Back

BackModern Macroeconomics and Monetary Policy: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Modern Macroeconomics and Monetary Policy

Historical Perspectives on Monetary Policy

Monetary policy has evolved through significant debates between Keynesian and Monetarist schools of thought. In the mid-20th century, Keynesians believed the money supply had little effect on the economy, while Monetarists, led by Milton Friedman, argued that changes in the money supply were central to both inflation and economic instability. The modern consensus recognizes that monetary policy has a substantial impact on macroeconomic outcomes, including output, employment, and price levels.

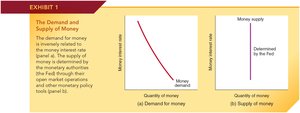

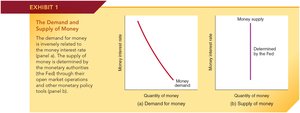

The Demand and Supply of Money

Demand for Money

The demand for money refers to the quantity of money that households and businesses wish to hold at any given time. It is inversely related to the money interest rate: as interest rates rise, holding money becomes more costly compared to holding interest-earning assets like bonds.

Key Point: Higher interest rates decrease the demand for money.

Key Point: Lower interest rates increase the demand for money.

Formula: The demand for money can be represented as a downward-sloping function of the interest rate.

Supply of Money

The supply of money is determined by the central bank (the Federal Reserve in the U.S.) and is independent of the interest rate in the short run. The money supply is represented as a vertical line because it is set by policy decisions rather than market forces.

Key Point: The central bank controls the money supply through open market operations and other policy tools.

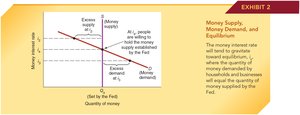

Equilibrium in the Money Market

Equilibrium occurs where the demand for money equals the supply of money. The interest rate adjusts to ensure that the quantity of money demanded matches the quantity supplied by the central bank.

Key Point: If the interest rate is above equilibrium, there is an excess supply of money; if below, there is excess demand.

Transmission of Monetary Policy

Expansionary Monetary Policy

When the central bank adopts an expansionary monetary policy, it typically buys government bonds, increasing the money supply and bank reserves. This action lowers real interest rates, stimulates investment and consumption, and increases aggregate demand (AD).

Key Point: Expansionary policy shifts the money supply curve rightward, lowering interest rates.

Key Point: Lower interest rates increase the supply of loanable funds and stimulate economic activity.

Aggregate Demand and Output

As real interest rates fall, aggregate demand increases, leading to higher output and price levels in the short run. If the monetary expansion is unanticipated, the economy experiences a short-run boost in output and inflation.

Key Point: The effects are transmitted through interest rates, exchange rates, and asset prices.

Channels of Monetary Policy Transmission

Expansionary monetary policy affects the economy through several channels:

Directly increases investment and consumption by lowering interest rates

Depreciates the currency, boosting net exports

Raises asset prices, increasing personal wealth and further stimulating spending

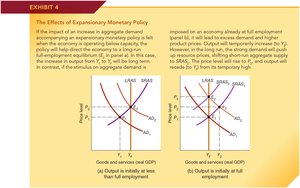

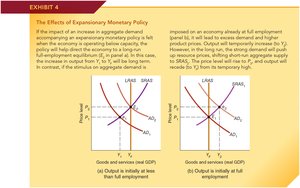

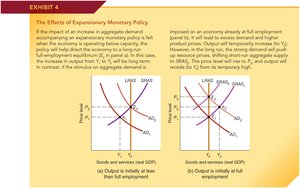

Effects of Expansionary Policy at Different Economic States

If the economy is below full employment, expansionary policy can restore output to its potential level. If the economy is already at full employment, further increases in AD lead to inflation and only temporary increases in output.

Key Point: Long-term output returns to full employment, but the price level remains higher.

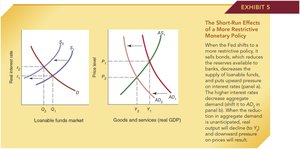

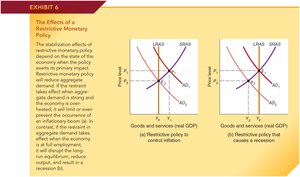

Restrictive Monetary Policy

Restrictive (contractionary) monetary policy involves selling government bonds, reducing the money supply, and raising real interest rates. This decreases aggregate demand, output, and puts downward pressure on prices.

