Back

BackMoney and the Banking System: Structure, Functions, and Policy Tools

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Money and the Banking System

What is Money?

Money is defined as anything that is generally accepted in exchange for goods and services. It serves as a temporary store of purchasing power, enabling individuals to buy other goods and services in the future. The value of money is derived from its acceptability and its ability to facilitate transactions efficiently.

Medium of Exchange: Money is used to buy and sell goods and services.

Unit of Account: Money provides a common measure for valuing goods and services.

Store of Value: Money can be saved and used for future purchases.

Standard of Deferred Payment: Money is used to settle debts payable in the future.

Example: U.S. dollars, euros, and yen are all forms of money because they are widely accepted for transactions in their respective economies.

How the Supply of Money Affects Its Value

The value of money is influenced by its supply relative to the demand for goods and services. If the supply of money increases rapidly without a corresponding increase in goods and services, the value of money falls, leading to inflation. Conversely, a limited supply of money can increase its value, potentially causing deflation.

Measuring the Money Supply

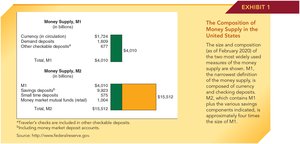

The money supply in the United States is measured using several aggregates, primarily M1 and M2. These aggregates differ in their liquidity and components.

M1: The most liquid forms of money, including currency in circulation, demand deposits, and other checkable deposits.

M2: Includes all of M1 plus savings deposits, small time deposits, and money market mutual funds.

Example: M1 is used for everyday transactions, while M2 includes assets that are less liquid but can be quickly converted to cash.

Credit Cards versus Money

Credit cards are not considered money. They are a means of obtaining a loan to make purchases, and the balances on credit cards are liabilities, not assets. Money, in contrast, is an asset that can be used directly for transactions.

The Business of Banking

Functions of Commercial Banking Institutions

Banks play a crucial role in the financial system by accepting deposits, providing loans, and facilitating payments. They attract deposits by offering interest and use a portion of these deposits to make loans, generating income. Banks must also hold reserves to meet withdrawal demands.

Deposits: Checkable, savings, and time deposits are liabilities for banks.

Loans and Investments: Banks use deposits to make loans and investments, which are assets.

Reserves: A portion of deposits is held as reserves, either as cash or deposits with the central bank.

Fractional Reserve Banking

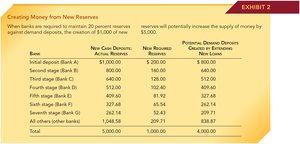

Under fractional reserve banking, banks are required to keep only a fraction of their deposits as reserves. The remainder can be loaned out, which increases the money supply through the process of money creation.

How Banks Create Money by Extending Loans

Banks create money by making loans from their excess reserves. When a bank extends a loan, it credits the borrower's account, increasing the total deposits in the banking system. The process is limited by the reserve requirement set by the central bank.

Money Multiplier: The potential expansion of the money supply is determined by the reserve requirement. The formula for the simple deposit multiplier is:

For example, with a 20% reserve requirement, the multiplier is 5.

The Federal Reserve System

Structure of the Federal Reserve System

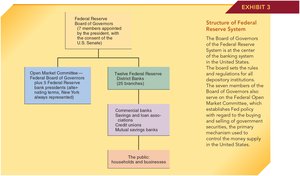

The Federal Reserve (the Fed) is the central bank of the United States. It consists of the Board of Governors, twelve regional Federal Reserve Banks, and the Federal Open Market Committee (FOMC). The Board of Governors sets policy and regulations, while the FOMC directs open market operations.

Board of Governors: Seven members appointed by the President and confirmed by the Senate.

Federal Reserve Banks: Twelve district banks serving different regions of the country.

FOMC: Responsible for setting monetary policy, especially open market operations.

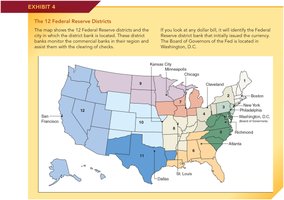

The 12 Federal Reserve Districts

The United States is divided into 12 Federal Reserve districts, each with its own regional bank. These banks supervise commercial banks in their regions and assist with the clearing of checks.

The Independence of the Fed

The Federal Reserve operates independently of the federal government to insulate monetary policy from political pressures. This independence is considered important for maintaining price stability and controlling inflation.

How the Fed Controls the Money Supply

Monetary Policy Tools

The Fed uses several tools to control the money supply and influence economic activity:

Reserve Requirements: The percentage of deposits that banks must hold as reserves. Lowering the reserve requirement increases the money supply; raising it decreases the money supply.

Open Market Operations: The buying and selling of government securities in the open market to influence the level of bank reserves.

Discount Rate and Extension of Loans: The interest rate charged by the Fed on loans to commercial banks. Lowering the rate encourages borrowing and increases the money supply.

Interest on Reserves: The Fed pays interest on reserves held by banks, influencing their willingness to lend excess reserves.

Recent Fed Policy, the Monetary Base, and the Money Supply

The Monetary Base

The monetary base consists of currency in circulation and reserves held by banks at the Fed. It is the foundation for the broader money supply (M1 and M2). Changes in the monetary base, through Fed policy, can have significant effects on the overall money supply.

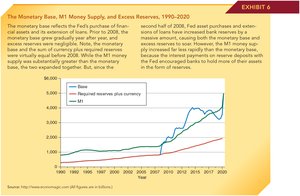

Trends in the Monetary Base, M1, and Excess Reserves (1990–2020)

From 1990 to 2008, the monetary base and M1 grew steadily. After 2008, the Fed's policies, including quantitative easing, led to a sharp increase in the monetary base and excess reserves, while M1 grew at a slower pace due to interest payments on reserves.

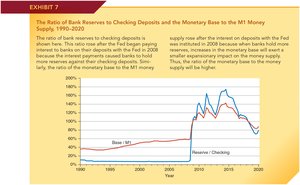

Ratio of Bank Reserves to Checking Deposits and Monetary Base to M1 (1990–2020)

After 2008, the ratio of bank reserves to checkable deposits and the ratio of the monetary base to M1 both increased. This was due to the Fed's policy of paying interest on reserves, which encouraged banks to hold more reserves rather than lend them out, moderating the expansion of the money supply.

Ambiguities in the Meaning and Measurement of the Money Supply

The Changing Nature of Money

In recent decades, the nature of money has evolved with the development of new financial instruments and payment technologies. This has made it more challenging to define and measure the money supply precisely, as distinctions between money and near-money assets have blurred.

Example: The rise of electronic payments, online banking, and money market funds has changed how people use and hold money.