Back

BackMacroeconomic Policy, Economic Stability, and the Federal Debt: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Macroeconomic Policy, Economic Stability, and the Federal Debt

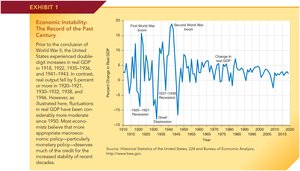

Economic Fluctuations: The Historical Record

Economic fluctuations refer to the ups and downs in real output (GDP) experienced by an economy over time. The United States has seen significant swings in real GDP, especially before World War II, with annual changes sometimes exceeding 5% to 10%. In the last six decades, these fluctuations have become more moderate, a trend attributed by most economists to improved monetary policy.

Real GDP: The value of all final goods and services produced within a country in a given period, adjusted for inflation.

Economic Instability: Large and unpredictable changes in output and employment.

Stabilization: The reduction of the amplitude of economic fluctuations.

Can Discretionary Policy Promote Economic Stability?

Stabilization policy aims to reduce the volatility of the business cycle through government intervention. There are two main perspectives on the effectiveness of such policies:

Activist View: Advocates believe that policymakers can and should use monetary and fiscal policy to counteract economic fluctuations.

Non-activist View: Critics argue that discretionary policy often does more harm than good due to timing and information lags.

Both perspectives agree that stabilization is challenging due to practical problems with timing, such as recognition, implementation, and impact lags.

Forecasting Tools and Macro Policy

Forecasting tools help policymakers anticipate economic downturns and expansions. One widely used tool is the Index of Leading Indicators, a composite statistic based on 10 key variables that typically change before the overall economy does.

Index of Leading Indicators: Predicts recessions and expansions, but with some false positives and variable lead times.

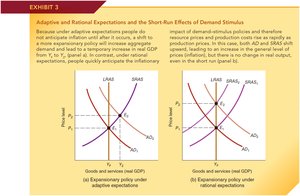

Expectations and Macroeconomic Policy

Theories of Expectations Formation

Expectations about future economic conditions influence how individuals and firms respond to policy changes. Two main theories explain how expectations are formed:

Adaptive Expectations: People base their expectations on past events, adjusting slowly as new information arrives. This causes expectations to lag behind actual changes.

Rational Expectations: People use all available information, including anticipated policy changes, to form expectations. Systematic errors are avoided, though random errors can still occur.

Key Difference: Under adaptive expectations, policy can have short-term real effects; under rational expectations, anticipated policy changes are quickly incorporated, reducing real effects.

Macro Policy Implications of Adaptive and Rational Expectations

The effectiveness of monetary and fiscal policy depends on how expectations are formed:

With adaptive expectations, unanticipated expansionary policy can temporarily boost output and employment.

With rational expectations, anticipated policy changes are quickly offset by changes in wages and prices, making real effects less predictable.

Both theories agree that sustained expansionary policy leads to inflation without permanently increasing output or employment.

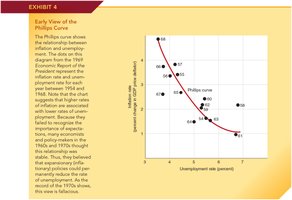

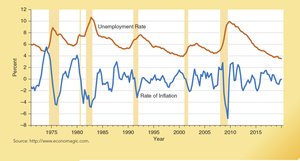

The Phillips Curve: Inflation and Unemployment

Early View of the Phillips Curve

The Phillips Curve illustrates the inverse relationship between inflation and unemployment observed in the 1960s and 1970s. Policymakers believed they could exploit this tradeoff to achieve lower unemployment at the cost of higher inflation.

Phillips Curve: Shows a short-run tradeoff between inflation and unemployment.

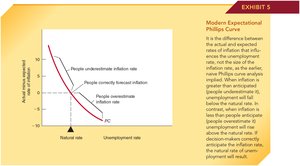

Expectations and the Modern Phillips Curve

The modern view incorporates expectations, emphasizing that the actual rate of inflation relative to the expected rate determines unemployment. When actual inflation exceeds expectations, unemployment falls below its natural rate, and vice versa.

Natural Rate of Unemployment: The unemployment rate consistent with stable inflation, where the labor market is in equilibrium.

Unemployment and Changes in the Rate of Inflation

Historical data show that sharp reductions in inflation often precede recessions and increases in unemployment, while periods of low and stable inflation are associated with low and stable unemployment rates.

The Growing Federal Debt and Economic Stability

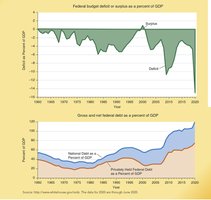

Deficits, Surpluses, and the National Debt

Federal budget deficits occur when government expenditures exceed revenues, while surpluses occur when revenues exceed expenditures. The national debt is the accumulation of past deficits minus surpluses.

From WWII to 1973, deficits were small and the debt-to-GDP ratio declined.

Since the 1970s, larger deficits have increased the debt-to-GDP ratio, especially after the 2008-09 recession.

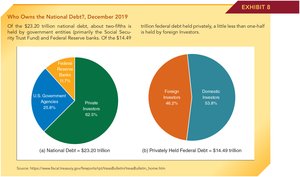

Who Owns the National Debt?

The national debt is held by both government agencies and private investors, including foreigners. As of December 2019:

37.5% held by government agencies and the Federal Reserve

62.5% held privately (domestic and foreign investors)

Of privately held debt, 46.2% is owned by foreigners

How Does Debt Financing Influence Future Generations?

Borrowing from foreigners can be beneficial if used for productive investment, but harmful if used for current consumption. Large deficits from 2001-2020 suggest current generations benefited more than future generations will.

Productive Investment: Increases future output, making debt service easier.

Current Consumption: Leaves future generations with debt but no corresponding assets.

Why is Deficit Spending So Difficult to Control?

Political incentives favor deficit spending because politicians can provide benefits without immediate tax increases. Unfunded promises (e.g., Social Security, Medicare) also contribute to the debt, reflecting the short-sightedness effect in politics.

Short-sightedness Effect: The tendency of policymakers to favor policies with immediate benefits and delayed costs.

Have Federal Debt Obligations Grown to a Dangerous Level?

While direct default is unlikely for a country with a central bank, excessive debt may lead to inflation as governments create money to meet obligations. Demographic trends, such as the retirement of baby boomers, will further strain federal finances.

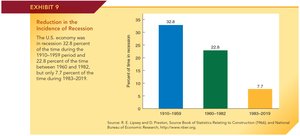

Perspective on Recent Macroeconomic Policy and Economic Instability

Despite current challenges, the U.S. economy has experienced greater stability in recent decades. The percentage of time spent in recession has declined significantly since 1983.

Summary Table: Key Concepts

Concept | Definition | Example/Application |

|---|---|---|

Stabilization Policy | Government actions to reduce economic fluctuations | Monetary and fiscal policy responses to recessions |

Adaptive Expectations | Expectations based on past events | Inflation expectations lag behind actual inflation |

Rational Expectations | Expectations based on all available information | People anticipate effects of policy changes |

Phillips Curve | Inverse relationship between inflation and unemployment (short run) | Lower unemployment at the cost of higher inflation (historical view) |

National Debt | Total accumulation of past federal deficits | U.S. national debt as a percent of GDP |