Key Point: Restrictive policy is used to combat inflation or cool an overheated economy.

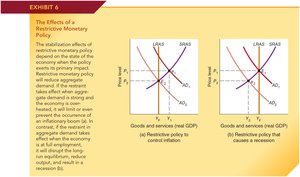

Stabilization Effects of Restrictive Policy

The effectiveness of restrictive policy depends on the economic context. If applied during strong demand, it can prevent inflation. If applied at full employment, it may cause a recession.

Key Point: Timing and context are crucial for stabilization policy.

Long-Run Effects of Monetary Policy

The Quantity Theory of Money

The Quantity Theory of Money states that in the long run, changes in the money supply lead to proportional changes in the price level, assuming velocity and real output are constant. Sustained rapid growth in the money supply results in inflation.

Formula: where is money supply, is velocity, is price level, and is real output.

Long-Run Adjustment to Monetary Expansion

When the money supply grows rapidly, aggregate demand increases, temporarily boosting output above potential. However, resource prices rise, shifting aggregate supply leftward, and output returns to its long-run potential while the price level rises.

Key Point: The ultimate result is higher prices (inflation), not higher real output.

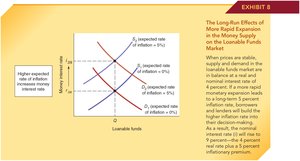

Loanable Funds Market and Interest Rates

In the long run, higher expected inflation leads to higher nominal interest rates, as lenders demand a premium to compensate for inflation. The nominal interest rate equals the real interest rate plus the expected inflation rate.

Formula: where is nominal interest rate, is real interest rate, and is expected inflation.

Challenges in Conducting Monetary Policy

Time Lags and Policy Effectiveness

There are long and variable lags between monetary policy actions and their effects on the economy. This makes it difficult for policymakers to time interventions correctly, increasing the risk of policy errors and economic instability.

Key Point: Constantly shifting policy can destabilize the economy rather than stabilize it.

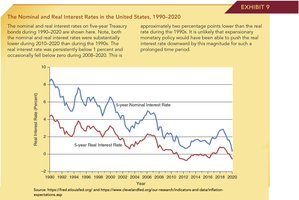

Recent Trends: Interest Rates and Demographics

Recent Low Interest Rates

Since 2008, real interest rates in the U.S. and other advanced economies have been persistently low, sometimes even negative. This trend is unlikely to be solely the result of expansionary monetary policy.

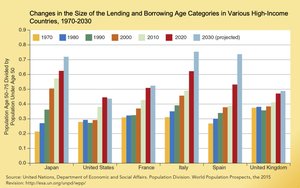

Demographic Changes and Loanable Funds

Demographic shifts, such as an aging population, have increased the supply of loanable funds and reduced demand, contributing to lower interest rates globally. Older populations tend to save more, increasing the supply of funds available for lending.

Key Point: The share of the population aged 50-75 has increased, expanding the supply of loanable funds.

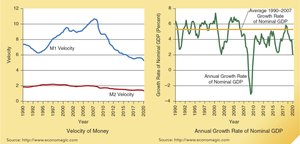

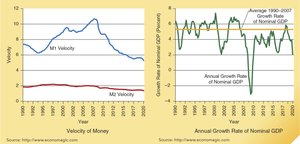

Velocity of Money and Monetary Policy

Velocity of Money

The velocity of money measures how frequently money circulates in the economy. A decline in velocity can blunt the effects of expansionary monetary policy, as seen after the 2008-2009 recession when both M1 and M2 velocity fell sharply.

Key Point: Lower velocity means that increases in the money supply have a smaller impact on nominal GDP.

Nominal GDP Growth

The growth rate of nominal GDP reflects changes in both the money supply and its velocity. After the Great Recession, nominal GDP growth remained modest, indicating that monetary policy was not highly expansionary in effect.

Summary Table: Effects of Monetary Policy

Policy Action | Short-Run Effect | Long-Run Effect |

|---|---|---|

Expansionary (Increase Money Supply) | Lower interest rates, higher output, higher prices (inflation) | Higher price level (inflation), output returns to potential |

Restrictive (Decrease Money Supply) | Higher interest rates, lower output, lower inflation | Lower price level, output returns to potential |

Additional info: These notes integrate textbook content with standard macroeconomic theory to provide a comprehensive, exam-ready summary of modern monetary policy and its effects.