovens to a pizza store increases productivity, but after a certain point, extra ovens add little.

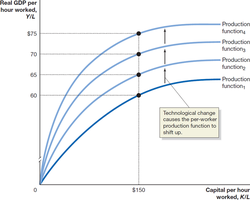

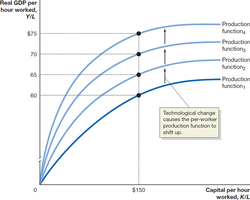

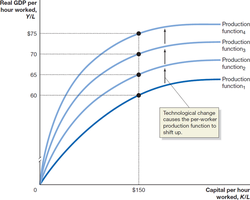

Technological Change and Output

Technological change shifts the production function upward, allowing more output per hour worked for the same amount of capital. In countries with high capital, technological change is the main driver of growth.

New Growth Theory

New growth theory, developed by Paul Romer, emphasizes that technological change is driven by economic incentives and the market system. Knowledge capital, unlike physical capital, is nonrival and nonexcludable, leading to increasing returns at the economy level.

Physical Capital: Rival and excludable (private good).

Knowledge Capital: Nonrival and nonexcludable (public good).

Government’s Role in Knowledge Capital Generation

Because knowledge capital is a public good, firms may underproduce it due to free riding. Governments can foster knowledge capital by:

Protecting intellectual property (patents, copyrights)

Subsidizing research and development

Subsidizing education

Protecting Intellectual Property

Patents grant exclusive rights to produce a product for 20 years, balancing firm incentives and societal benefits. Copyrights protect creative works for the creator’s lifetime plus 70 years.

Subsidizing R&D and Education

Governments may directly fund research or provide tax incentives. Subsidizing education ensures a technically skilled workforce, essential for innovation and growth.

Joseph Schumpeter and Creative Destruction

Schumpeter’s model highlights the role of entrepreneurs in economic growth. New products and technologies replace old ones, a process called creative destruction. Profits incentivize entrepreneurs to innovate and reorganize production.

Economic Growth in the United States

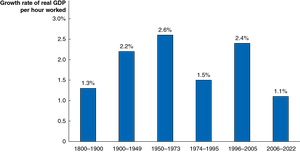

Fluctuations in Productivity Growth

U.S. productivity growth has varied over time, with notable increases following investment in research and development. Growth rates fell in the mid-1970s but rose again in the mid-1990s.

Is the United States Headed for Slow Growth?

There is debate among economists about future U.S. productivity growth. Some believe measurement issues understate growth, especially in services. Others argue that growth rates have entered a long-run decline.

Measurement Issues

Service output is harder to measure than goods output. Many improvements in convenience and quality are not captured in GDP statistics, potentially understating actual growth in living standards.

The Role of Information Technology

Information technology has driven productivity improvements, especially from 1996–2020. The impact of artificial intelligence may further increase productivity, though some economists are skeptical about future gains.

Secular Stagnation or Return to Faster Growth?

Some economists predict continued low growth due to slowing population and reduced capital needs. Others argue that investment will rebound, especially as global demand for U.S. goods increases.

Why Isn’t the Whole World Rich?

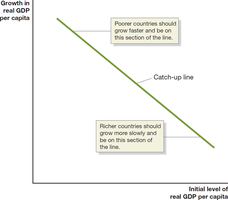

Economic Catch-Up

The economic growth model predicts that poor countries should grow faster than rich countries, a process called catch-up or convergence. This is due to the greater impact of additional capital and available technology in poorer countries.

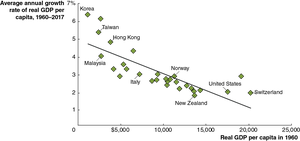

Evidence of Catch-Up

High-income countries show evidence of catch-up, with initially poorer countries experiencing higher growth rates than richer ones.

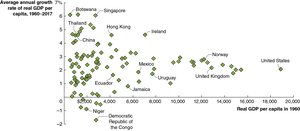

Failures of the Catch-Up Model

Many countries have not experienced catch-up, indicating that other factors impede growth.

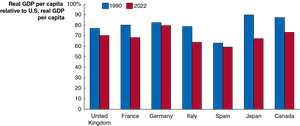

Other High-Income Countries and the U.S.

Some high-income countries have stopped catching up to the United States, due to differences in labor market flexibility, willingness to accept creative destruction, and efficient financial systems.

Why Don’t More Low-Income Countries Experience Rapid Growth?

Four key factors explain slow growth in many low-income countries:

Weak institutions (rule of law, property rights)

Wars and revolutions

Poor public education and health

Low rates of saving and investment

Weak Institutions

Effective enforcement of laws and property rights is essential for entrepreneurship and investment. An independent court system is also crucial.

Other Reasons for Lack of Growth

Wars and Revolutions: Disrupt investment and technological progress.

Poor Public Education and Health: Reduce worker productivity.

Low Rates of Saving and Investment: Undeveloped financial systems perpetuate low growth.

The Benefits of Globalization

Globalization, or openness to foreign trade and investment, has enabled many countries to escape the cycle of low savings and investment. Foreign direct investment (FDI) and foreign portfolio investment supplement domestic investment.

Growth Policies

Government Policies to Foster Economic Growth

Key policies include:

Enhancing property rights and the rule of law

Improving health and education

Promoting technological change

Encouraging savings and investment

Pro-Growth Policies

Health and Education: Provide increasing returns and prevent brain drain.

Technological Change: Essential for growth; can be promoted by encouraging FDI.

Savings and Investment: Eliminating corruption and providing tax incentives encourage investment.

Apply the Concept: Sub-Saharan Africa

Sub-Saharan Africa has seen a shift in FDI from extractive industries to manufacturing and services. Improved governance, political stability, and absence of violence are essential for catch-up growth.

Is Economic Growth Good or Bad?

While growth is generally beneficial for low-income countries, some argue that further growth in high-income countries may have negative effects, such as environmental degradation, resource depletion, and cultural diminishment. These are normative issues beyond the scope of economic analysis.

Summary Table: Factors Affecting Economic Growth

Factor | Effect on Growth |

|---|---|

Capital Accumulation | Increases productivity, subject to diminishing returns |

Technological Change | Shifts production function upward, enables sustained growth |

Human Capital | Improves labor productivity |

Institutions | Secure property rights and rule of law encourage investment |

Globalization | Facilitates foreign investment and technology transfer |

Government Policy | Supports R&D, education, and investment |