Back

BackMacroeconomics Study Guide: Financial System, Money, and Loanable Funds

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Financial Markets and the Financial System

Overview of the Financial System

The financial system is a network of institutions that facilitate the flow of funds from savers to borrowers, supporting investment and economic growth. It includes financial markets and intermediaries, each playing a distinct role in the economy.

Financial markets: Institutions where savers directly provide funds to borrowers (e.g., bond and stock markets).

Financial intermediaries: Institutions (e.g., banks, mutual funds) that indirectly connect savers and borrowers.

Financial asset: A paper claim entitling the buyer to future income (e.g., bonds, stocks).

Physical asset: A tangible object (e.g., real estate, equipment) that can be sold.

Liability: An obligation to pay money in the future.

Liquidity: The ease with which an asset can be converted to cash without loss of value.

The Bond Market

Bonds are certificates of indebtedness issued by borrowers to raise funds. They specify maturity dates and interest rates, and their value depends on term, credit risk, and tax treatment.

Term: Longer-term bonds generally offer higher interest rates.

Credit risk: Higher risk leads to higher interest rates.

Tax treatment: Municipal bonds offer tax advantages, lowering their interest rates.

The Stock Market

Stocks represent partial ownership in firms and are traded on exchanges. Their prices reflect expected profitability and are influenced by supply and demand.

Equity finance: Raising money by selling stock.

Debt finance: Raising money by selling bonds.

Stock index: An average of a group of stock prices, used to track market performance.

Financial Intermediaries

Banks: Accept deposits and make loans, facilitating payments and money creation.

Mutual funds: Pool funds to buy diversified portfolios of stocks and bonds.

Pension funds: Provide retirement income by holding assets for members.

Insurance companies: Offer policies guaranteeing payments to beneficiaries.

Saving and Investment in National Income Accounts

National Income Identity

Gross Domestic Product (GDP) is divided into consumption (C), investment (I), government purchases (G), and net exports (NX):

In a closed economy:

Isolating investment:

National saving (S):

Thus, (saving equals investment)

Private and Public Saving

Private saving: (income after taxes and consumption)

Public saving: (tax revenue minus government spending)

Budget surplus: Excess of tax revenue over spending

Budget deficit: Shortfall of tax revenue from spending

Money and Banking

Functions of Money

Money is any commodity or token generally accepted as payment. It serves three main functions:

Medium of exchange: Facilitates transactions, eliminating barter.

Unit of account: Provides a standard measure for prices.

Store of value: Retains purchasing power over time.

Types of Money

Fiat money: Money by government decree (e.g., currency, bank deposits).

M1: Currency, traveler’s checks, checkable deposits.

M2: M1 plus savings deposits, small time deposits, money market funds.

The Banking System

Commercial banks: Accept deposits, make loans, and manage risk.

Reserves: Currency in vaults and reserve accounts at the Fed.

Required reserve ratio: Fraction of deposits banks must hold as reserves.

Liquid assets: Short-term, low-risk assets (e.g., Treasury bills).

Securities and loans: Investments and loans to businesses and individuals.

Bank Regulations

FDIC deposit insurance: Guarantees deposits up to $250,000.

Capital requirements: Owners must hold assets above deposit values.

Reserve requirements: Minimum reserves set by the Fed.

Discount window: Fed lends to banks as needed.

Banks and Money Creation

100-Percent-Reserve Banking

In this system, banks hold all deposits as reserves, and do not influence the money supply.

Fractional-Reserve Banking and Money Creation

Banks hold only a fraction of deposits as reserves, lending out the rest and thereby creating money.

Reserve ratio: Fraction of deposits held as reserves.

Money multiplier:

The Federal Reserve System

Structure and Policy Tools

The Federal Reserve (Fed) is the central bank of the United States, regulating financial institutions and markets.

Board of Governors: Seven members, 14-year terms.

12 regional banks: Serve different areas of the country.

Federal Open Market Committee (FOMC): Main policy-making body.

Policy Tools

Required reserve ratios: Minimum reserves banks must hold.

Discount rate: Interest rate for Fed loans to banks.

Open market operations: Buying/selling government securities to influence money supply.

Extraordinary crisis measures: Quantitative easing, credit easing, operation twist.

Money Creation and the Monetary Base

Monetary base: Coins, Federal Reserve notes, and bank reserves at the Fed.

Fed actions (e.g., increasing reserve ratios, raising discount rate, selling securities) decrease money supply.

Open market purchases increase reserves and money supply; sales decrease them.

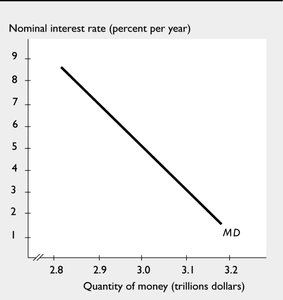

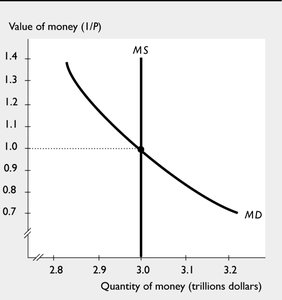

The Demand for Money Curve

Money Demand and Interest Rates

The demand for money is the amount households and firms choose to hold, influenced by the nominal interest rate (the opportunity cost of holding money).

As the nominal interest rate rises, the quantity of money demanded falls.

The demand for money curve shows the negative relationship between interest rate and quantity of money demanded.

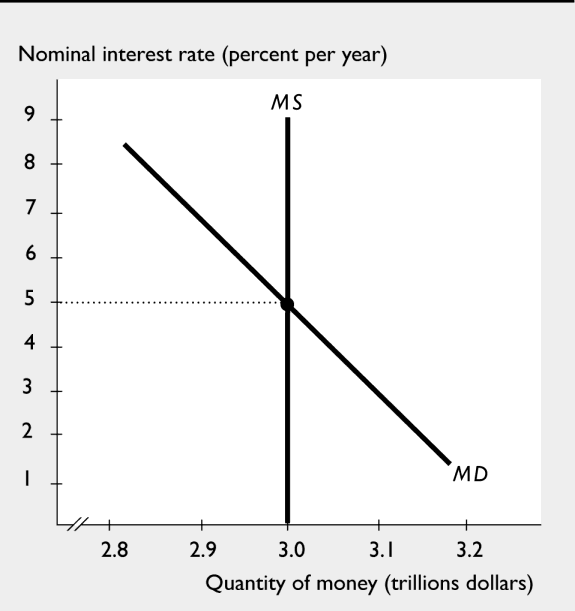

Money Market Equilibrium

The equilibrium interest rate is determined where the demand for money equals the fixed supply of money.

Supply of money is vertical (fixed by the central bank).

Equilibrium occurs at the intersection of money demand and supply curves.

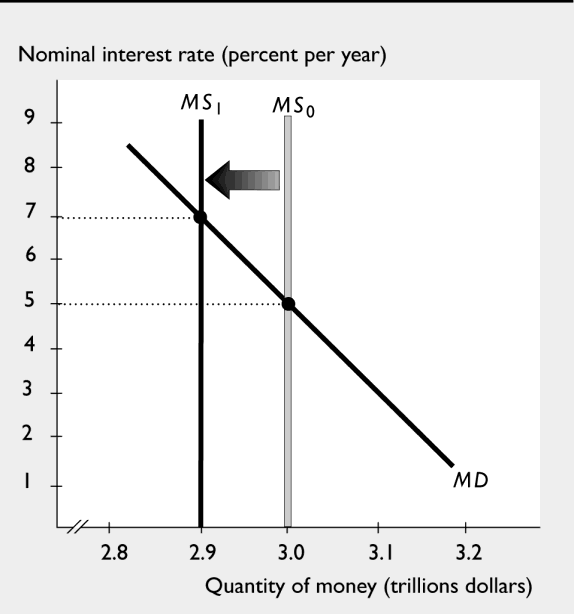

Changing the Interest Rate

The Fed can influence the interest rate by changing the money supply. A decrease in money supply shifts the supply curve left, raising the equilibrium interest rate.

Open market sales decrease money supply, raising interest rates.

Open market purchases increase money supply, lowering interest rates.

The Money Market in the Long Run

Value of Money and Price Level

In the long run, the nominal interest rate equals the equilibrium real interest rate plus the inflation rate. The value of money is the quantity of goods and services a unit of money can buy, and is the inverse of the price level.

Money market equilibrium determines the value of money.

In the long run, an increase in money supply raises the price level and lowers the value of money.

The Quantity Theory of Money

When real GDP equals potential GDP, an increase in money supply brings an equal percentage increase in the price level.

Velocity of circulation:

Equation of exchange:

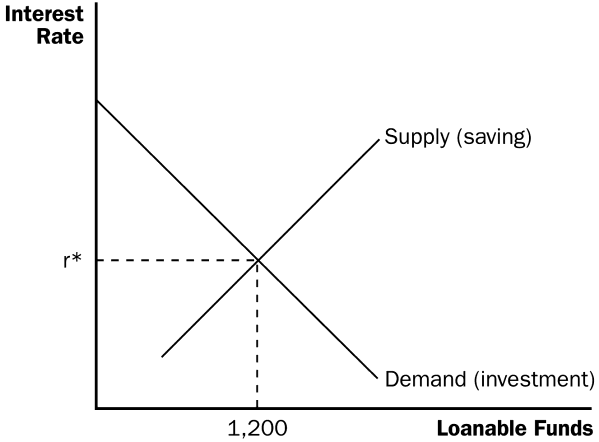

The Market for Loanable Funds

Supply and Demand for Loanable Funds

The market for loanable funds matches savers (supply) with borrowers (demand). The interest rate is the price of a loan, determined by the equilibrium of supply and demand.

As interest rate rises, supply of loanable funds increases, demand decreases.

Equilibrium interest rate equates supply and demand.

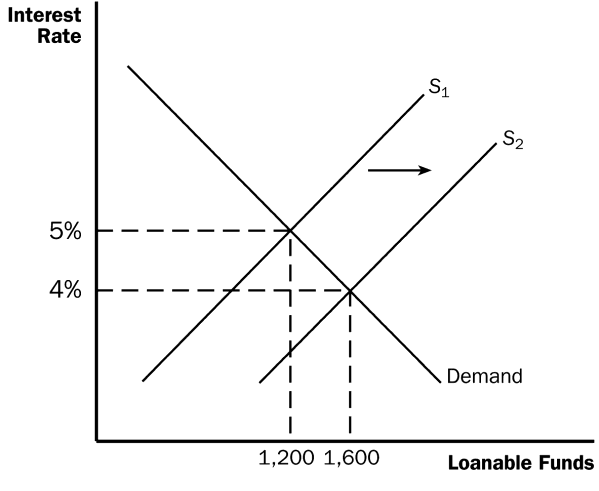

Savings Incentives

Government policies that encourage saving shift the supply of loanable funds right, lowering the equilibrium interest rate and increasing investment.

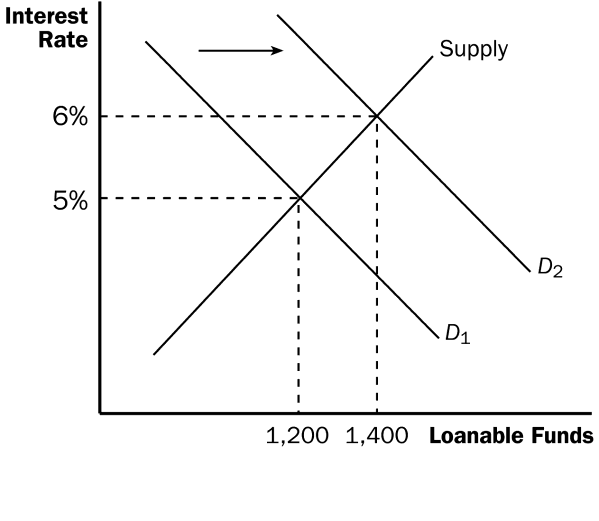

Investment Incentives

Policies that encourage investment (e.g., investment tax credits) shift the demand for loanable funds right, raising the equilibrium interest rate and increasing investment.

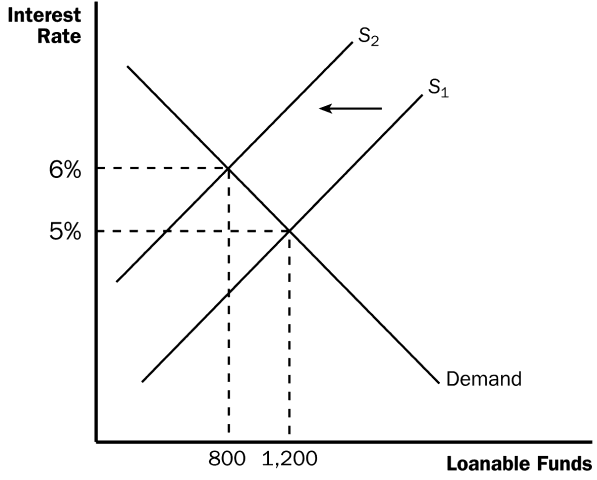

Government Budget Deficits and Surpluses

Budget deficits reduce public saving, shifting the supply of loanable funds left, raising interest rates, and decreasing investment (crowding out). Surpluses have the opposite effect.